|

Dear Colleague,

In today's edition we focus on the two-track pandemic recovery, digital money and cryptoassets, the pandemic needs of low-income countries, the informal economy, how the Dominican Republic is tackling COVID-19, digital financial inclusion in India and much more. On that note, let's dive right in.

WIDENING GAPS IN THE GLOBAL RECOVERY

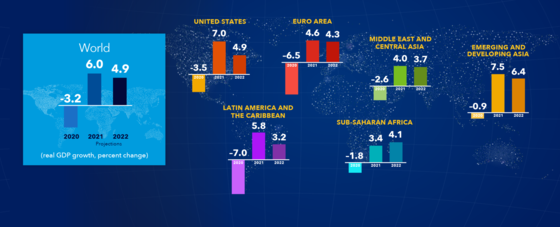

"The global economic recovery continues, but with a widening gap between advanced economies and many emerging market and developing economies," writes IMF Chief Economist Gita Gopinath in a new blog about our latest World Economic Update. "Our latest global growth forecast of 6 percent for 2021 is unchanged from the previous outlook, but the composition has changed."

Growth prospects for advanced economies this year have improved by 0.5 percentage point, but this is offset exactly by a downward revision for emerging market and developing economies driven by a significant downgrade for emerging Asia. For 2022, we project global growth of 4.9 percent, up from our previous forecast of 4.4 percent. But again, underlying this is a sizeable upgrade for advanced economies, and a more modest one for emerging market and developing economies.

While more widespread vaccine access could improve the outlook, risks on balance are tilted to the downside. The emergence of highly infectious virus variants could derail the recovery and wipe out $4.5 trillion cumulatively from global GDP by 2025. Financial conditions could also tighten abruptly amid stretched asset valuations, if there is a sudden reassessment of the monetary policy outlook, especially in the United States. It is also possible that stimulus spending in the United States could prove weaker than expected. A worsening pandemic and tightening financial conditions would inflict a double hit on emerging market and developing economies and severely set back their recoveries.

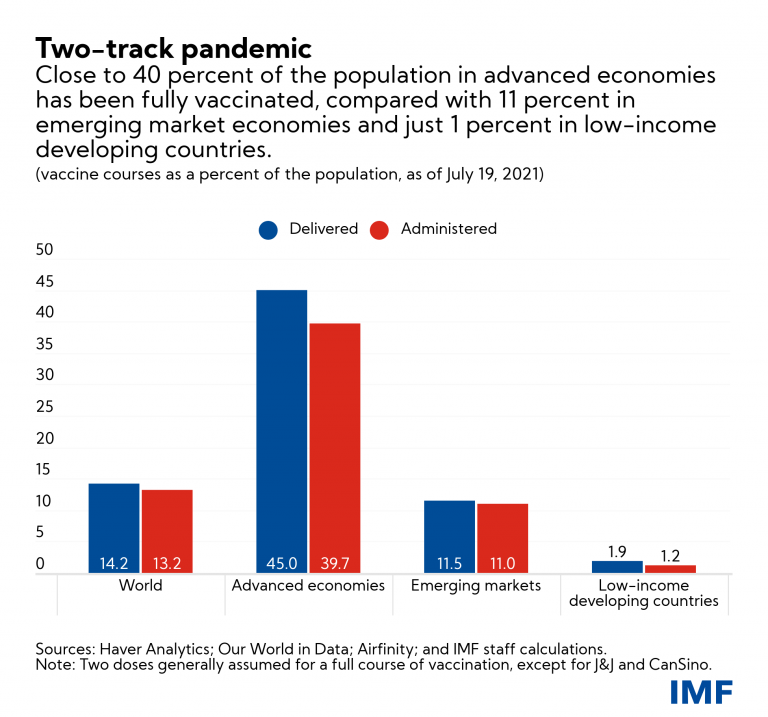

Multilateral action is needed to ensure rapid, worldwide access to vaccines, diagnostics, and therapeutics. This would save countless lives, prevent new variants from emerging, and add trillions of dollars to global economic growth. IMF staff’s recent proposal to end the pandemic, endorsed by the World Health Organization, World Bank, and World Trade Organization, sets a goal of vaccinating at least 40 percent of the population in every country by the end of 2021 and at least 60 percent by mid-2022, alongside ensuring adequate diagnostics and therapeutics at a price of $50 billion.

To achieve these targets, at least 1 billion vaccine doses should be shared in 2021 by countries with surplus vaccines, and vaccine manufacturers should prioritize deliveries to low- and lower-middle income countries. It is important to remove trade restrictions on vaccine inputs and finished vaccines and make additional investment in regional vaccine capacity to ensure sufficient production. It is essential to also make available upfront grant financing of around $25 billion for diagnostics, therapeutics, and vaccine preparedness for low-income developing countries.

Interested in learning more? Read the full blog here.

Watch Gita Gopinath provide a 60-second take on the latest update or watch the entire press conference here.

MAKING DIGITAL MONEY WORK FOR ALL

The rapid growth of digital money is a call to action. Countries should guide, and not be guided by, today’s transformations. It is also important for the IMF to engage early with countries, and usher in reforms that will contribute to the stability of the international monetary system, and foster solutions that work for all countries, the IMF's Tobias Adrian and Tommaso Mancini-Griffoli write in a new blog.

This week marked the release of two important IMF papers on the issue of digital money: one on the new policy challenges, and another on an operational strategy for the Fund to engage with countries on the digital money revolution.

What's at stake: Whether its a central bank digital currency, stablecoin, or the more wildly valuated cryptoassets, these innovations are already a reality, and growing rapidly.

The most far-reaching implications are to the stability of the international monetary system. Digital money must be designed, regulated, and provided so that governments maintain control over monetary policy to stabilize prices, and over capital flows to stabilize exchange rates. There are also implications for domestic economic and financial stability. The public and private sectors should continue to work together to provide money to end-users, while ensuring stability and security without stifling innovation.

A case study: IMF Managing Director Kristalina Georgieva and Bahamas Central Bank Governor John Rolle discussed fundamental questions about the future of digital money. The Bahamas is the first country to launch its own central bank digital currency, the "Sand Dollar."

Trust is an essential element of creating a central bank digital currency. Consumers should be confident that their money will be available when they need it, Rolle said during the event.

In a new article for F&D, the IMF's Yan Carrière-Swallow, Vikram Haksar, And Manasa Patnam write that a digital infrastructure known as the India Stack is revolutionizing access to finance.

A decade ago, India’s vibrant local markets were filled with people buying and selling goods with well-worn banknotes. Today, they are just as likely to use smartphones. Advances in digital finance mean that millions of people in the formal and vast informal economy can accept payments, settle invoices, and transfer funds anywhere in the country with just a few screen taps. COVID-19 has accelerated the use of contactless digital payments for small transactions as people try to protect themselves from the virus. These advances build on the India Stack—a comprehensive digital identity, payment, and data-management system that they write about in a new paper.

The India Stack is widening access to financial services in an economy where retail transactions are heavily cash based. A digital ID card dramatically lowers the cost of confirming people’s identities. Open-access software standards facilitate digital payments between banks, fintech firms, and digital wallets. And access to people’s personal data is controlled through consent. The expansion of digital payments, facilitated by the stack, is an important driver of economic development in India and has helped stabilize incomes in rural areas and boost sales for firms in the informal sector (Patnam and Yao 2020). Other emerging market and developing economies could learn from the experience.

Interested in reading the full article? Check it out here.

CRYPTOASSETS AS NATIONAL CURRENCY? A STEP TOO FAR

New digital forms of money have the potential to provide cheaper and faster payments, enhance financial inclusion, improve resilience and competition among payment providers, and facilitate cross-border transfers. They also require significant investment as well as difficult policy choices, such as clarifying the role of the public and private sectors in providing and regulating digital forms of money.

Some countries may be tempted by a shortcut: adopting cryptoassets as national currencies. Many are indeed secure, easy to access, and cheap to transact. We believe, however, that in most cases risks and costs outweigh potential benefits, the IMF's Tobias Adrian and Rhoda Weeks-Brown write in a blog this week.

The bottom line: As national currency, cryptoassets—including Bitcoin—come with substantial risks to macro-financial stability, financial integrity, consumer protection, and the environment. The advantages of their underlying technologies, including the potential for cheaper and more inclusive financial services, should not be overlooked. Governments, however, need to step up to provide these services, and leverage new digital forms of money while preserving stability, efficiency, equality, and environmental sustainability. Attempting to make cryptoassets a national currency is an inadvisable shortcut.

PANDEMIC RECOVERY NEEDS OF LOW-INCOME COUNTRIES

In a new blog by the IMF's Christian Mumssen and Seán Nolan, they dive deeper into why low-income countries have been hard hit by the pandemic. Their large financing needs are only likely to grow as they deal with the crisis and its economic aftermath.

The IMF has approved a far-reaching package of support that would expand their access to financial assistance at zero-interest rates, while providing stronger safeguards against taking on debt they cannot handle. For these efforts to succeed, economically stronger member countries will have to play their part.

A rapid, unprecedented response

The pandemic has dealt a severe blow to the economies of many low-income countries: output growth stopped or reversed, living standards declined, poverty increased, and a decade of solid progress is now threatened.

The IMF responded with unprecedented speed and scale. Financial assistance to 50 low-income countries reached $13 billion in 2020 compared to an average of $2 billion a year pre-pandemic: a more than sixfold increase. It also provided $739 million in grant-based debt service relief to 29 of its poorest and most vulnerable members.

Three-quarters of the new lending came from the Poverty Reduction and Growth Trust (PRGT)–the IMF’s vehicle for zero-interest loans to low-income countries. The lion’s share was in the form of emergency disbursements with limited conditionality focused on ensuring transparent use of the resources to address pandemic-related needs.

As they entered the pandemic with limited financial means, IMF assistance was crucial for many low-income countries to support lives and livelihoods.

Interested in learning more? Click here to read the full blog.

ARE YOU INFORMED ABOUT THE INFORMAL ECONOMY?

In a new IMF Country Focus, we explore how the informal economy is a global and pervasive phenomenon. Some 60 percent of the world’s population participates in the informal sector. Although mostly prevalent in emerging and developing economies, it is also an important part of advanced economies.

First, the informal economy consists of activities that have market value but are not formally registered.

The informal economy embraces professions as diverse as minibus drivers in Africa, the market stands in Latin America, and the hawkers found at traffic lights all over the world. In advanced economies, examples can range from gig and construction workers, through domestic workers, to registered firms that engage in informal activities.

The International Labor Organization estimates that about 2 billion workers, or over 60 percent of the world’s adult labor force, operate in the informal sector--at least part time. The informal economy is a global phenomenon, but there is great variation within and across countries. On average, it represents 35 percent of GDP in low- and middle- income countries versus 15 percent in advanced economies. Latin America and sub-Saharan Africa have the highest levels of informality, and Europe and East Asia are the regions with the lowest levels of informality.

Interested in learning more? Click here for the full article.

🎙️ A new book titled The Global Informal Workforce, Priorities for Inclusive Growth uses IMF research to study the causes and effects of the high levels of informality in economies across the globe. The book covers interactions between the informal economy, labor and product markets, gender equality, fiscal institutions and outcomes, social protection, and financial inclusion. In this new podcast, co-editors Corinne Deléchat and Leandro Medina say the pandemic has exposed the vulnerabilities of the informal workforce.e

Related links:

THE CHALLENGES AND OPPORTUNITIES FACING CENTRAL BANKS

Earlier this week, Banco de México Governor Alejandro Díaz de León delivered the 2021 Camdessus Lecture, followed by a one-on-one conversation with IMF Managing Director Kristalina Georgieva on the challenges and opportunities currently faced by central banks.

"Multilateral and international financial institutions have a historic opportunity to increase their catalytic role in emerging markets’ development," said Governor Díaz de León.

Watch the video here, read MD Georgieva's opening remarks here, and read Governor Díaz de León's speech here.

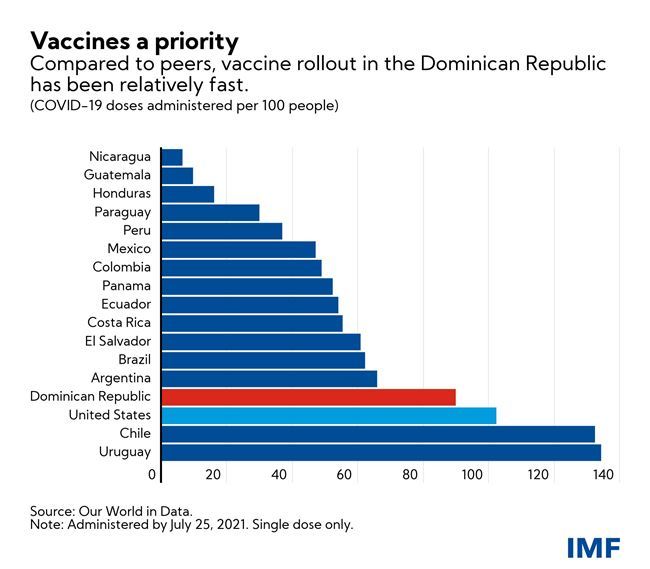

DOMINICAN REPUBLIC’S CRISIS RESPONSE AND RECOVERY

As one of the fastest-growing and most dynamic economies in Latin America and the Caribbean, the Dominican Republic entered the COVID-19 crisis in a relatively strong position, write Mariana Sans and Pamela Madrid of the IMF Western Hemisphere Department in a new country focus article. Despite the toll of the pandemic, smart policy making and continued access to markets allowed the country to implement a response plan that has put the Dominican Republic on a path to recovery.

What was the policy response to the crisis?

The country’s response has adjusted to the needs created by the pandemic. Initially, with the economy in lockdown, the response prioritized health spending and broad transfers to low-income families and the unemployed, and targeted tax relief. The Central Bank reacted decisively through interest rate cuts and ample liquidity provision that supported credit and activity. As the economy began to recover, policies became more targeted. Broad support programs ended in April 2021, but temporary social programs were gradually merged into a new social assistance program. Support to the unemployed focused on the most affected sectors, notably tourism. To support a safe reopening, new health spending focused on the rollout of vaccines. The government has set a target of immunizing 7.8 million people—over 70 percent of the population. Around 51 percent of the target population has received two vaccine doses, as of July 25, 2021.

Interested in learning more? Read the full article here.

IMF AROUND THE WORLD

The IMF Executive Board this past week approved a $553.2 million financing arrangement for Gabon under the Extended Fund Facility. The Board also completed its first review under the Precautionary and Liquidity Line arrangement for Panama for the equivalent of about $2.7 billion.

In other action this week, the Board completed third and fourth reviews of Sierra Leone's Extended Credit Facility. The Board this week also reviewed Nicaragua's Poverty Reduction Strategy.

RESPONDING TO THE CRISIS: To date, 85 countries have received more than $113 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note. We would love to hear from you.

Sincerely,

|