|

(Credit: IMF Photo/Tuane Fernandes)

By Mario Catalán, Andrea Deghi, and Mahvash S. Qureshi

Uncertainty is not as easily measured as traditional indicators like growth or inflation, but economists have built some reliable proxies.

One of the best-known gauges is the Economic Policy Uncertainty Index, which tallies how many news stories in major publications cite uncertainty, the economy, and policy. Others track the difference between published economic data and what economists previously projected.

With measures like these still elevated after years of disruption from the pandemic, the surge in inflation, fraying geopolitics and war, climate disasters and rapidly evolving technologies, we now have a better understanding of how greater uncertainty can threaten financial stability. It can exacerbate risks of financial market turmoil, delay consumption and investment decisions by people and businesses, and prompt lenders to tighten the credit supply.

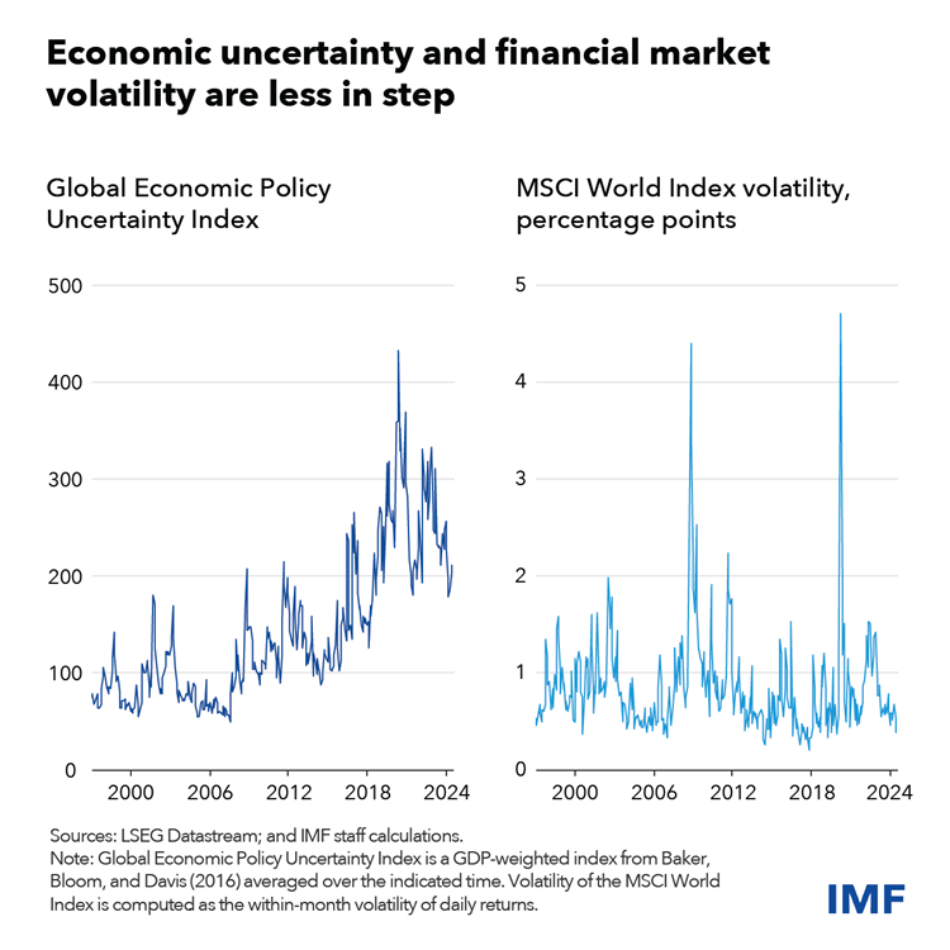

One important observation is that uncertainty about the economy may not always be in step with uncertainty reflected in financial markets. As we show in a chapter of the Global Financial Stability Report, disconnects between high economic uncertainty and low financial market volatility can persist over time. But if a shock brings market volatility roaring back, it can have much broader implications for the economy.

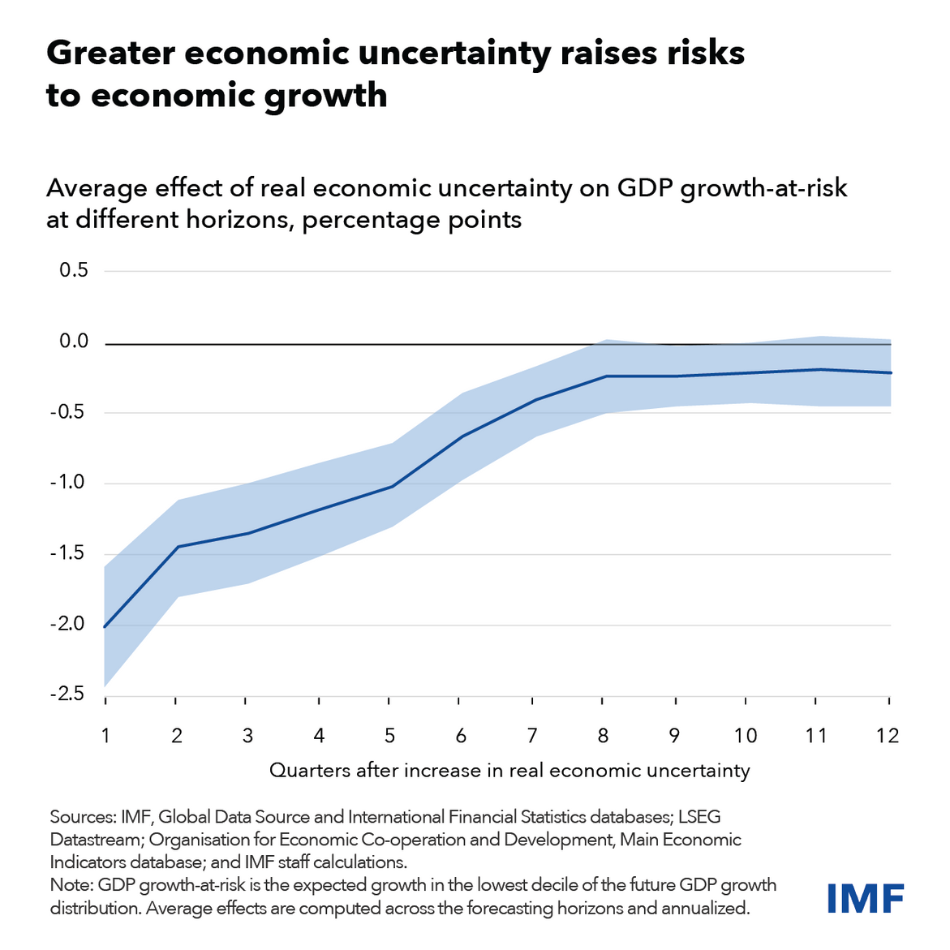

If measures of economic uncertainty were to climb like they did during the global financial crisis, then what we consider as the lowest decile of potential outcomes for economic growth—otherwise known as downside tail risk—would drop by 1.2 percentage points. This means that if the global economy was projected to grow by 0.5 percent in an adverse scenario, it would now be expected to contract by 0.7 percent.

These economic impacts can vary across countries. These effects also can be amplified when public and private debt levels are elevated relative to the size of a given economy.

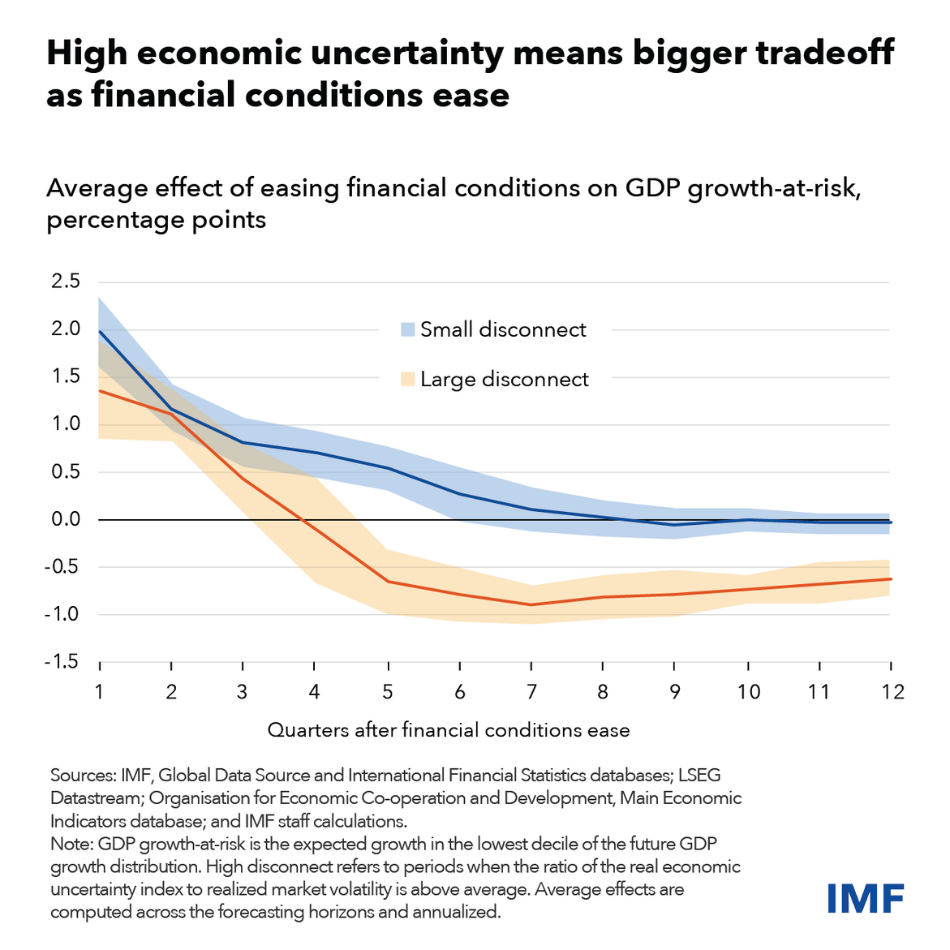

More generally, high economic uncertainty can amplify what we call the macro-financial stability tradeoff associated with loose financial conditions. When financial conditions become easier, expectations for economic growth typically go up and downside risks to the economy in the first year are reduced. That’s because of factors like lower interest rates, higher asset valuations, narrower credit spreads and reduced stock market volatility. But easy financial conditions can increase debt vulnerabilities, which worsen downside risks to economic growth down the road.

Our analysis shows that a disconnect between the economy and the market increases the chances of a sudden jump in financial market volatility and a big drop in asset prices following an adverse shock.

The potential harms from economic uncertainty are important for policymakers to recognize also because they can have cross-border spillover effects through trade and financial linkages. These spillover effects have the potential to trigger international financial contagion.

Policymakers should help provide more certainty by enhancing the credibility of their frameworks through, for example, adopting fiscal and monetary policy rules backed by strong institutions. In addition, greater transparency and well-designed policy communication frameworks can better guide market expectations—making policy decisions, and their transmission to the real economy, more predictable.

As high uncertainty exacerbates the effects of debt vulnerabilities on the real economy, policymakers should proactively use adequate macroprudential policies to limit those risks. This is particularly relevant when financial conditions are loose and appear disconnected from elevated uncertainty about the broader economy. In addition, fiscal policies should prioritize sustainability to keep elevated public debt levels from raising borrowing costs that in turn risk undermining macro-financial stability.

—This blog is based on Chapter 2 of the October 2024 Global Financial Stability Report, “Macrofinancial Stability Amid High Global Economic Uncertainty.”

|