|

Dear Colleague,

In today's edition we focus on Special Drawing Rights, the political economy of climate change, challenges facing fragile and conflict states, the economics of social unrest, IMF support for Lebanon, the Kyrgyz Republic and COVID-19, and much more. With that, let's begin.

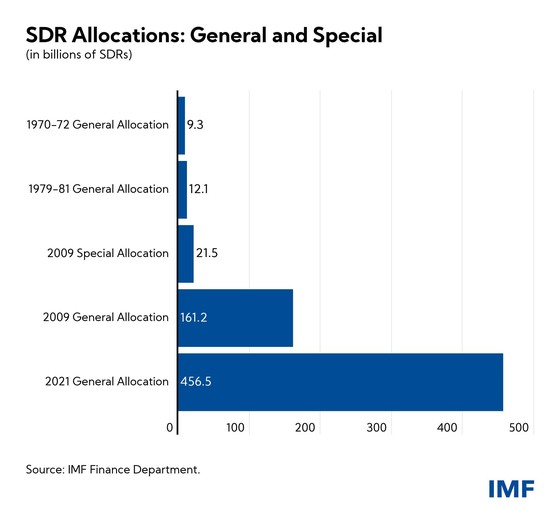

Earlier this week, the Board of Governors of the IMF approved a general allocation of Special Drawing Rights (SDRs) equivalent to US$650 billion (about SDR 456 billion). A move which will help boost global liquidity.

IMF Managing Director Kristalina Georgieva described it as a "historic decision" and "a shot in the arm for the global economy at a time of unprecedented crisis."

"The SDR allocation will benefit all members, address the long-term global need for reserves, build confidence, and foster the resilience and stability of the global economy. It will particularly help our most vulnerable countries struggling to cope with the impact of the COVID-19 crisis,” she added.

The decision could also be used to support low-income countries as IMF members countries that have strong external positions have the option to voluntarily channel part of their SDRs to scale up lending for low-income countries through the IMF’s Poverty Reduction and Growth Trust (PRGT).

THE POLITICAL ECONOMY OF CLIMATE CHANGE POLICIES

Few issues have sparked more attention than how to avoid environmental and human catastrophe from climate change. But even in the wake of massive public protests and an ambitious agenda since the 2015 Paris Agreement, governments are wary of the political costs of enacting climate mitigation policies.

Recent IMF research by Davide Furceri, Michael Ganslmeier, and Jonathan D. Ostry identified strategies that can minimize or even eliminate such challenges. In the first analysis of its kind, researchers combined information on the political aftermath (governmental popular support) of policy changes with information on the policy changes themselves in a sample of 31 OECD countries.

They find that climate change policies—especially market-based measures such as a carbon tax on fossil fuels, which are the most effective to limit pollution levels—are likely to face opposition not only from energy-using industries, but from the public at large.

Interested in learning more? Read the full blog here.

In a new article for F&D, the IMF's Philip Barrett, and Sophia Chen write that economic analysis can shine a revealing light on the causes and consequences of social unrest.

The past decade was marked by a series of high-profile social protests—the Arab Spring, Black Lives Matter, the Gilets Jaunes, and Occupy Wall Street, to name just a few. Yet while there has been a lot of soul-searching about their causes and consequences, and even though many commentators have pointed their fingers at economic forces, the economics profession has been relatively slow to respond. Indeed, rigorous quantitative economic analysis of social unrest is scant, with evidence limited to isolated cases until recently. However, a new body of IMF staff research is filling this gap by analyzing the risks and economic costs of social unrest.

A key challenge when researching social unrest—defined as protests, riots, and other forms of civil disorder and conflict—is identifying when such events have occurred. Although sources of information are available, many are sporadic or are inconsistent in their coverage.

To address these shortcomings, the authors have constructed the Reported Social Unrest Index, based on press coverage of social unrest (Barrett and others 2020). This provides a consistent, monthly measure of social unrest for 130 countries from 1985 to the present.

Interested in reading the full article? Check it out here.

HOW TO ESCAPE THE PERILS OF FRAGILITY

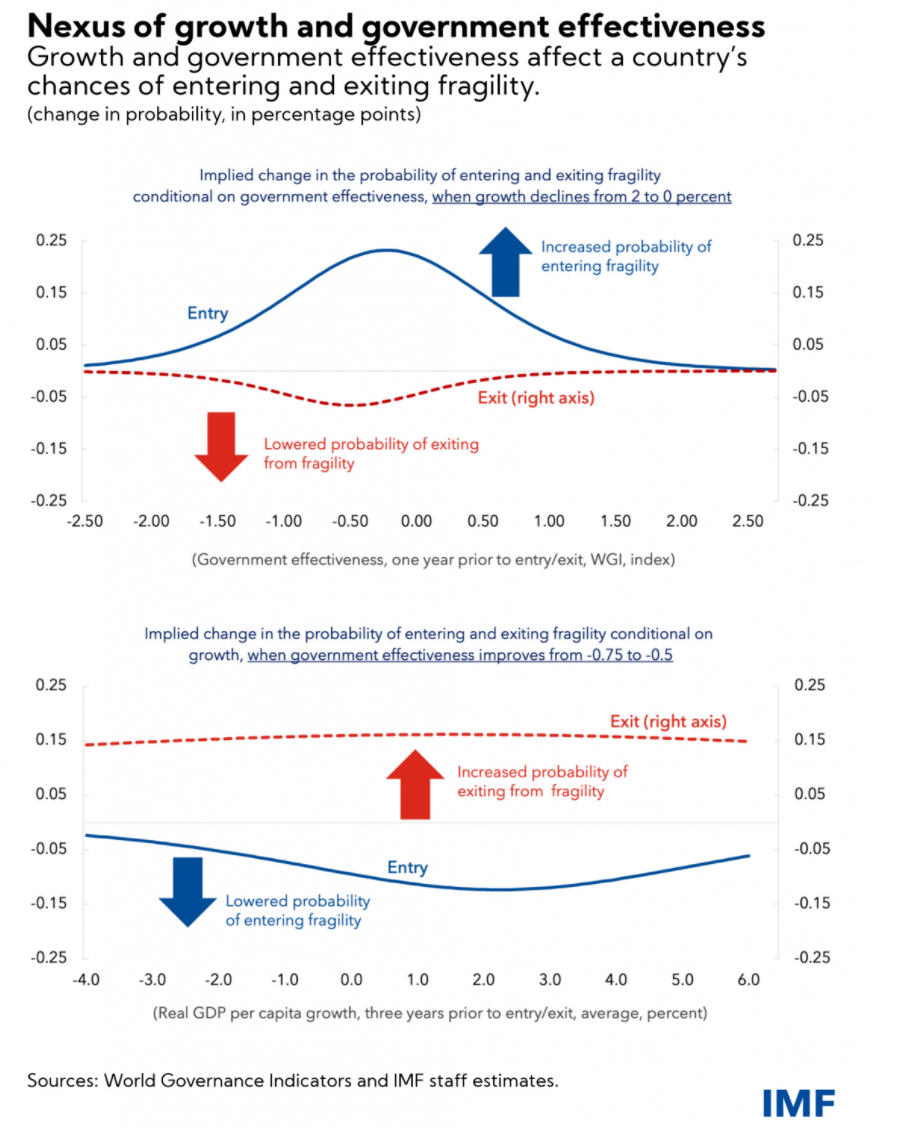

Already facing huge development needs, the COVID-19 pandemic is exacerbating the challenges facing fragile and conflict states—a group of currently about 40 countries trapped in cycles of low administrative capacity, political instability, conflict, and weak economic performance. A new IMF staff working paper by Olusegun Akanbi, Kenji Moriyama, and Keyra Primus, which analyzes the experiences of 196 countries between 1979 and 2018, shines a light on how countries can avoid or break out of this trap.

As the chart below shows, weaker growth raises the probability of falling into fragility, particularly for countries in the middle-range of government effectiveness (measured by, e.g., the ability to collect taxes and enforce contracts). The top chart measures the change in the probability of entry into/exit from fragility when growth declines by 2 percentage points at various levels of government effectiveness.

One implication is that near-fragile countries need to implement counter-cyclical policies—such as a fiscal stimulus—to prevent sharp contractions in economic output. Counter-cyclical policies could be supported by external financing from international partners, but also needed are sound macroeconomic policies, supported by strong governance and anti-corruption measures that ensure proper use of resources to help maintain a stable economy.

Read the full blog here.

HOW THE PANDEMIC WIDENED GLOBAL CURRENT ACCOUNT BALANCES

2020 was a year of extremes. Travel all but ceased for a period. Oil prices wildly fluctuated. Trade in medical products reached new heights. Household spending shifted to consumer goods rather than services and savings ballooned as people stayed home amid a global shutdown.

Exceptional policy support prevented a global economic depression, even as the pandemic took a heavy toll on lives and livelihoods, the IMF's Martin Kaufman and Daniel Leigh write in a blog this week. The global reaction, as seen in major shifts in travel, consumption, and trade, also made the world a more economically imbalanced place as reflected in current account balances—a record of a country’s transactions with the rest of the world.

In our latest External Sector Report we found that the global reaction to the pandemic further widened global current account balances—the sum of absolute deficits and surpluses among all countries—from 2.8 percent of world GDP in 2019 to 3.2 percent of GDP in 2020. Those balances are set to widen further as the pandemic continues to rage in much of the world.

Read the entire blog here.

SUPPORTING LEBANON

At a conference attended by the French President and the UN Secretary General, the IMF's Managing Director, Kristalina Georgieva, delivered remarks on the state of the Lebanese economy and voiced her support for the people of the country:

"Since we met after the devastating explosion in Beirut last August, parts of the city have been rebuilt and there was hope back then that such a tragedy would galvanize broader political, social, and economic reform," said Kristalina Georgieva.

"Regrettably, this has not happened. On the contrary, what we are seeing is a dramatic deterioration in the living conditions for the people of Lebanon.

Many speakers highlighted the humanitarian crisis in Lebanon. Let me just add a point on the economy. It has already shrunk by nearly one-third since 2017—and it is expected to contract further in 2021–22; unemployment is through the roof. And on top of it, the pandemic continues to take its heavy toll.

It is in this context that you have brought us together, President Macron, to talk about people who have endured far too much neglect of their pressing humanitarian needs, and far too long a delay in reforming a badly weakened economy.

So for us, for the IMF, there is the urgency to act today, and the importance of a longer-term transformation of the Lebanese economy."

Interested in learning more? Click here to read her remarks in full.

HOW THE KYRGYZ REPUBLIC TACKLED THE PANDEMIC

The Kyrgyz Republic was the first country to receive IMF emergency funding to tackle the COVID-19 crisis. In a new IMF Country Focus, he mission chief, Nikoloz Gigineishvili, explains the pandemic’s impact on the economy and how the IMF supported the recovery.

How has the pandemic affected the Kyrgyz Republic?

The Kyrgyz Republic has been significantly affected by the COVID-19 pandemic and was one of the hardest-hit countries in the region. The human cost of the lives lost is immeasurable, but the shock to the economy has also been substantial. The pandemic led to the contraction of output by 8.6 percent in 2020, a substantial loss of jobs, and an increase in poverty.

The labor-intensive sectors of the economy were affected the most. Tourism fell by nearly 80 percent. Transportation, trade, and construction were also significantly impacted. On the other hand, agriculture, which is mostly family-operated and does not involve extensive human interaction in closed environments, grew by about 1 percent in 2020.

Inflation increased from 3 percent in 2019 to about 10 percent in 2020, primarily due to the depreciation of the currency and higher imported food prices. Public debt increased by 16 percentage points of GDP to 68 percent in 2020, reflecting lower output, a higher fiscal deficit, and currency depreciation. According to World Bank estimates, poverty increased from 20 percent to 31 percent as incomes declined and unemployment rose.

click here for the full article.

NEW COVID-19 DATA DASHBOARD ON VACCINES, THERAPEUTICS, DIAGNOSTICS

The Task Force on COVID-19 Vaccines, Therapeutics and Diagnostics for Developing Countries, established by the heads of the IMF, World Bank Group, WHO and the WTO just launched a new data dashboard. Through this web site, which includes a global database and country-by-country data dashboards, the Task Force is tracking and monitoring specific global and country-level gaps to support faster and more targeted solutions to accelerate access to COVID-19 vaccines, treatments and tests in developing countries.

Read the statement here.

IMF AROUND THE WORLD

The IMF issued a report which considered a request by Guinea-Bissau for a nine-month staff monitored program, while IMF staff also concluded their regular Article IV consultations with, among others, Tuvalu, Bolivia, the Federated States of Micronesia and the Kingdom of the Netherlands—Curaçao and Sint Maarten.

RESPONDING TO THE CRISIS: To date, 85 countries have received more than $113 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note. We would love to hear from you.

Sincerely,

Hyun-Sung Khang

Deputy Editor, IMF Weekend Read

HKhang@imf.org

|