TTB to Publish 2 Final Rules on Monday, September 29, 2025

On Monday, September 29, 2025, we will publish two final rules in the Federal Register:

- In T.D. TTB–202, we will establish the Tryon Foothills American viticultural area (AVA). This 176-square-mile AVA is in Polk County, North Carolina. We are establishing this AVA in response to a petition from local wine industry members and following a notice of proposed rulemaking published as Notice No. 229 on January 5, 2024.

T.D. TTB–202 is currently on public inspection on the Federal Register’s website. This final rule will be effective on October 29, 2025. See Docket No. TTB–2023–0011 for all documents and comments related to the Tryon Foothills AVA.

- In T.D. TTB–203, Tobacco Product Floor Stocks Tax; Removal of Obsolete Regulations, we are removing 42 sections of TTB regulations related to the 2009 tobacco product floor stocks tax. These regulations are no longer necessary because they implement a tax that applied only to specified articles held for sale on April 1, 2009, and was required to be paid on or before August 1, 2009.

As a direct final rule, this rule will be effective on November 28, 2025, without further action, unless we receive significant adverse comment by October 29, 2025.

This final rule is also currently on public inspection on the Federal Register’s website, and you can find all documents related to it in docket No. TTB–2025–0005.

TTB Top Tips: When to Gauge Distilled Spirits

This week, we’re sharing a top tip from investigators for distillers: when to gauge your spirits!

We require distilled spirits to be gauged at numerous points in the production, storage, and removal processes to ensure accurate tax determination and regulatory compliance.

What is “gauging”?

Gauging is the determination of the quantity and the proof of distilled spirits (and, where applicable, wine or alcoholic flavoring materials). Requirements for gauging are set forth in 27 CFR Part 19, Subpart K--Gauging, including general gauging requirements, when gauges must be performed, and special rules for particular kinds of gauges.

When is gauging required?

Spirits, wine, and alcoholic flavoring materials must be gauged when required by a TTB officer, or when they are:

(a) Produced and entered for deposit;

(b) Filled into packages from storage tanks;

(c) Transferred or received in bond;

(d) Transferred between operational accounts;

(e) Mixed in the manufacture of a distilled spirits product;

(f) Mingled under § 19.329 (when wines or spirits of less than 190° of proof are mingled in a tank)

(g) Reduced in proof before bottling;

(h) Voluntarily destroyed;

(i) Removed or withdrawn from bond;

(j) Tax determined;

(k) Returned to bond; or

(l) Denatured.

See 27 C.F.R. 19.283 When gauges are required.

The specific procedures for gauging, including the types of instruments that may be used, can be found in 27 CFR Part 30--Gauging Manual. TTB’s Proofing Videos provide instruction on how to proof your spirits correctly.

A helpful way to keep track of gauges is to keep a gauging log with the information required in 27 CFR 19.618 Gauge record. Having a running log makes reporting easier and helps to ensure that you won’t miss a required gauge!

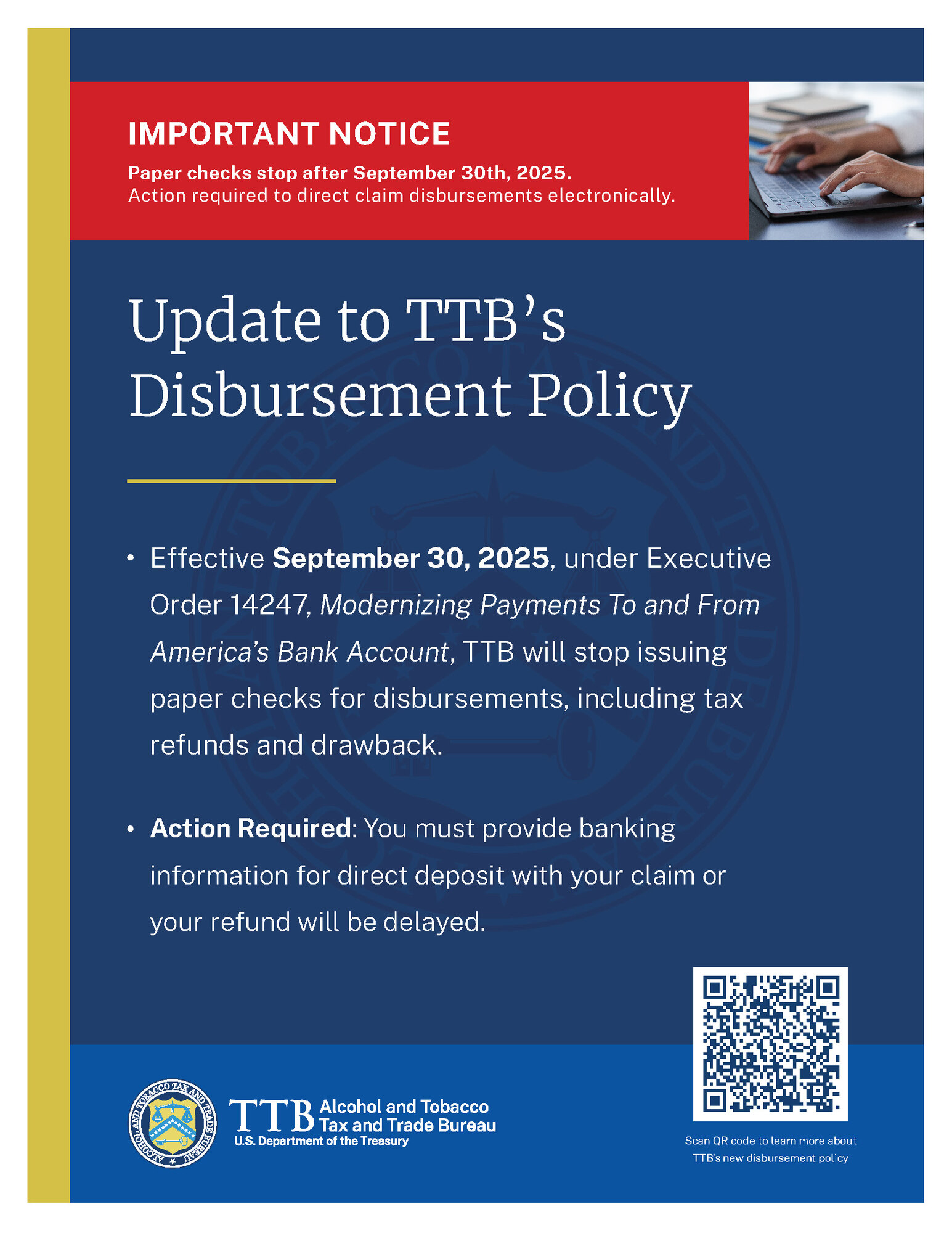

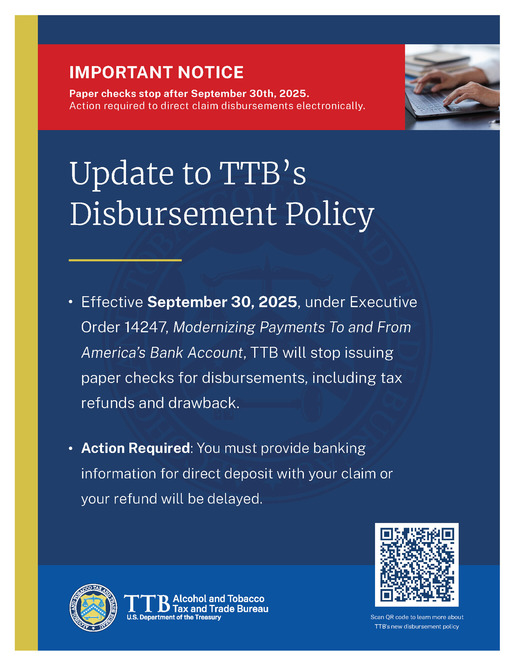

Reminder: Changes to TTB’s Outgoing Payments Effective September 30, 2025

What is happening?

Executive Order 14247 mandates the transition to electronic payments for all federal receipts and disbursements, including those to and from TTB.

We will stop issuing paper checks for disbursements, including tax refunds and drawback, on September 30, 2025.

Additionally, as soon as practicable, we will begin requiring electronic submission of all payments made to TTB.

How does this impact my tax refunds?

Unless you qualify for an exception specified in section 4 of the order, failure to provide your bank account information in connection with a claim will delay your refund.

For tax refund and drawback claims, you need to include your bank account information so that your claim can be processed, and your refund can be deposited directly into the account. Updated claim forms include sections for you to provide your account information. You can find the new forms at these links: TTB Form 5620.8 (claim – alcohol, tobacco, and firearms taxes); TTB Form 5620.7 (tobacco tax drawback); TTB Form 5110.30 (distilled spirits export drawback); TTB Form 5120.24 (wine export drawback); TTB Form 5130.6 (beer export drawback).

For CBMA importer refund claims, the system no longer offers paper checks as a payment option. If you have not already done so, please update your entity’s myTTB information to include bank account information. An entity manager, or other user authorized to access the myTTB Banking service for your entity, can add account information in myTTB by logging in and navigating to the Entity Access/Entity Management screens from the myTTB dashboard. See detailed instructions for adding an initial bank account, deleting an existing bank account, and editing a bank account nickname.

How does this impact my tax payments?

If you currently pay excise taxes with a paper check or money order, we encourage you to begin transitioning to electronic payments through Pay.gov or other electronic funds transfer as soon as possible. Note that payments made through Pay.gov (or other ACH payment method) must be made by 8:55 PM Eastern Time the business day prior to the due date.

Who do I contact with questions?

Contact TTB’s Office of Permitting and Taxation Call Center at 877-882-3277, and select option 4, or submit this contact form.

TTB's Electronic Payment Mandate Flyer with QR Code

Food and Drug Administration Notices

TTB-regulated tobacco industry members may find these notices of interest.

Agency Information Collection Activities; Submissions for Office of Management and Budget Review; Comment Requests

SOURCE: Federal Register / Vol. 90, No. 180 / Friday, September 19, 2025

AGENCY: Food and Drug Administration, Department of Health and Human Services

ACTION: Notices.

SUMMARY: The Food and Drug Administration (FDA) is announcing that three proposed collections of information have been submitted to the Office of Management and Budget (OMB) for review and clearance under the Paperwork Reduction Act of 1995.

DATE: Submit written comments (including recommendations) on the collections of information by October 20, 2025.

|