|

By Pierre-Olivier Gourinchas

The global economy is poised to slow this year, before rebounding next year. Growth will remain weak by historical standards, as the fight against inflation and Russia’s war in Ukraine weigh on activity.

Despite these headwinds, the outlook is less gloomy than in our October forecast, and could represent a turning point, with growth bottoming out and inflation declining.

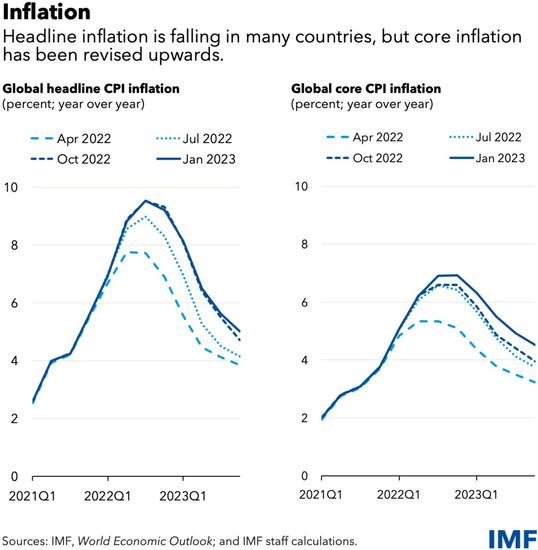

Economic growth proved surprisingly resilient in the third quarter of last year, with strong labor markets, robust household consumption and business investment, and better-than-expected adaptation to the energy crisis in Europe. Inflation, too, showed improvement, with overall measures now decreasing in most countries—even if core inflation, which excludes more volatile energy and food prices, has yet to peak in many countries.

Elsewhere, China’s sudden re-opening paves the way for a rapid rebound in activity. And global financial conditions have improved as inflation pressures started to abate. This, and a weakening of the US dollar from its November high, provided some modest relief to emerging and developing countries.

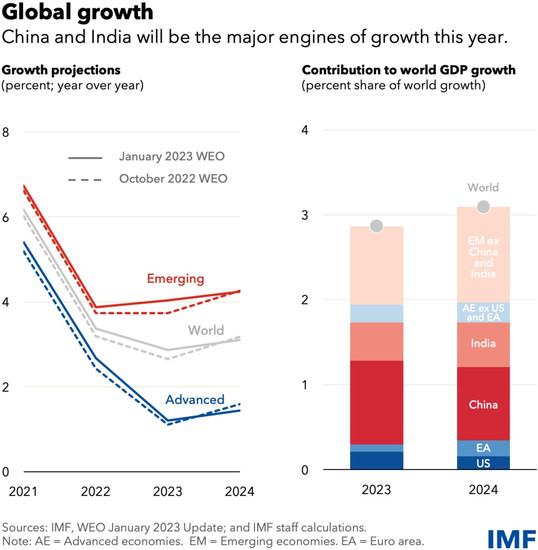

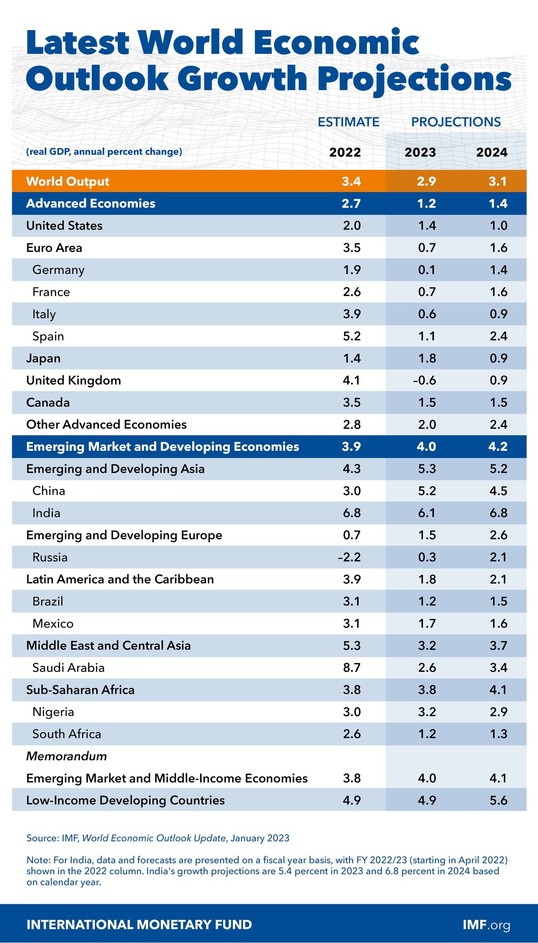

Accordingly, we have slightly increased our 2022 and 2023 growth forecasts. Global growth will slow from 3.4 percent in 2022 to 2.9 percent in 2023 then rebound to 3.1 percent in 2024.

For advanced economies, the slowdown will be more pronounced, with a decline from 2.7 percent last year to 1.2 percent and 1.4 percent this year and next. Nine out of 10 advanced economies will likely decelerate.

US growth will slow to 1.4 percent in 2023 as Federal Reserve interest-rate hikes work their way through the economy. Euro area conditions are more challenging despite signs of resilience to the energy crisis, a mild winter, and generous fiscal support. With the European Central Bank tightening monetary policy, and a negative terms-of-trade shock—due to the increase in the price of its imported energy—we expect growth to bottom out at 0.7 percent this year.

Emerging market and developing economies have already bottomed out as a group, with growth expected to rise modestly to 4 percent and 4.2 percent this year and next.

The restrictions and COVID-19 outbreaks in China dampened activity last year. With the economy now re-opened, we see growth rebounding to 5.2 percent this year as activity and mobility recover.

India remains a bright spot. Together with China, it will account for half of global growth this year, versus just a tenth for the US and euro area combined. Global inflation is expected to decline this year but even by 2024, projected average annual headline and core inflation will still be above pre-pandemic levels in more than 80 percent of countries.

The risks to the outlook remain tilted to the downside, even if adverse risks have moderated since October and some positive factors gained in relevance.

On the downside:

- China’s recovery could stall amid greater-than-expected economic disruptions from current or future waves of COVID-19 infections or a sharper-than-expected slowdown in the property sector

- Inflation could remain stubbornly high amid continued labor-market tightness and growing wage pressures, requiring tighter monetary policies and a resulting sharper slowdown in activity

- An escalation of the war in Ukraine remains a major threat to global stability that could destabilize energy or food markets and further fragment the global economy

- A sudden repricing in financial markets, for instance in response to adverse inflation surprises, could tighten financial conditions, especially in emerging market and developing economies

On the upside:

- Strong household balance sheets, together with tight labor markets and solid wage growth could help sustain private demand, although potentially complicating the fight against inflation

- Easing supply-chain bottlenecks and labor markets cooling due to falling vacancies could allow for a softer landing, requiring less monetary tightening

Policy priorities

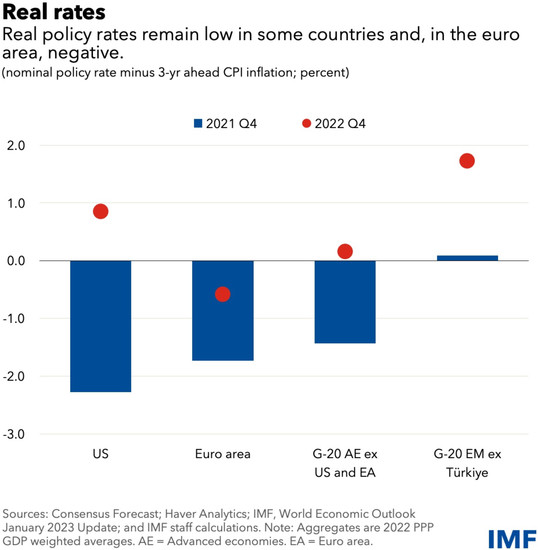

The inflation news is encouraging, but the battle is far from won. Monetary policy has started to bite, with a slowdown in new home construction in many countries. Yet, inflation-adjusted interest rates remain low or even negative in the euro area and other economies, and there is significant uncertainty about both the speed and effectiveness of monetary tightening in many countries.

Where inflation pressures remain too elevated, central banks need to raise real policy rates above the neutral rate and keep them there until underlying inflation is on a decisive declining path. Easing too early risks undoing all the gains achieved so far.

The financial environment remains fragile, especially as central banks embark on an uncharted path toward shrinking their balance sheets. It will be important to monitor the build-up of risks and address vulnerabilities, especially in the housing sector or in the less-regulated non-bank financial sector. Emerging market economies should let their currencies adjust as much as possible in response to the tighter global monetary conditions. Where appropriate, foreign exchange interventions or capital flow measures can help smooth volatility that’s excessive or not related to economic fundamentals.

Many countries responded to the cost-of-living crisis by supporting people and businesses with broad and untargeted policies that helped cushion the shock. Many of these measures have proved costly and increasingly unsustainable. Countries should instead adopt targeted measures that conserve fiscal space, allow high energy prices to reduce demand for energy, and avoid overly stimulating the economy.

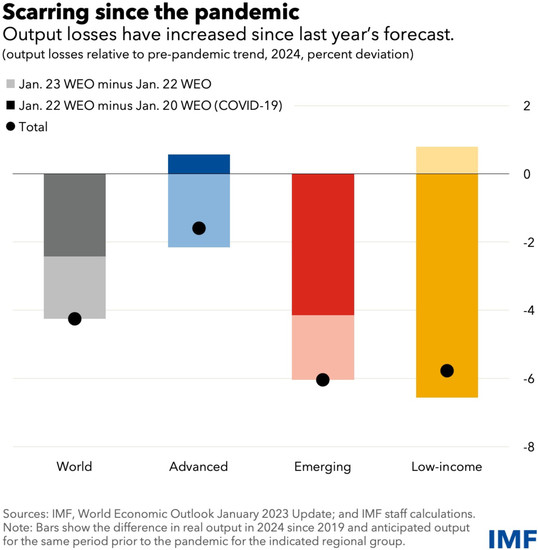

Supply-side policies also have a role to play. They can help remove key growth constraints, improve resilience, ease price pressures, and foster the green transition. These would help alleviate the accumulated output losses since the beginning of the pandemic, especially in emerging and low-income economies.

Finally, the forces of geoeconomic fragmentation are growing. We must buttress multilateral cooperation, especially on fundamental areas of common interest such as international trade, expanding the global financial safety net, public health preparedness and the climate transition.

This time around, the global economic outlook hasn’t worsened. That’s good news, but not enough. The road back to a full recovery, with sustainable growth, stable prices, and progress for all, is only starting.

|