|

The war in Ukraine and sanctions on Russia are causing substantial economic spillovers, notably for energy.

Oil prices have climbed, but increases have largely been contained thanks to spare production capacity in some countries and strategic petroleum reserves in others.

Brent crude, the global oil benchmark, rose to a seven-year high around $100 before the invasion sent it surging to more than $130. It has since pared gains amid pandemic lockdowns in China, the biggest oil importer, that may weigh on economic growth there.

For some, rising oil prices

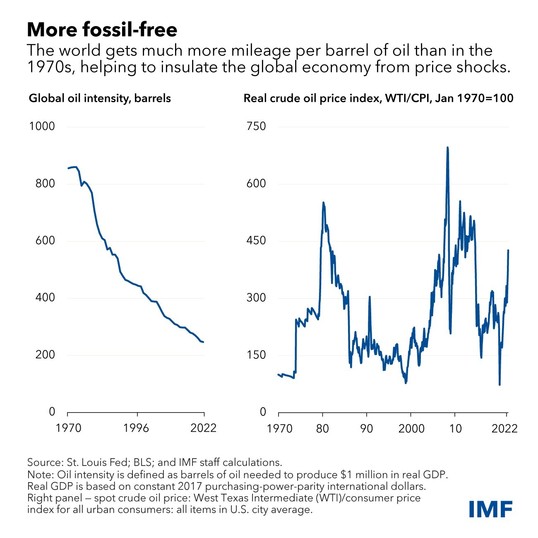

Memories of the high inflation and slow growth that followed—known as stagflation—have fueled concerns about a possible repeat. Importantly, though, times have changed.

As the Chart of the Week shows, the world relies less on oil, easing any potential shocks. Economists track oil intensity by comparing how many barrels are needed to produce $1 million in gross domestic product, and this measure was about 3.5 times higher than current levels when crude prices almost tripled between August 1973 and January 1974.

Another factor is today’s generally lower prevalence of wage-setting mechanisms that automatically adjust worker pay based on inflation. This reduces upward pressure on prices.

Central banks, too, have changed since the 1970s. More are independent today, and the credibility of monetary policy has broadly strengthened over the intervening decades.

We expect global growth to be close to the pre-pandemic average of 3.5 percent, even after our April World Economic Outlook lowered projections, but it still could slow more than forecast, and inflation could turn out higher than expected. This may be most salient for parts of Europe, given their relatively higher reliance on Russian energy imports.

|