|

Set up your My Account login to protect your account

If you haven't logged in to My Account since June 2022, you need to set up a new login. Take 5 minutes to get online access to your TSP investments, verify your contact information, and help protect your account from fraud.

|

|

|

Although this level of volatility we’ve been seeing in the markets is unusual, it’s not new. History has shown us that the markets—and TSP investments—do rebound over time. Remember that investing for retirement is for the long term, and sticking to a plan with diversified investments is more likely to bring you success than trying to time the markets. By the time you react to a downturn, the markets may be moving in the opposite direction, and you could miss out on significant gains. We’ve seen it again and again: Participants who stick to their long-term goals during market downturns can end up with tens of thousands more dollars in savings over time.

Sincerely,

Your TSP

|

|

Summary of contents

- Your TSP account is yours to keep, even after you leave service

- Have you noticed? TSP expenses lower in 2024

- Jargon for a bargain: benchmark index

- Free TSP webinars

- Add TSP account maintenance and security to your spring-cleaning checklist

- First quarter account statements in My Account

|

|

Your TSP account is yours to keep, even after you leave service

What do you do with your TSP money after you leave federal or uniformed service? Some participants have told us they didn’t even know that staying with the TSP was an option. You can leave your money safely in your TSP account until you’re ready to use it, as long as you maintain the minimum account balance. Staying with the TSP means your investments can continue to grow through compound earnings in low-cost TSP funds.

Rest assured that your TSP money is secured for you by federal law (5 U.S. Code § 8437). Money in TSP accounts is held in trust and “may not be used for, or diverted to, purposes other than for the exclusive benefit of the employee” or their beneficiary. When creating the TSP, Congress emphasized this: “The employee owns it, and it cannot be tampered with by any entity.” Your money in the TSP is even protected if you’re ever sued or need to file for bankruptcy.

And you always have control of how you invest your money in your TSP account. You can log in to My Account to monitor and change your investments, request a withdrawal, and access important Plan information. Although you can’t make payroll contributions after you leave service, you can roll over money from other eligible retirement plans to consolidate your savings in your TSP account and track your nest egg more easily.

One more thing to consider: Keeping your account open keeps your options open. If you take all your money out of your TSP account, you won’t have a TSP account anymore. Once you close a TSP account, you can’t put money back in unless you rejoin service in a position that’s eligible to contribute to the TSP.

Whatever you decide to do with your TSP savings, it’s important that you have all the information you need to make the best decision for you. You can find details about everything—contributions, loans, withdrawals, taxes, death benefits, and more—in our booklets, fact sheets, and other materials available for download on our website.

|

|

Have you noticed?

TSP expenses lower in 2024

The average cost to a TSP participant in 2024 was only 39 cents for every $1,000 invested. And that means the TSP’s expenses continue to be lower than 99% of other investment options.*

And what lower expenses really mean is that more of your money stays invested so that it can continue to grow. As part of administering the TSP solely in the interest of participants and beneficiaries, we make sure that our operations are cost-effective and efficient for you.

You can learn more about how we determine our expenses on our website. And we encourage you to visit the Department of Labor’s webpage about retirement plan fees for information about how expenses and fees affect the growth of your investments.

|

|

* As of January 2025, less than 1% of the roughly 150,000 available investment options (primary share class) on the Bloomberg Terminal reported expenses below the TSP’s highest 2024 total expense ratio. We exclude funds that reported ratios of 0.00%, since these often hold options that do charge expenses.

|

|

Jargon for a bargain

benchmark index

When we talk about investing in the TSP, there’s some finance jargon we just can’t avoid. Here’s a brief review of what we mean when we talk about a benchmark index and why it’s important to know for managing your TSP investments.

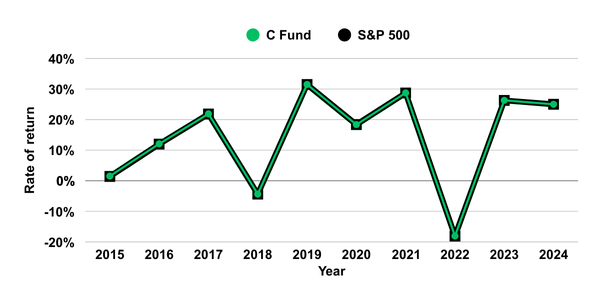

Simply put, an index is a broad collection of stocks or bonds designed to match the performance of a particular market. For example, the Standard & Poor’s 500 (S&P 500) is an index of large U.S. companies.

An index fund is an investment fund that attempts to track the investment performance of an index. The TSP’s index funds are the F, C, S, and I Funds.

And a benchmark index is the specific index that an index fund attempts to track. For example, the C Fund's investment objective is to match the performance of the S&P 500 Index, so the S&P 500 is the benchmark index for the C Fund.

This chart shows that the C Fund’s performance has matched the S&P 500 so closely over the past decade that it looks like one line:

|

|

You can compare all the TSP index funds to their benchmarks with a charting tool on our website. |

|

Free TSP webinars

Thousands of TSP participants join our free webinars every month!

Our official TSP trainers host free webinars on a variety of TSP topics and always include time to answer your specific questions. We add new sessions throughout the year, so check frequently to find times that work for you.

|

|

|

TSP webinar recordings on YouTube!

You can now watch recordings of TSP webinars on our YouTube channel. If the live webinars don’t fit your schedule, or you’d like to review specific topics on your own, we have you covered.

|

|

Add TSP account maintenance to your spring-cleaning checklist

With long-term investment plans like the TSP, it’s true that you don’t need to check your account frequently. It’s still a good idea to log in periodically and make sure that your information is up to date and that your investment choices support your goals.

Here’s your TSP account maintenance checklist:

-

Update your mailing address—How you update your mailing address depends on whether you still work for the federal government. You can also add an alternate mailing address to your profile and choose which address should receive mail from the TSP.

-

Add or update direct deposit information—You can submit financial institution information by logging in to My Account.

-

Add or check your beneficiary designation—You should designate a person or persons, your estate, or a trust to receive your TSP account after your death.

-

Check your investment election—Make sure that money coming into your account goes into the TSP funds that meet your investment goals.

-

Check your investment allocation—Make sure that money already in your account is invested in funds that match your risk profile.

-

Consider adding an account lock for extra protection—An account lock prevents new loan, withdrawal, and distribution requests without a 10-digit unlock key that you create.

|

|

First quarter statements in My Account

Your first quarter TSP statement covers account activity for January 1–March 30, 2025. You'll receive an email when your statement is available online in My Account. If you have postal mail selected as your delivery preference in your current My Account profile, you’ll also receive a copy of your quarterly statement by mail.

Request a custom statement

You can generate an electronic statement in My Account at any time. After you log in, go to Account Statements from the Quick Links menu and select the date range you want for your statement. (In the TSP Mobile App, you’ll find this link in the Retirement tab.)

|

|

Was this TSP newsletter helpful?

Please complete our very short survey to provide feedback.

|

|

|

Schedule for the Thrift Savings Planner

You'll receive your TSP newsletter by email in January, April, July, and October each year.

You can unsubscribe from the Thrift Savings Planner at any time.

View this email in your browser.

Contact us

Privacy

tsp.gov

ThriftLine Service Center

C/O Broadridge Processing

P.O. Box 1600

Newark, NJ 07101-1600

|

|

|

|

|