|

Dear Colleague,

In today's edition we focus on building resilience through adaptation, the four fault lines of the world economy, attracting private finance for Africa's development, the benefits of economic inclusion, streaming services in emerging markets, a new era of digital money, tackling the pandemic in Cyprus and much more. On that note, let's dive right in.

📣 But first, join IMF Managing Director Kristalina Georgieva and others for a conversation on international carbon price floors hosted together with the Brookings Institution. Watch the live event here, which starts at 10:00 AM ET. A new paper from IMF staff, still under discussion with the IMF Board and membership, proposes the creation of an international carbon price floor arrangement that complements the Paris Agreement. Read more about this proposal in a new blog published this morning.

RESILIENT AND SUSTAINABLE

IMF Managing Director Kristalina Georgieva this week discussed the creation of a new Resilience and Sustainability Trust that would give countries additional resources to battle the effects of climate change.

“I can tell you immediately that the very first delivery of this on-lending will be through the existing Poverty Reduction and Growth Trust that we have at the IMF. And many countries vulnerable to climate change are benefiting from it already,” she said in an event with Barbados Prime Minister Mia Mottley and Madagascar Economy and Finance Minister Richard Randriamandrato. IMF Chief Economist Gita Gopinath provided opening remarks.

A new trust in 2021? The MD said she hoped the new trust could be approved by IMF membership and launched by the end of the year, using the upcoming COP 26 conference as catalyzing event. The Resilience and Sustainability Trust would take “a little bit of time [to develop] because it is new. It is not like expanding the operations of an existing entity.”

“We would do our best to mobilize the membership towards an agreement so we can go to COP 26 and say, ‘here is an additional contribution to building a more resilient world on the foundation of multilateral cooperation, on the foundation of solidarity,’” Georgieva said.

Mottley, who the MD noted is working with the IMF to develop the new financing tool, said “to the extent that we can get some increased space to help us meet the demands, that is going to be huge.”

“We are very much encouraged by this,” said Randriamandrato. “Let's put it this way: It's a revolutionary vision as regards to how the IMF will contribute to improved global financing for low income countries.”

📺 Watch the entire event here.

THE FOUR FAULT LINES OF THE WORLD ECONOMY

In a speech by IMF Chief Economist Gita Gopinath at the APEC Structural Reform Ministerial Meeting, she talked about four fault lines of the pre-COVID world economy that the pandemic has aggravated—(1) slow progress in raising average living standards (2) highly unequal progress across demographic groups (3) high and rising public debts, and (4) insufficient global public goods—and how the pandemic has aggravated all four of these areas.

Gopinath also talked about how International cooperation is central, but to raise living standards, reduce inequality and slowly curb public debts within APEC and other economies, structural reforms are also going to be critical. While detailed reform priorities are obviously economy-specific, one overarching theme is the need to tailor them to the three phases of the pandemic—the acute, recovery and post-pandemic phases.

First, the acute phase of the pandemic

For economies that are still, or might fall back, into the acute phase of the pandemic and restrictions on activity, the priority remains to alleviate a destruction of viable jobs and firms that would leave permanent scars on our economies. This means, where fiscal space allows, a continuation of support to existing jobs and firms. For example, in response to the pandemic last year, all ASEAN-6 economies—Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam—provided liquidity support to firms including loan moratoria, subsidized lending and government guarantees, and several of them also implemented wage subsidies. These various policies have helped preserve future living standards, and they also tend to benefit disproportionately lower-skilled workers and SMEs that would be hit harder by the pandemic otherwise—historically, displaced workers who find reemployment in a different occupation experience an average earnings loss as large as 15 percent.

During the acute phase, it is also important to postpone the implementation of reforms that would pay off in normal times but could backfire in such unusual times—for example, labor market or pension reforms that increase labor supply should not be implemented while work restrictions are in place.

Read the full speech here.

F&D: A NEW ERA OF DIGITAL MONEY 💰

In a new article for F&D, the IMF's Tobias Adrian and Tommaso Mancini-Griffoli argue that digital money has the potential to transform the financial sector, and that emerging markets and lower-income countries stand to gain the most from this dramatic shift.

Broad and inexpensive access to digital money and phone-based transactions could open the door to financial services for 1.7 billion people without traditional bank accounts. And countries may grow increasingly connected, facilitating trade and market integration. The real-world impact is significant.

But with any opportunity comes risk. The passage to this new world could exclude those on the other side of the digital divide. It also opens the door to fragmentation, currency substitution, and loss of policy effectiveness. The transition must be well managed, coordinated, and soundly regulated.

Interested in learning more? Read the full article here.

HOW TO ATTRACT PRIVATE FINANCE TO AFRICA’S DEVELOPMENT

In a new blog by Luc Eyraud, Catherine Pattillo, and Abebe Aemro Selassie, they argue that African economies are at a pivotal juncture. The COVID-19 pandemic has brought economic activity to a standstill. Africa’s hard-won economic gains of the last two decades, critical in improving living standards, could be reversed.

High public debt levels and the uncertain outlook for international aid limit the scope for growth through large public investment programs. The private sector will have to play more of a role in economic development if countries are to enjoy a strong recovery and avoid economic stagnation. Heads of state from Africa made this one of their resounding messages during the recent summit on “Financing African Economies” held in Paris in May.

Infrastructure—both physical (roads, electricity) and social (health, education)—is one area where the private sector could be more involved. Africa’s infrastructure development needs are huge—in the order of 20 percent of GDP on average by the end of the decade. How can this be financed? All else equal, the main source of financing would be more tax revenue collections, something that most countries are working towards. But, given the scale of the needs, new financing sources will have to be mobilized from the international community and the private sector.

Africa is a continent that holds immense opportunity for private investors. It has a young and growing population and abundant natural resources. Cities are seeing massive growth. Many countries have launched long-term industrialization and digitalization initiatives. But significant investment and innovation are necessary to unlock the region’s full potential. Recent research published by IMF staff shows that the private sector could, by the end of the decade, bring additional annual financing equivalent to 3 percent of sub-Saharan Africa’s GDP for physical and social infrastructure. This represents about $50 billion per year (using 2020 GDP) and almost a quarter of the average private investment ratio in the region (currently 13 percent of GDP).

Click here to read the full blog.

🎙️ NEW PODCAST: A PROPOSAL TO END THE PANDEMIC

There will be no durable end to the economic crisis until enough people around the world are vaccinated against Covid-19 and its variants to put the health crisis behind us. Economist Ruchir Agarwal and IMF Chief Economist Gita Gopinath have joined forces to come up with a plan that would make that happen. In this podcast, Agarwal says the return on investment for ending the pandemic could reach $9 trillion, one of the highest-return investments ever.

Listen to the podcast here. And if you're in a hurry, skim the transcript (PDF).

THE BENEFITS OF ECONOMIC INCLUSION

Achieving inclusive growth—that is, strong and sustainable economic growth whose benefits are widely shared—is the key policy challenge of our day and thus a fundamental pillar of the IMF’s policy focus in the years ahead.

Earlier this week, on a panel for “Promoting an Inclusive Recovery,” MD Georgieva said that achieving inclusion is not only a moral imperative – it is an economic imperative for stronger growth and sustainable recovery. She then described the many ways in which the IMF promotes economic inclusion, including through taxation, social protection, access to finance, and opportunities for green growth. MD Georgieva also called to secure an insurance against the new variants by further investing in vaccinations and further supporting developing countries.

During the event, speakers also highlighted the forthcoming publication of a new book co-edited by the IMF and UC Berkeley Professor Barry Eichengreen on “How to Achieve Inclusive Growth” and the recent launch of a new IMF course on this topic.

Watch the full event here.

F&D: 🎥 FROM STREAM TO FLOOD IN EMERGING MARKETS

In our latest issue on the road ahead for emerging markets, F&D senior editor Adam Behsudi writes that streaming video offers emerging markets an avenue for content at home and around the world.

Streaming giants like Netflix, Disney+, and Amazon are growing new audiences and overlapping markets in ways never seen before. In doing so, they’ve opened burgeoning film and television industries in some of the most vibrant emerging markets to new possibilities, changing the economic calculation for producing films and redefining what can be a hit.

“What’s beautiful about it is we’re sitting on the same platform. That’s what’s exciting—being a Nollywood movie—where it’s going, what we’re sitting next to in terms of Hollywood production and it being received in that way,” said Hamisha Daryani Ahuja, a third-generation Nigerian with Indian roots who created, directed, produced, and acted in the movie that Netflix released on Valentine’s Day. Ahuja’s romantic comedy broke into Netflix’s top 10 list in the United States for a short period, generating buzz for the streaming company’s recent expansion into African content.

Interested in learning more? Click here. The PDF of this article is also available.

A THREE-POINT PLAN TO TACKLE THE PANDEMIC IN CYPRUS

In a new Country Focus, Anita Tuladhar, Estelle Xue Liu, and Ruifeng Zhang of the European Department discuss the IMF's latest economic assessment of Cyprus, outlining three key policies to strengthen the recovery from the effects of the pandemic shock.

Cyprus entered the COVID-19 crisis in a strong position, but the economy’s dependence on tourism and its high public and private debt levels made it especially vulnerable to the pandemic shock. Nevertheless, the country has avoided widespread defaults and high unemployment, thanks in part to prompt policy support and a strong capital cushion accumulated before the pandemic.

The near-term outlook points to a gradual but uneven recovery, with significant risks. Growth is projected to recover moderately to 3 percent in 2021 after output fell by 5.1 percent in 2020. However, the pace of vaccinations and potential new waves of infection remain key uncertainties.

Given this outlook, Cyprus can help guide its economic recovery from the pandemic by focusing on financial policies, fiscal support, and measures to improve productivity.

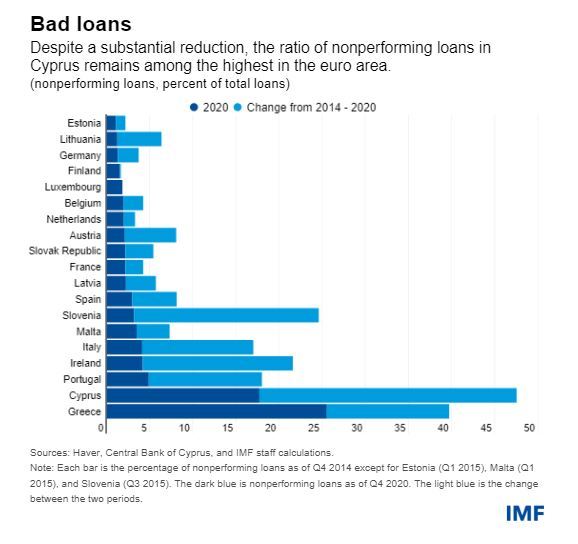

To start, the authors focus on how to address problem loans to strengthen bank balance sheets and support credit growth. While Cyprus has reduced nonperforming loans substantially, the ratio of these loans remains among the highest in the euro area. Sizable exposure to vulnerable contact-intensive sectors such as tourism and retail also poses a risk. A significant share of loans to these sectors were protected under a loan repayment moratorium, which could test the capacity of banks to cope with a possible new wave of borrower distress.

Bank supervisors should encourage continued close monitoring of borrowers’ repayment capacity to ensure prompt recognition and adequate provisioning of potential loan losses. Macroprudential buffers should be used flexibly to support both restructuring and the ability of banks to supply credit. Stronger debt restructuring and insolvency tools are vital for timely debt resolution so that firms under debt distress remain viable as policy support is gradually withdrawn. Complementary reforms in the judicial sector are also crucial to facilitate this process.

Click here to read the full Country Focus.

IMF AROUND THE WORLD

The IMF Executive Board this week concluded its fifth review of the IMF’s extended arrangement of the Extended Fund Facility for Barbados, allowing the country to draw about $24 million in additional financing from the program. The Board also announced the conclusion of Article IV economic assessments for Cyprus, Bolivia, Panama, Ireland, Denmark, Turkey, Guatemala, and Andorra.

IMF staff this week also announced the conclusion of virtual visits to Nigeria, Zimbabwe and Albania. Staff also concluded virtual Article IV missions to the Philippines, Latvia, Austria, Lithuania and Côte d’Ivoire.

RESPONDING TO THE CRISIS: To date, 86 countries have received more than $110 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note. We would love to hear from you.

Sincerely,

|