Unreported gambling income.

Unpaid taxes on early retirement distributions.

An update on Inflation Reduction Act spending.

Here's a quick snapshot of today's reports.

The IRS Could Collect Over a Billion Dollars in Taxes From Unreported Wagering Income

Why did we do this audit?

Gambling is becoming increasingly popular, with revenues reaching an all-time high of $109 billion in 2022. Money made from gambling is generally taxable.

We evaluated the IRS’s efforts to promote income tax compliance by individuals who have received reported winnings from gambling activities and compliance by gaming operators responsible for payment of associated excise taxes on wagering.

What did we find?

The IRS has not enforced income tax filing requirements for hundreds of thousands of individuals with reported gambling winnings. We identified nearly 150,000 recipients of Forms W‑2G (the tax form used to report gambling winnings to the IRS and to individuals) reporting $13 billion in gambling winnings over a 3-year period who didn't file a tax return. In fact, 103,000 of these nonfilers were never issued a delinquency notice – the first step to bring taxpayers into compliance. Total gambling winnings for this population were $7.1 billion.

For more of our findings:

Millions of Taxpayers Took Early Retirement Distributions but Some Did Not Pay the Additional Tax, Claim an Exception, or Report the Income

Why did we do this audit?

Taxpayers have to pay a 10% additional tax for certain early retirement distributions. Taxpayers can claim an exception to the penalty (e.g., qualified higher education expenses) by filing a Form 5329. Early distributions are also subject to income taxes.

We determined whether the IRS is effectively ensuring that taxpayers comply with filing and payment requirements when they receive an early distribution from a retirement account.

What did we find?

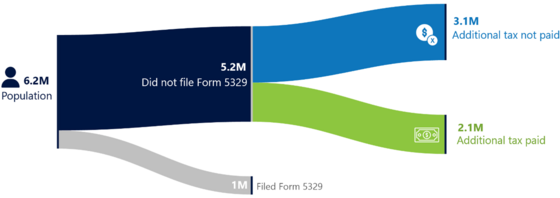

Our analysis of Tax Year 2021 tax return information identified 6.2 million taxpayers who had one or more Forms 1099-R (which shows distributions from retirement plans) indicating that the taxpayers took an early distribution that could be subject to the 10% additional tax.

- 5.2 million taxpayers didn't have an attached Form 5329.

- 3.1 million of these taxpayers didn't self-report the 10% additional tax on their tax returns.

- However, 300,000 of these taxpayers potentially rolled their funds to another retirement account (so they don’t owe the tax or need to file Form 5329).

- 2.8 million of these taxpayers received $12.9 billion in early retirement distributions.

The 2.8 million taxpayers could be subject to $1.3 billion in additional taxes and/or $322 million in Form 5329 failure to file penalties.

Additionally, approximately 2.3 million of the 2.8 million taxpayers did not properly report $11.4 billion in early distributions as taxable income.

For more of our findings:

Here's what else we issued today:

Quarterly Snapshot: The IRS’s Inflation Reduction Act Spending Through June 30, 2024

Having trouble viewing this email? View it as a Web page.

|