|

By Bo Li and Nobuyasu Sugimoto

The already volatile world of crypto has been upended anew by the collapse of one its largest platforms, which highlighted risks from crypto assets that lack basic protections.

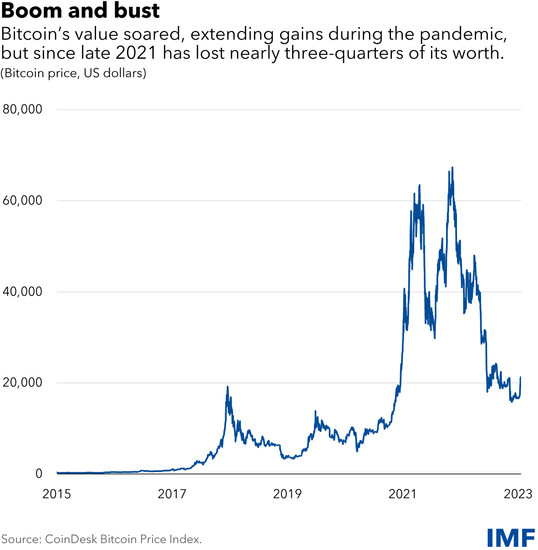

The losses punctuated an already perilous period for crypto, which has lost trillions of dollars in market value. Bitcoin, the largest, is down by almost two-thirds from its peak in late 2021, and about three-quarters of investors have lost money on it, a new analysis by the Bank for International Settlements showed in November.

During times of stress, we’ve seen market failures of stablecoins, crypto-focused hedge funds, and crypto exchanges, which in turn raised serious concerns about market integrity and user protection. And with growing and deeper links with the core financial system, there could also be concerns about systemic risk and financial stability in the near future.

Many of these concerns can be addressed by strengthening financial regulation and supervision, and by developing global standards that can be implemented consistently by national regulatory authorities.

Two recent IMF reports on regulating the crypto ecosystem are especially timely amid the severe turmoil and disruption in many parts of the crypto market and the repeated cycles of boom and bust for the ecosystem around such digital assets.

Our reports address the issues noted above at two levels. First, we take a broad approach, looking across key entities that carry out the core functions within the sector, and hence, our conclusions and recommendations apply to the entire crypto asset ecosystem.

Second, we focus more narrowly on stablecoins and their arrangements. These are crypto assets that aim to maintain a stable value relative to a specified asset or a pool of assets.

New challenges

Crypto assets, including stablecoins, are not yet risks to the global financial system, but some emerging market and developing economies are already materially affected. Some of these countries are seeing large retail holdings of, and currency substitution through, crypto assets, primarily dollar-denominated stablecoins. Some are experiencing cryptoization—when these assets are substituted for domestic currency and assets, and circumvent exchange and capital control restrictions.

Such substitution has the potential to cause capital outflows, a loss of monetary sovereignty, and threats to financial stability, creating new challenges for policy makers. Authorities need to address the root causes of cryptoization, by improving trust in their domestic economic policies, currencies, and banking systems.

Advanced economies are also susceptible to financial stability risks from crypto, given that institutional investors have increased stablecoin holdings, attracted by higher rates of return in the previously low interest rate environment. Therefore, we think it’s important for regulatory authorities to quickly manage risks from crypto, while not stifling innovation.

Specifically, we make five key recommendations in two Fintech Notes, Regulating the Crypto Ecosystem: The Case of Unbacked Crypto Assets and Regulating the Crypto Ecosystem: The Case of Stablecoins and Arrangements, both published in September.

1. Crypto asset service providers should be licensed, registered, and authorized. That includes those providing storage, transfer, exchange, settlement, and custody services, with rules like those governing providers of services in the traditional financial sector. It’s particularly important that customer assets are segregated from the firm’s own assets and ring-fenced from other functions. Licensing and authorization criteria should be well defined, and responsible authorities clearly designated.

2. Entities carrying out multiple functions should be subject to additional prudential requirements. In cases where carrying out multiple functions might generate conflicts of interest, authorities should consider whether entities should be prohibited to do so. Where firms are permitted to, and do carry out multiple functions, they should be subject to robust transparency and disclosure requirements so authorities can identify key dependencies.

3. Stablecoin issuers should be subject to strict prudential requirements. Some of these instruments are starting to find acceptance beyond crypto users, and are being used as a store of value. If not properly regulated, stablecoins could undermine monetary and financial stability. Depending on the model and size of the stablecoin arrangement, strong, bank-type regulation might be needed.

4. There should be clear requirements on regulated financial institutions, concerning their exposure to, and engagement with, crypto. If they provide custody services, requirements should be clarified to address the risks arising from those functions. The recent standard by Basel Committee on Banking Supervision on the prudential treatment of banks’ crypto assets exposures recently is very welcome in this respect.

5. Eventually, we need robust, comprehensive, globally consistent crypto regulation and supervision. The cross-sector and cross-border nature of crypto limits the effectiveness of uncoordinated national approaches. For a global approach to work, it must also be able to adapt to a changing landscape and risk outlook.

Containing user risks will be difficult for authorities around the world given the rapid evolution in crypto, and some countries are taking even more drastic steps. For example, sub-Saharan Africa, the smallest but fastest growing region for crypto trading, nearly a fifth countries have enacted bans of some kind to help reduce risk.

While broad bans might be disproportionate, we believe targeted restrictions offer better policy outcomes provided there is sufficient regulatory capacity. For instance, we can restrict the use of some crypto derivatives, as shown by Japan and the United Kingdom. We can also restrict crypto promotions, as Spain and Singapore have.

Still, while developing global standards takes time, the Financial Stability Board has done excellent work by providing recommendations for crypto assets and stablecoins. Our Fintech Notes draw many of the same conclusions, a testament to our close collaboration and shared observations on the market. For its part, the IMF will continue to work with global bodies and member nations to help leading policy makers working on this topic to best serve individual users as well as the global financial system.

—This blog reflects research contributions by Parma Bains, Fabiana Melo, and Arif Ismail.

|