|

Dear Colleague,

We just published a new blog—please find the full text below. Translations coming soon.

The Benefits of Setting a Lower Limit on Corporate Taxation

By Aqib Aslam and Maria Coelho

On June 5, 2021, Finance Ministers from the Group of Seven major industrialized nations committed to a global minimum corporate tax rate on multinationals of at least 15 percent. While there are a number of details yet to be hammered out in broader global discussions, this historic agreement heralds an important step forward on the road to international corporate tax reform. It also highlights the role minimum taxes can play at the global level to help reverse nearly four decades of falling global corporate tax rates and reduce the incentives for large multinational firms to shift profits to low-tax jurisdictions to reduce their worldwide tax liability. Our new study examines how different types of domestic minimum tax regimes can help countries preserve their corporate tax base and mobilize revenue.

Minimum taxation over the decades

There is an unusual tension in the world of corporate taxation. On the one hand, countries compete vigorously to lure businesses and investors within their borders by offering numerous profit- and cost-based tax incentives, driving their tax rates down. On the other hand, governments decry these multinational enterprises—once they have been successfully attracted to the country—for not paying their fair share of corporate taxes, leaving the burden to fall on often-struggling local firms.

Increasingly, governments are turning to minimum taxes as a means of preserving their tax base. This is particularly true in developing countries with weaker tax administrations, which face major challenges in effectively taxing these large multinationals.

The idea of a minimum tax rate is not new. At the local level countries have been using modern forms of minimum taxation since at least the 1960s, taxing businesses on income generated based on activity undertaken within their territory. The goal of this “local” (domestic) minimum taxation is to prevent erosion of the tax base from the excessive use of what is known as “tax preferences.” These tax preferences take the form of credits, deductions, special exemptions, and allowances and usually result in a reduction in the amount of tax a corporation owes. By instituting a corporate minimum tax rate, governments guarantee a floor on the businesses’ contribution to the public purse.

Minimum taxes are typically computed using an alternative simplified tax base that avoids the complexities of the standard corporate tax base. They are often based on turnover (gross income or receipts) or assets (net or gross). A third alternative uses modified definitions for corporate income that explicitly limit the number of deductions and exemptions allowed.

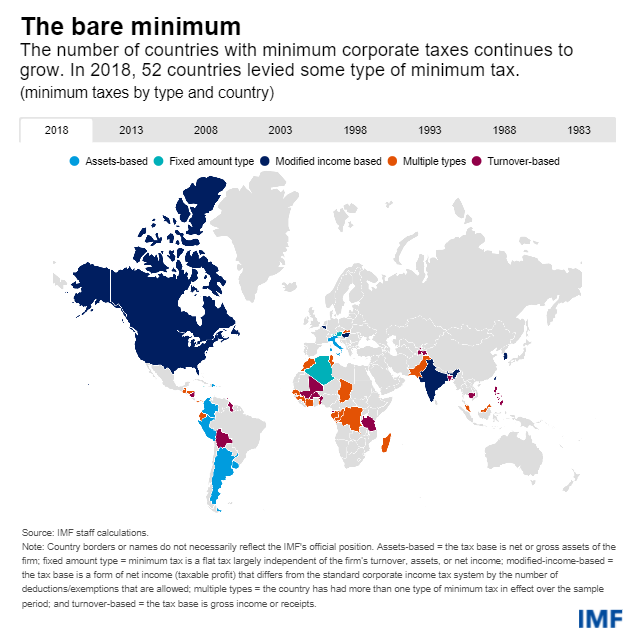

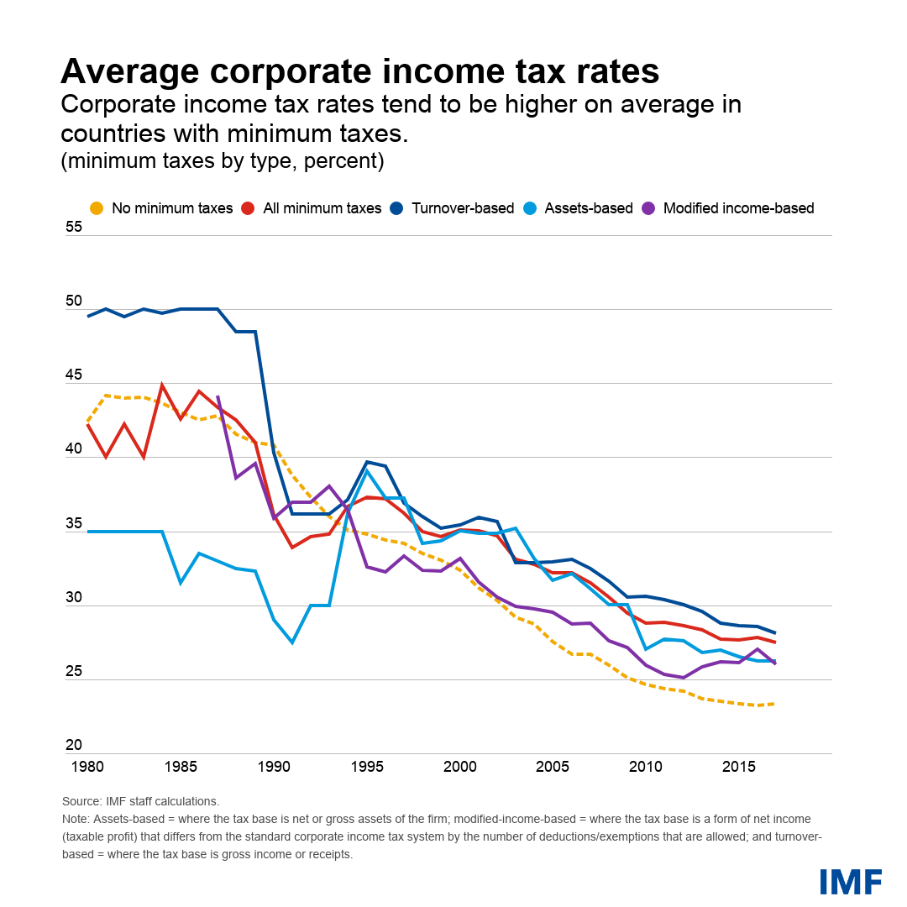

Using a new database of minimum corporate tax regimes worldwide, we show how minimum taxes have grown in popularity over the past few decades. Turnover-based minimum taxes are the most prevalent and tend to be found in countries with higher statutory corporate tax rates (the rate imposed by law). Countries that levy a minimum tax also tend to report higher corporate tax revenue as a share of GDP.

We study the impact of minimum taxes on revenue and economic activity by combining our new country panel database with firm-level data. What we find is that introducing a minimum tax is associated with an increase in the average effective tax rate—that is, the tax rate actually paid by corporations after taking into account tax breaks—of just over 1.5 percentage points with respect to turnover and around 10 percentage points with respect to profits.

Minimum taxes based on modified corporate income lead to the largest increases in effective tax rates, followed by those based on assets and turnover. Ultimately, the revenue impact also depends on the rate applied.

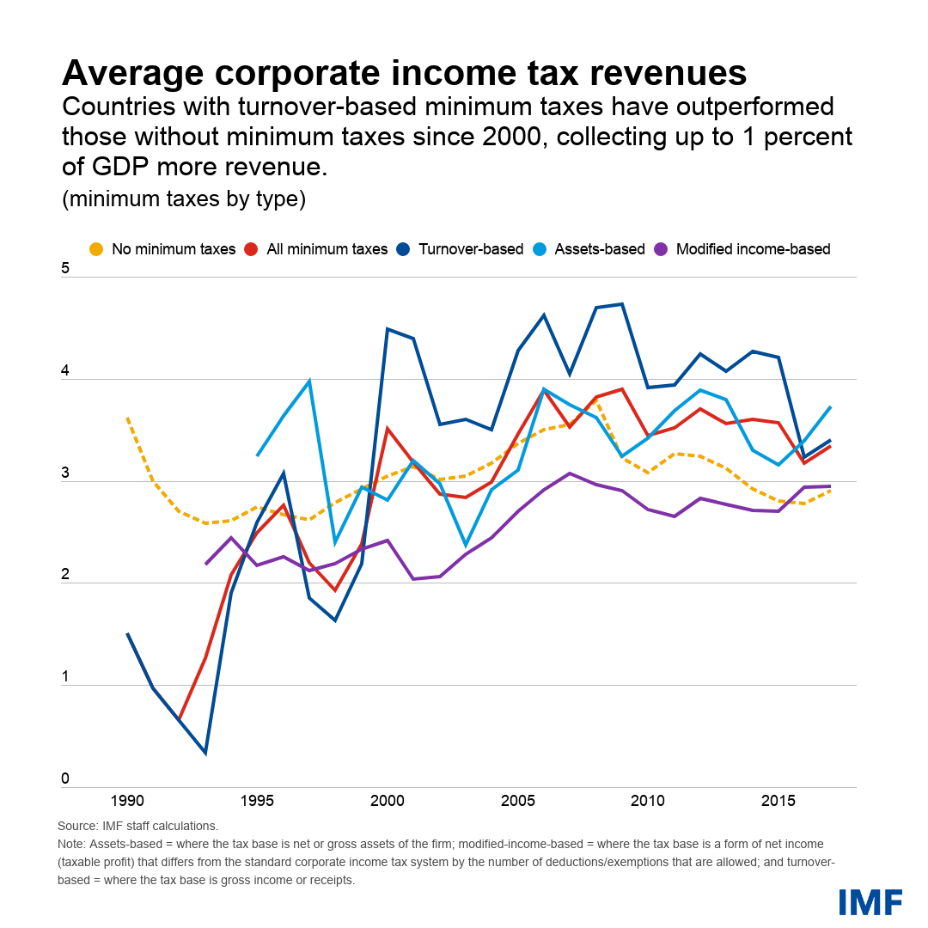

In addition, we use firm-level data to get a sense of the potential revenue that would result from the introduction of a hypothetical minimum tax of 0.5 percent on turnover and minimum tax of 1 percent on total assets. For the median country, the former could raise an additional 7 percentage points of tax revenue for governments relative to current levels and the latter almost a third more.

This translates into an average of 0.2 and 0.9 percent of GDP in additional revenue—for the median country in our sample—for a turnover-based and an assets-based minimum tax, respectively, on top of a median corporate income tax-to-GDP ratio of 2.7 percent. These results represent a significant revenue potential that merits serious policy consideration.

Fresh momentum

The agreement reached by the G7 countries on minimum taxes has provided fresh momentum to the overhaul of international tax rules led by international organizations. As part of this overhaul, the Organisation for Economic Cooperation and Development (OECD) and the G20 had proposed in late 2020 a global minimum corporate tax that would apply to profits of multinationals. Countries would still set their own local tax rates, but if a multinational company paid less than the global minimum rate in another country, that company’s home or source jurisdiction could supplement its tax liability to ensure it paid the minimum. In this way, the advantages of shifting profits to low-tax jurisdictions would be reduced.

The OECD and G20’s global proposal differs from standard local minimum taxes—it would not focus solely on income generated on activities undertaken within a country. Instead, payments would be triggered only if other countries don’t tax multinationals enough. Furthermore, the use of local minimum taxes could end up increasing as they provide a simpler alternative to the complex provisions of this proposal for a global minimum tax, which many low-income and developing countries may not have the capacity to implement.

Powerful but not perfect

Despite inefficiencies associated with local minimum taxes, they could allow countries to tap significant revenue. In this way, setting a floor on corporate taxation—at least at the local domestic level with moderate tax rates—can be a good option for countries looking to preserve revenue and prevent the erosion of their tax base without severely damaging corporate activity.

However, minimum taxes alone cannot replace reforms that broaden the corporate tax base. The proliferation of multiple rates and all sorts of special preferences within the standard corporate tax system causes costly distortions and low revenues—and encourages tax avoidance and evasion.

Tax incentives to attract multinationals are also likely to persist even after the introduction of a global minimum tax, as countries will continue to do what they can to entice foreign investment for growth and development. But the value of these incentives will decline, as multinationals will only be able to reduce their liabilities to 15 percent and not zero. And so therefore, the first best remains to tackle and remove these head on.

Aqib Aslam is an economist in the World Economic Studies Division of the IMF's Research Department.

Maria Coelho is an economist in the Tax Policy Division of the IMF's Fiscal Affairs Department.

*****

We want to hear from you! Click here for a 3-question survey on IMFBlog.

Thank you again for your interest in IMF Blog. Read more of our latest content here.

Take good care,

P.S. Are you on LinkedIn? Subscribe to our new Weekend Read visual newsletter.

_____

Surprise a colleague: forward this email

First-time reader? Sign up here

Update your profile for tailored content

View all IMF newsletters

Unsubscribe from IMF Blog here

|