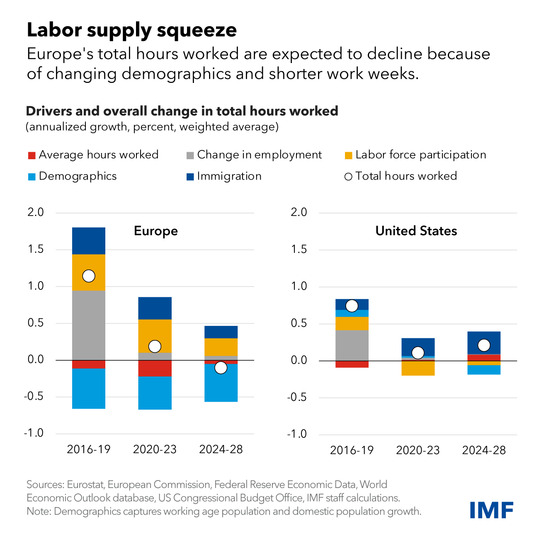

Over the past decade, Europe’s labor force participation grew relatively rapidly. Even if this trend continues, the labor supply could decline by 0.1 percent annually over the next five years as the population ages, population growth slows, and the shortening of working weeks continues. By contrast, the US labor supply is expected to grow by 0.2 percent as immigration and longer working hours more than compensate for a deterioration in demographics.

The scope to offset these labor market trends in Europe is limited. Proposals to increase retirement ages further may run into political opposition. There is also little scope to increase average working hours because shorter work weeks are gaining popularity.

What must policymakers do? There is a fine line between aiding economic recovery and banishing stubbornly high inflation. Central banks must watch for upside risks to inflation and closely monitor wage settlements and their consistency with productivity trends. A marked divergence would be worrisome. The mix of monetary and fiscal policy should remain appropriately tight to bring inflation back to target.

At the same time, structural reforms to increase productivity are becoming critical. Doing so would both lower inflationary labor-market pressures and raise longer-term economic growth potential. Boosting the labor supply by allowing workers to work more hours, making it simpler to transition between jobs, equipping new generations for future jobs, reskilling workers, and facilitating the integration of migrant workers all have an important role to play.

—See the European Department’s recent blog outlining its latest economic outlook for the region: Europe Must Succeed in Restoring Price Stability.