|

|

Audit Buzz Newsletter

January 2025

|

Engagement and Office Updates

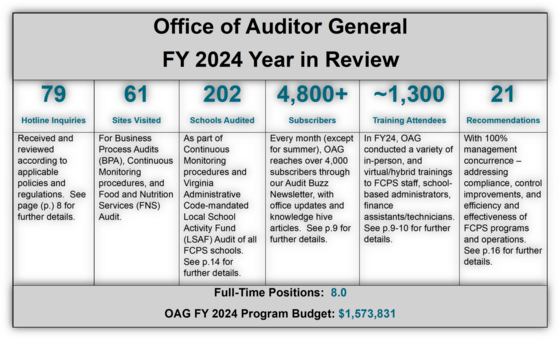

In this issue of the Audit Buzz, we provide an update on current engagements; provide highlights the Office of Auditor General's (OAG) Fiscal Year (FY) 2024 Annual Report, explain What’s the Difference Between Findings, Observations, and Exceptions in the Knowledge Hive; and offer a training opportunity for Fairfax County Public Schools (FCPS) employees.

Prior editions of Audit Buzz are archived here on OAG website.

As always, we appreciate the cooperation and courtesies extended to our staff by FCPS management and staff during all past, current, and future audit engagements.

Here is a challenge to test your audit knowledge, before we begin this issue:

Say What You See

*Hint: this is two words

Current Engagement Update

At the January 13 Audit Committee meeting, OAG presented the following agenda items:

Knowledge Hive

What’s the Difference Between Findings, Observations, and Exceptions

If you ever read or receive our audit reports and memos, you may see our office using different terms: findings, observations, and exceptions. While these terms all indicate there are opportunities for improvement in your school or department, there are subtle yet important distinctions. If you have ever wondered what the difference is – or didn’t realize there was one – in today’s Audit Buzz, we’ll be diving into just that!

Findings: Key Issues Requiring Attention

-

When We Issue Findings: Findings are issued when management needs to act on an important issue identified during an audit. According to our professional standards, the Yellow Book, a finding can be issued when there are weaknesses in internal controls or checks and balances, fraud, or noncompliance with laws, regulations, or other requirements. In accordance with the Yellow Book, when we issue findings, we will provide details on the condition (issue), criteria (standards, laws, guidelines, etc.), cause, effect, and recommendation. Findings are most often issued in department or program performance audits (past audits include Facilities Maintenance and Food and Nutrition Services), or Business Process Audits (BPAs). Additionally, our office assigns a risk level with findings of high, moderate, or low to indicate the potential impact to FCPS in terms of efficiency, effectiveness, and compliance. On the other hand, exceptions and observations do not have risk levels. Check out our June 2024 Audit Buzz article if you’d like to read more about the components of a finding!

-

Example: Outdated Regulation – A department has not updated one of their regulations and contains outdated information. This poses a risk that employees will be following incorrect procedures, which may lead to non-compliance or inefficiency.

-

What Comes Next: After a finding is issued, management must provide a response and due date. OAG follows up on these corrective actions for implementation to improve FCPS processes, controls, and operations and reports progress to the School Board Audit Committee. Note: For Business Process Audits, we require management response and corrective actions only for moderate and high-risk findings.

Observations: Areas for Improvement

-

When We Issue Observations: Observations can be issued during Local School Activity Funds (LSAF) audits, department/program performance audits, and BPAs. It may not always involve non-compliance, internal control weakness, or fraud, but is still presents important information for management to improve processes.

-

Example: Local School Activity Funds – Signatures are required by the principal but only recommended for the finance assistant/technician on the bank reconciliation. Even if the one required signature is present, we may issue an observation, as the presence of both signatures is considered an FCPS best practice.

-

What Comes Next: Observations do not require formal management responses. However, we encourage schools and departments to take them into consideration, as they represent areas to implement best practices, guidelines, or improve efficiency and effectiveness.

Exceptions: Identified Instances of Non-Compliance

-

When We Issue Exceptions: Exceptions are issued during our quarterly continuous monitoring procedures when we notice an instance of non-compliance with FCPS regulations, policies, or guidelines (i.e. in specific and sampled school finance transactions). In our memorandums, we will provide conditions, criteria, and recommendations for any exceptions, but exclude cause and effect. As a result, they are not considered findings, based on the Yellow Book definition.

-

Example: Untimely Deposit – a deposit was not made within five business days for cash receipts greater than $25, as required by FCPS Regulation 5910 Monetary Receipts.

-

What Comes Next: We communicate Continuous Monitoring exceptions in memorandums to finance assistants/technicians and principals/program managers. These do not require any management response or corrective action; however, we encourage staff to take them seriously to maintain compliance with the required FCPS financial guidelines.

Final Takeaway: All are important!

Whether it’s a finding, observation, or exception, each provides valuable insights to improve FCPS operations and maintain compliance. As always, if you would like additional clarification about any of these terms and what they mean for your school or department, please feel free to reach out to our office!

Did You Know?

OAG Outreach and Education: Continuing Professional Education (CPE) Opportunity

OAG is registered with the National Association of State Boards of Accountancy (NASBA) and serves as the sponsor for the FCPS Continuing Professional Education (CPE) programs, dedicated to support FCPS employees with complimentary CPE credits required by various certification agencies. OAG is pleased to offer a new NASBA training opportunity for FCPS employees to earn up to 3 CPE credits:

Course: Bridging Payroll and Audit: Tools for Excellence

Date: March 7, 2025

Time: 9:00 AM - 12:00 PM

Do you know that approximately 89% of FCPS annual budget is spent on salary? In this training, Office of Payroll Management and Office of Auditor General, will co-present topics related to payroll compliance, regulations and internal controls, timekeeping and attendance, reconciliation etc. We will also cover topics of fraud prevention and detection related to payroll, time and attendance – including common payroll fraud schemes, red flags to look for, and how to use audits to detect and prevent payroll fraud.

FCPS employees may sign-up for the training on MyPDE.

Upcoming Events

Next Audit Committee Meeting

The next Audit Committee meeting is scheduled for February 10, 2025 at 4:30 PM. Please refer to BoardDocs for meeting information once it becomes available.

Fraud, Waste, and Abuse Hotline:

(571) 423-1333 (anonymous voicemail)

InternalAudit@fcps.edu (email is not anonymous)

Online Submission Form

[Answer: Audit Evidence]

|