|

By Krishna Srinivasan

The global economic outlook has darkened, and growth across Asia and the Pacific is poised to slow further amid the continuing impact of Russia’s invasion of Ukraine and other shocks.

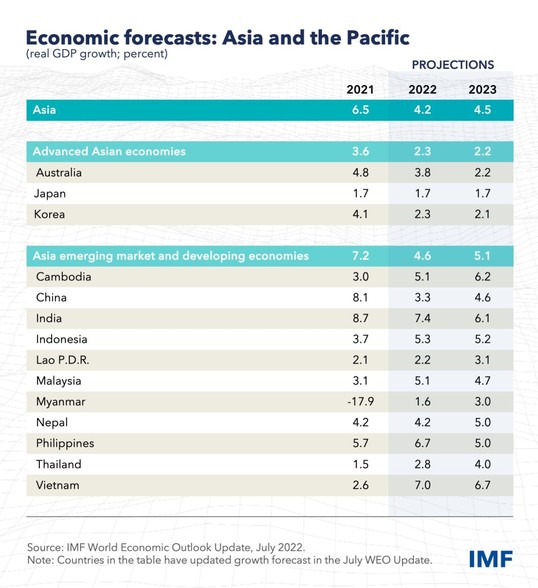

Economic growth in Asia and the Pacific is projected to decelerate to 4.2 percent this year, 0.7 percentage points less than we forecasted in April and slower than the 6.5 percent growth in 2021. We lowered our 2023 forecast to 4.6 percent, down by 0.5 percentage points.

Risks that we highlighted in our April forecast—including tightening financial conditions associated with rising central bank interest rates in the United States and commodity prices surging because of the war in Ukraine—are materializing. That in turn is compounding the regional growth spillovers from China’s slowdown.

China slowdown deepens

China, Asia’s largest economy, saw a significant deceleration in the second quarter as the zero-COVID policy prompted lockdowns for major cities and supply-chain hubs. Accordingly, our full-year growth forecast is lowered to 3.3 percent from 4.4 percent in April, and we expect 4.5 percent growth next year, a reduction of 0.6 percentage points.

Such a decline in activity, which also reflects a prolonged and intensifying slump in the real estate sector, is likely to have sizeable spillovers on regional trading partners. Japan and Korea, the two largest regional economies integrated closely with global supply chains and China, will also see growth slow on weaker external demand and disruptions to supply chains.

But despite China’s recent slowdown, signs of a rebound in economic activity are emerging as some pandemic restrictions on mobility are now being gradually eased. The resilience of manufacturing and rebound in tourism is supporting a gradual rebound in Malaysia, Thailand and the Pacific island countries.

Financial conditions tighten

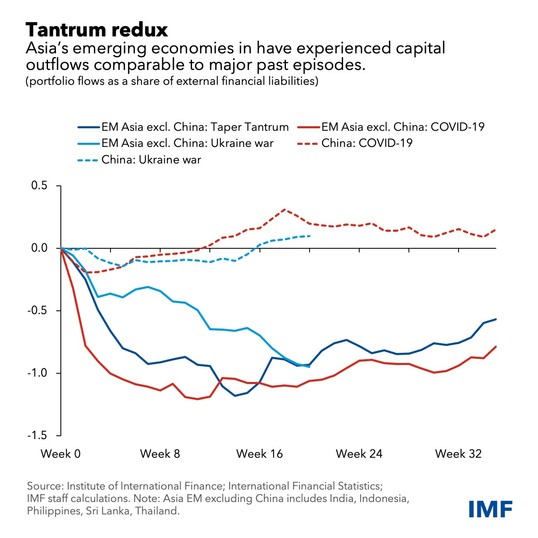

Most emerging market economies in Asia, excluding China, have experienced capital outflows comparable to those in 2013, when the Federal Reserve hinted it might taper bond buying sooner than previously expected, causing global bond yields to rise sharply. The outflows have been especially large for India: $23 billion since Russia’s invasion of Ukraine. Outflows have also occurred from some advanced Asian economies such as Korea and Taiwan Province of China, as the Fed signals continued rate hikes and geopolitical tensions reverberate.

Asia’s share of total global debt has increased from 25 percent before the global financial crisis to 38 percent post-COVID, raising the region’s susceptibility to changes in global financial conditions. Sri Lanka is an extreme case where the run up in debt became unsustainable and the economy lost access to global capital markets, leading to a default on its external obligations.

Ramifications of war

Furthermore, increased trade policy uncertainty and a fraying of supply chains, which contribute to the trend toward geoeconomic fragmentation, is expected to delay the economic recovery and exacerbate scarring from the pandemic in Asia—one of the biggest beneficiaries of decades of deepening global trade and financial integration.

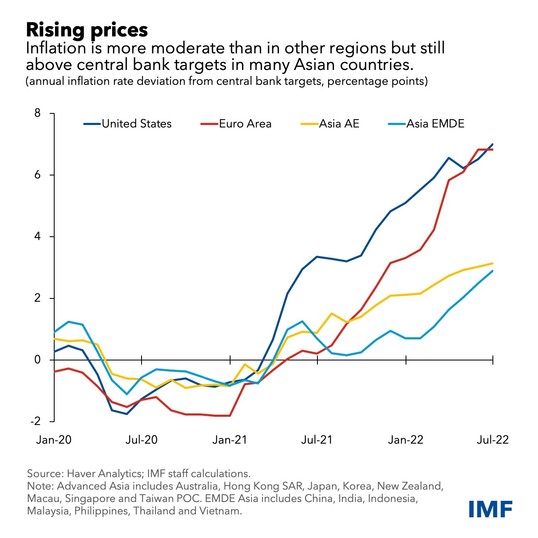

While growth is weakening, Asian inflation pressures are rising, driven by a global surge in food and fuel costs resulting from the war and related sanctions. That hits the poor and vulnerable the hardest, who are least able to cope, hurting consumption and raising the chances of social unrest, as seen in Sri Lanka, and in other countries.

Rising prices

Asia’s growing inflation pressures remain more moderate compared with other regions, but price increases in many countries have been moving above central bank targets.

Targeted fiscal support

Fiscal policy will need to tighten in countries facing elevated debt levels, providing a complement to monetary efforts to tame inflation. At the same time, targeted and temporary fiscal transfers to support vulnerable people facing renewed shocks, especially from high energy or food prices, is necessary.

Such fiscal support must be budget-neutral in most cases, funded by raising new revenues or reorienting budgets to avoid adding debt or working against monetary policy. Exceptions to this are China and Japan, provided medium-term fiscal policies remain anchored.

Beyond this, global and regional collaborative solutions that reduce trade policy uncertainty, roll back damaging trade restrictions, and avoid the most severe fragmentation scenarios are urgently needed to boost productivity and improve people’s living standards. Economic reforms over the next two to three years should aim to increase aggregate supply to tackle rising inflation, address longer-term challenges such as climate change adaptation, invest in human capital, enhance the green transition, and promote digitization.

Integrated, multifaceted, tailored response

In sum, several economies will need to raise rates rapidly as inflation is broadening to core prices, which exclude the more volatile food and energy categories, to prevent an upward spiral of inflation expectations and wages that would later require larger hikes to address if left unchecked.

At the same time, further rate rises will squeeze budgets for consumers, companies and governments that took on substantial debt during the pandemic.

While precise policy advice will differ for each country, flexible exchange rates alone may not suffice and be feasible in all countries, and other measures such as foreign exchange interventions, macroprudential policies, and capital-flow management may be useful tools to help anchor expectations and manage systemic risks.

The Fund has recently developed the Integrated Policy Framework to guide economic policy making exactly under circumstances such as this. The Fund also remains a committed partner to countries to help weather the storm on the horizon through its financing function.

Countries should not wait until it is too late—either to adjust their policy mix where necessary or to rebuild their external financing buffers where appropriate.

|