|

Dear Colleague,

In today's edition we focus on seizing the opportunity for a pro-growth future, trade and the recovery, how the IMF is helping low-income countries, market power and monetary policy, getting to net zero emissions, Olympic economics, and much more. On that note, let's dive right in.

📣 But first, don't forget to tune in to a conversation today at 9 a.m. ET between IMF Managing Director Kristalina Georgieva and International Labour Organization Director General Guy Ryder where they will discuss recent developments in the informal economy. The event marks the launch of a new IMF book, The Global Informal Workforce: Priorities for Inclusive Growth. Find out more about the book here.

GROWING IN A POST-PANDEMIC WORLD

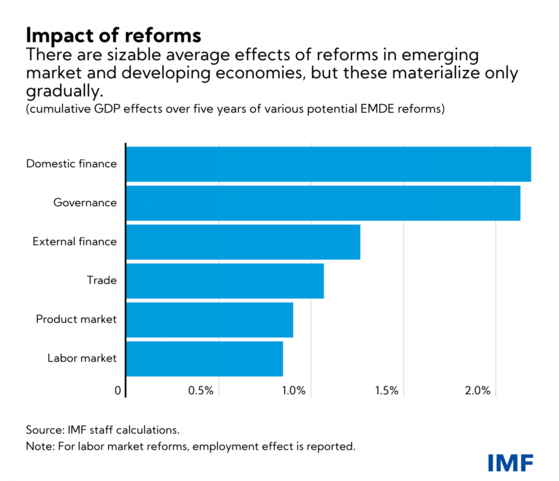

This crisis is an opportunity for policymakers to strengthen their economies for a brighter future. That means using this moment of unprecedented monetary and fiscal stimulus to support difficult reforms, such as enhanced debt restructuring mechanisms, improved labor policies, and competition policy frameworks, that could deliver years of solid growth and progress in living standards, IMF First Deputy Managing Director Geoffrey Okamoto writes in a new blog.

The IMF estimates that comprehensive growth-enhancing reforms cutting across product, labor, and financial markets could raise annual growth in GDP per capita by over one percentage point in emerging market and developing economies in the next decade. These countries would be able to double their speed of convergence to advanced economies’ living standards relative to the pre-pandemic years.

Read the full blog here.

HOW CAN TRADE SUPPORT THE RECOVERY?

The answer to that question is, first and foremost, that trade can play a role in ending the pandemic faster by getting vaccines to where they need to go. IMF Managing Director Kristalina Georgieva discussed the issue this week with Cecilia Malmström, former European Trade Commissioner now a nonresident senior fellow at the Peterson Institute.

"Trade contributes, first, by eliminating restrictions and providing facilitation for the delivery of vaccines and the necessary supplies to produce vaccines as well as therapeutics and oxygen. Trade matters by bringing manufacturers for a concerted effort together with policymakers and trade authorities," Georgieva said.

"Trade discussions matter because there is an understandable demand from developing countries for a broader platform to produce vaccines in more places," she added.

Eliminating trade restrictions on vaccines, vaccine inputs and medical supplies is a major part of a plan to end the pandemic proposed by IMF staff and supported by the World Health Organization, World Bank and World Trade Organization.

Watch the full event here.

2021 MICHEL CAMDESSUS CENTRAL BANKING LECTURE

On July 28, from 9:30 am to 10:30 am, Managing Director Kristalina Georgieva will host virtually the 2021 Michel Camdessus Central Banking Lecture. This year's lecture will be delivered by Alejandro Díaz de León, Governor of Banco de México. The lecture will be followed by a one-on-one conversation between Alejandro Díaz de León and Kristalina Georgieva. Watch the event live on IMF social media accounts and here: 2021 Michel Camdessus Central Banking Lecture

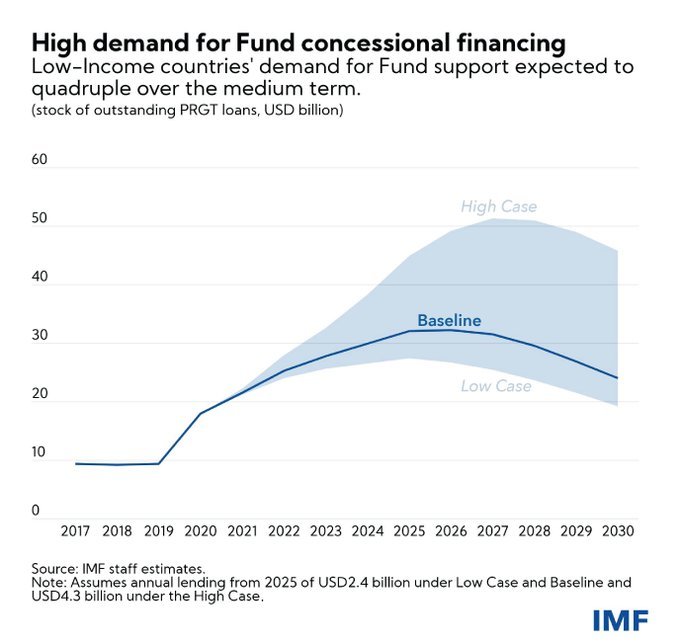

HELPING LOW-INCOME COUNTRIES RECOVER FROM THE CRISIS

Low-income countries are struggling from the effects of the pandemic and will need help if they are to secure a durable recovery. Looking ahead, the IMF has approved a number of measures that will make its Poverty Reduction and Growth Trust (PRGT)--the IMF's vehicle for zero-interest loans to low-income countries--more effective in helping countries recover from the pandemic and boost investment. Demand from low-income countries for IMF support is only expected to increase in the coming years.

These new reforms will increase the limit of how much zero-interest financing all low-income countries can access, remove the access cap altogether for the poorest countries, retain zero interest rates for all PRGT loans, and reinforce safeguards to keep low-income countries from over-indebtedness.

Read the full policy paper here.

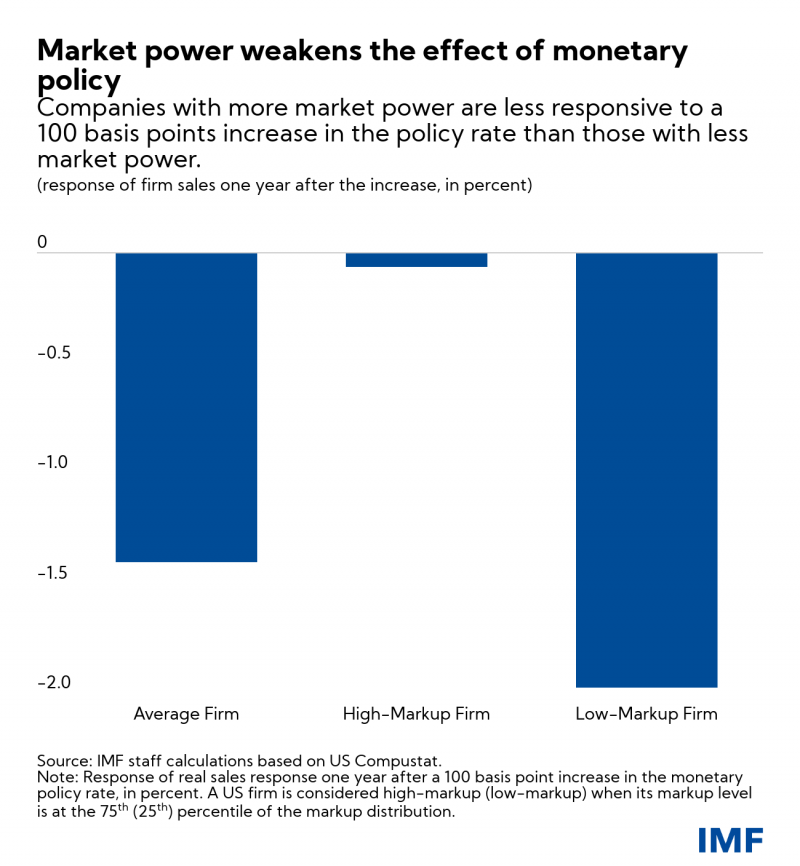

BIG COMPANIES AND MONETARY POLICY

As central banks debate whether to tighten monetary policy to fight inflationary pressures, they have to consider how much businesses and consumers will respond. The structure of the financial system and the future expectations of consumers and businesses are key drivers of how effective monetary policy actions will be. Yet there’s another, overlooked, driver: corporate market power.

New IMF staff research has found ever larger and more powerful companies are making monetary policy a less potent tool for managing the economy in advanced economies, all else equal, the IMF's Romain Duval, Davide Furceri, and Marina M. Tavares write in a new blog.

Specifically, using data for the United States and a panel of 14 advanced economies, we find that high-markup firms, aka larger and more powerful companies, respond a lot less to a monetary policy shock—an unexpected change in the policy rate—than the average firm in the economy. For example, in the US, a 100 basis point increase in the policy rate causes a low-markup firm to cut sales by about 2 percent after four quarters, while a high-markup firm barely reduces its sales. Results for the panel of advanced countries are qualitatively similar.

To find out more, read the full blog here.

GETTING TO NET ZERO EMISSIONS

There may be more attention now on climate change than ever before, but there's less time to do something about it. The carbon budget, or maximum amount of emissions allowable, to limit global warming to well below 2°C is running out quickly. More frequent and intense disasters, a decline in agricultural productivity, and rising sea levels will only grow more common if this critical goal is not met.

Reaching net zero emissions by 2050, the agreed-upon deadline for averting a dangerous global increase in temperatures, will strategy that relies on carbon pricing, a green investment plan, and measures to help people economically transition to clean energy future, the IMF's Florence Jaumotte and Gregor Schwerhoff write in a new blog.

Real numbers: Green investments are crucial to enable the transition to a low-carbon economy and support the response to carbon pricing. Reducing emissions can come with a higher upfront investment but will bring a lower cost in the long run due to a reduction in fuel consumption.

An estimated additional $6 to 10 trillion in global investments, both public and private, are needed in the next decade to mitigate climate change. This amounts to a cumulative 6-10 percent of annual global GDP.

Read the full blog here.

IMF CLIMATE INNOVATION CHALLENGE

At the IMF, climate change is now at the heart of our work on economic and financial stability, growth, and jobs. Our Climate Innovation Challenge is underway to gather answers to the question “How might we integrate climate change into economic analysis to promote green policies?” Country authorities/agencies, civil society organizations (including think tanks), and staff from the IMF, World Bank, and international organizations are invited to submit proposals that have the potential to enhance the IMF’s capacity development, policy advice, and operational impact in areas where economic and financial policies intersect with climate change. Hear from our sponsoring partner, the Swiss State Secretariat for Economic Affairs, and our technical partner, the World Resources Institute, on why you should submit your ideas. And click here to learn more about the process and timeline.

THIS WEEK IN HISTORY

On July 22, 1944 the Bretton Woods Conference concluded, giving birth to the IMF.

Representatives of 44 Allied nations, seeking to avoid the mistakes that led to depression and World War II, met to plan a new economic order built on global cooperation. They gave the Fund three critical missions: promoting international monetary cooperation, supporting the expansion of trade and economic growth, and discouraging policies that would harm prosperity.

Read more here to see how the IMF's role in history has evolved.

F&D: ARE THE OLYMPICS A VICTIM OF THEIR OWN SUCCESS?

In a new F&D online exclusive, Victor Matheson and Rob Baade examine how the Olympic Games are now routinely exceeding any reasonably expected returns for a host country and how it may be time to consider significant reforms to the way the Olympics are pursued, prepared for, and hosted.

For 125 years, the modern Olympic Games have highlighted the peak of human athletic endeavor as reflected in the International Olympic Committee’s (IOC’s) motto—“Faster, Higher, Stronger.” Host cities have gladly shared the spotlight with the world’s greatest athletes at the world’s premier athletic event, and for many years, cities competed as vigorously as the athletes themselves for the perceived honor of hosting the quadrennial Summer or Winter Olympic Games. The past decade, however, has witnessed growing popular backlash against the Olympics worldwide as exploding costs and increasingly uncertain benefits accruing to the host city have significantly dampened interest in staging the games. Without significant changes, the IOC may find itself with few partners willing to undertake the risk and expense.

Interested in learning more? Read the full article here.

THREE MORE SESSIONS FOR IMF VIRTUAL SUMMER SCHOOL

Following session 1 on inclusive growth and session 2 on debt sustainability for low income countries, the remaining three sessions will deal with monetary policy analysis and forecasting (July 28), public financial management (August 4), and financial inclusion and development (August 11).

Don’t miss out on those unique insights into some of the IMF’s flagship open online courses. You can follow the next sessions at noon ET (UTC-4) on the IMF LinkedIn account, the Twitter and Facebook feeds of IMF Capacity Development, and the IMF Institute’s YouTube Learning Channel. Find out more on the IMF Summer School watching this promo video.

IMF AROUND THE WORLD

The IMF Executive Board this week concluded Article IV economic assessment consultations with the United States, Côte d’Ivoire, Estonia, Ghana, Singapore, and Greece. The Board also recently approved a 3-year, $1.52 billion Extended Credit Facility arrangement with the Democratic Republic of the Congo.

RESPONDING TO THE CRISIS: To date, 85 countries have received more than $113 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note. We would love to hear from you.

Sincerely,

|