FAQ on Wine Tax: I understand that a tax credit may apply to wine I "produce" and remove. What activity counts as "produced"?

For the purpose of taking the tax credit allowed under the Craft Beverage Modernization Act (CBMA) provisions, the activities considered to be “production” are set forth below. In addition to the entire volume of wine produced by fermentation, a winery may count as production wine that has undergone the following activities:

- Sweetening

- Addition of wine spirits

- Amelioration

- Production of formula wine

On the CBMA page under General Tax Reform Questions and Answers, see FAQ TR-W8 for the definitions of these activities.

The entire volume of wine that has undergone one of these production activities would be considered “produced” for purposes of applying the tax credit. Blending that does not involve one of the operations listed above is not considered production. The eligibility for the tax credit is also subject to controlled group and single taxpayer rules similar to those in 26 U.S.C. 5051(a)(5), which may further limit the wine eligible for the tax credit. See 26 U.S.C. 5041(c)(3).

In addition, the production of sparkling wine and carbonated wine are also considered "production" for the purpose of taking the credit allowed by the law. On the CBMA page, see FAQ TR-W11. Also, we note that TTB’s interpretation of "foreign wine producer" for CBMA purposes is set forth in FAQ CB-TB11 (see CBMA Imports page under CBMA Tax Benefit Assignment FAQs).

Veterans Day Observation

Veterans Day is observed annually on November 11 to recognize all who served in the United States Armed Forces, including those who continue to serve our nation. TTB joins the White House in honoring all of our Veterans. Read President Biden’s Proclamation.

In recognition of Veterans Day, TTB offices will be closed on Friday, November 10.

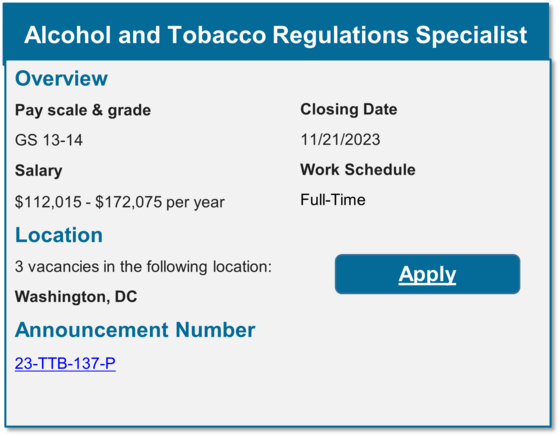

Are you interested in a career at an agency that ranks in the top 10% of Best Places to Work in the Federal Government? If yes, consider applying for this TTB job.

|