|

Dear Colleague,

In today's edition we focus on a $50 billion plan to bring the pandemic under control, financing for African economies, multilateralism in the context of vaccines, taxation and climate change, monitoring pandemic-related spending for transparency and accountability, and "back to basics" economic explainers. On that note, let's dive right in.

A PROPOSAL TO END THE COVID-19 PANDEMIC

Many countries and institutions have stepped up in the global fight against the COVID-19 pandemic. Yet, more than a year into the public health crisis, new cases worldwide are higher than ever.

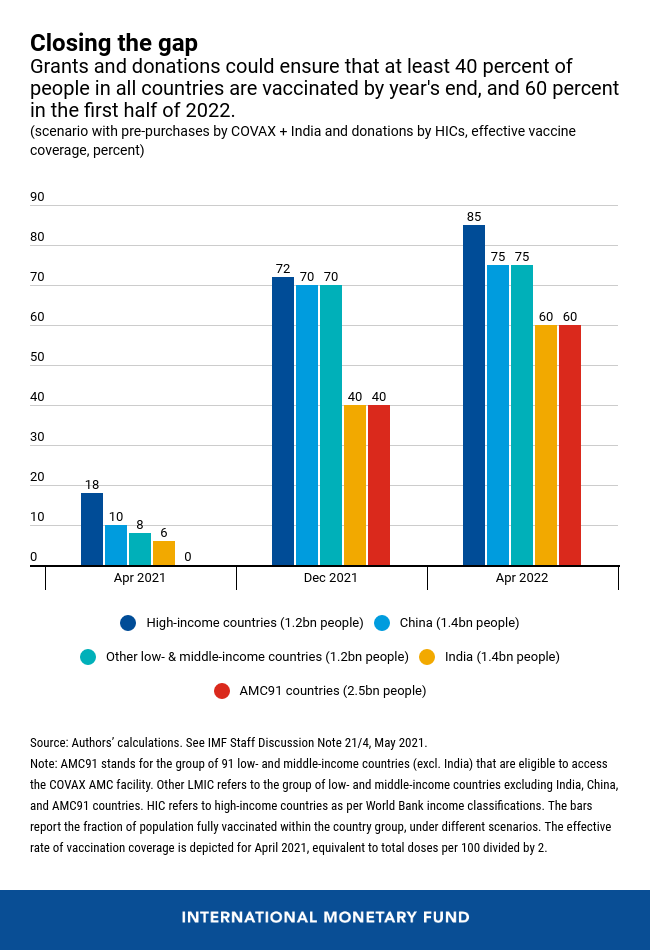

Building on the work of the World Health Organization, World Bank, Gavi, African Union and others, the proposal sets targets, estimates financing requirements, and lays out pragmatic action, the IMF's Kristalina Georgieva, Gita Gopinath, and Ruchir Agarwal. write in a new blog.

Three broad elements:

(1) Vaccinating of at least 40 percent of the global population by end-2021 and at least 60 percent by the first half of 2022. To do so requires additional upfront grants to COVAX, donating surplus doses and free cross-border flows of raw materials and finished vaccines.

(2) Insuring against downside risks such as new variants that may necessitate booster shots. This means investing in additional vaccine production capacity by 1 billion doses, scaling up genomic surveillance and supply-chain surveillance, and contingency plans to handle virus mutations or supply shocks.

(3) Managing the interim period where vaccine supply is limited with widespread testing and tracing, therapeutic and public health measures, and, at the same time, ramping up preparations for vaccine deployment together with any approved dose-stretching strategies.

What will it cost?

The proposal’s total cost of around $50 billion would include grants, national government resources, and concessional financing.

There is a strong case for grant financing of at least $35 billion. The good news is G20 governments have already identified as important to address the $22 billion grant funding gap noted by the Access to COVID-19 Tools (ACT) Accelerator. This leaves an estimated $13 billion in additional grant contributions needed.

The remainder of the overall financing plan—around $15 billion—could come from national governments, potentially supported by COVID-19 financing facilities created by multilateral development banks.

Read the blog here, and read the full paper here.

SUMMIT ON THE FINANCING OF AFRICAN ECONOMIES

"Africa’s leaders and Africa’s friends have a common objective: for Africa to return to the remarkable development progress we have witnessed before the pandemic. And to take full advantage of the tectonic shifts in the global economy toward digital-driven, low-carbon and climate resilient growth," said Managing Director Kristalina Georgieva at the Summit on the Financing of African Economies hosted by French President Emmanuel Macron.

One of the primary goals of the summit, attended by some two dozen African heads of state and financial institutions, was to accelerate the COVID-19 vaccine rollout and create the fiscal breathing room for African nations, which will face a spending shortfall of some $285 billion.

There is urgency to focus on financing Africa. Last year, the pandemic-caused recession shrank the GDP of the Continent by 1.9 percent – the worst performance on record. This year, we project global growth at 6 percent, but only half that – 3.2 percent – for Africa.

This is a dangerous divergence. It ought to be the reverse: Africa needs to grow faster than the world – at 7 to 10 percent – to meet the aspirations of its youthful populations, and become more prosperous and more secure. Together we have avoided a much worse economic crisis. Now, we must build on this initial momentum to bring the pandemic to a durable end and boost growth in Africa. In other words, to secure a fair shot: a shot in the arm, for everyone, everywhere, and a shot at a better future.

What is the price tag of this fair shot? At the IMF, we estimate Africa’s additional financing needs for an adequate COVID response at around $285 billion through 2025. Of this,$135 billion is for low-income countries. This is the bare minimum. To do more – to get African nations back on their previous path of catching up with wealthy countries – will cost roughly twice as much.

Three priorities for action:

(1) Ending the pandemic everywhere: the economic case is overwhelming: for a cost of $50 billion, faster vaccination can result in higher global output of $9 trillion between now and 2025.

(2) Bilateral and multilateral development financing including grants and concessional loans ought to go up. We recognize exceptional times call for exceptional measures. Our membership backs an unprecedented new allocation of Special Drawing Rights of $650 billion – by far the largest in our history. Once approved, which we intend to achieve by the end of August, it will directly and immediately make about $33 billion available to our African members. It will boost their reserves and liquidity, without adding to their debt burden

(3) Actions at home – a crisis is an opportunity for transformational domestic reforms that increase domestic revenue, improve public services, and strengthen governance. For instance, digitalization can improve tax administration and revenue collection, and the quality of public spending. And with radical transparency, Africa can tap into new sources of finance – such as carbon offsets.

Read the speech here and watch the video of the event here (starting at 35min).

P.S. Speaking of climate offsets, IMF economists and their counterparts from UNDP assist government officials from the Caribbean on attracting climate finance, using green budgeting, promoting climate resilient infrastructure, and having a better understanding of climate risks. Learn more here.

MONITORING PANDEMIC-RELATED SPENDING

The IMF presses for better governance through greater transparency, and has sought specific governance measures for countries receiving IMF financing during the crisis. These include commitments to publish pandemic-related procurement contracts and the beneficial ownership of companies awarded these contracts, as well as COVID-19 spending reports and audit results.

In a new blog by Chady El Khoury, Jiro Honda, Johan Mathisen, and Etienne Yehoue, they write that a year into the emergency response, information is becoming available on the progress in implementing these governance measures in pandemic-related spending.

- On publication of contract information, most of the commitments have or are in the process of being met, including, for example, in the Dominican Republic, Guinea, Nepal, and Ukraine. In some countries, capacity constraints contribute to limited progress. In these cases, the IMF is providing capacity development to support implementation.

- Collecting and publishing the beneficial ownership of contracting companies is a measure that aims to deter corruption, including by facilitating the detection of potential conflicts-of-interest involving public officials. It requires bidding companies to provide the names of the people with effective control over a company, that is the “beneficial owners.” This information is provided to the procurement agency, which must publish it.

Implementation of this innovative practice has proven challenging in some cases, with only half of the countries (including Benin, Ecuador, Jordan, Malawi, and Moldova) having implemented this commitment or made substantial progress toward it.

However, such commitments made in the context of IMF financing during the pandemic have helped spur some countries, such as Kenya and the Kyrgyz Republic, to adopt this reform on a permanent basis. That is, beyond just pandemic-related spending.

- On audits of emergency spending, the deadline for conducting ex-post audits is typically set at 3-12 months after the end of the fiscal year. Accordingly, it is too early to assess implementation—most audits are in preparation based on existing systems.

However, some countries, such as Jamaica, Honduras, Maldives, and Sierra Leone have already taken early action by conducting risk-based, real-time audits. Where needed, the IMF is also stepping up its capacity development to help supreme audit institutions fulfill their responsibility, while also supporting efforts to ensure that such information is easily retrievable.

- On reporting of pandemic-related spending, most countries are, or will shortly begin, publicly reporting on execution of this spending.

-

Safeguard assessments are being undertaken rapidly, with the pace of these assessments doubling after the pandemic’s onset.

Click here to learn more.

If you're interested in the IMF's work more broadly on improving governance and curbing corruption, check out our new landing page for these issues, which spotlights our latest blogs, research, factsheets, videos and more.

MULTILATERAL SOLUTIONS TO GLOBAL CHALLENGES

In a recent speech at the U.S. Chamber of Commerce, IMF Deputy Managing Director Antoinette M. Sayeh spoke on three global economic priorities where we need multilateral solutions:

(1) Vaccines. Right now, vaccine policy is the most important economic policy. Investing in ensuring everyone rapidly has access to vaccines may well be the highest-return public project if you consider that faster progress in ending this crisis would add almost $9 trillion to global GDP by 2025, enabling over $1 trillion in additional tax revenue.

(2) International tax. It is broadly in the interest of countries—and of the private sector—to limit tax competition and the proliferation of chaotic, unilateral tax measures. We must come together to create an international tax system that is designed for the 21st century: one that is simplified, harmonized, predictable, and fair, thus instilling broad public trust. Multilateral efforts are already underway with the Inclusive Framework initiated by the OECD, which now includes 139 countries. The IMF supports the Inclusive Framework – and we are optimistic about a global agreement this year.

-

Speaking of taxation, the latest TADAT podcast discusses how the IMF and its development partner, the Asian Development Bank, cooperate to improve revenue mobilization and international tax practices in the Asia Pacific region.

(3) Climate. Yes, it is an economic priority. Climate change has an impact on macroeconomic and financial stability – and presents risks to the functioning of our economies. At the same time, the way in which we respond to this challenge also offers opportunities for growth and jobs. So, as the world starts to recover, we must accelerate the shift to a green economy. To do that, we need a robust price on carbon, which can send a critical market signal – and advance climate friendly investments. IMF analysis shows that steadily rising carbon prices and a green investment push could boost global GDP by about 0.7 percent per year in the next 15 years and create millions of new jobs.

Carbon pricing is already gaining momentum – many businesses now use a shadow carbon price in their models. But the average global price of $2 a ton needs to rise substantially by 2030 to be in line with the Paris Agreement. This is why the IMF has called for an international carbon price floor among large emitters, such as the G20. Focus on a minimum carbon price among a small group of large emitters could facilitate an agreement covering up to 80 percent of global emissions.

Focusing on a greener recovery clearly opens up prospects. But the harsh reality is that poorer nations risk missing out on this historic transformation. IMF research shows that low-income countries need $450 billion over five years to fight the pandemic, preserve buffers, and return to the path of catching up to higher income levels. They can cover only a portion of this on their own.

Read the speech and watch the video here.

F&D: BACK TO BASICS IN THE SPOTLIGHT

Have you checked out our Back to Basics explainers in Finance & Development magazine? They're an easy-to-read way to grasp the fundamentals of economic issues in the headlines.

What is the informal economy? Having fewer workers outside the formal economy can support sustainable development.

How can interest rates be negative? Countries are starting to experiment with negative interest rates.

What is stress testing? Checking the health of banks is crucial to financial stability.

What is carbon taxation? Carbon taxes have a central role in reducing greenhouse gases.

IMF AROUND THE WORLD

The IMF Executive Board this week concluded a review of Chile's performance under the Flexible Credit Line (FCL) arrangement.

IMF staff this week announced a staff-level agreement on the first review of Kenya's Extended Fund Facility and Extended Credit Facility. Staff also announced the conclusion of Article IV economic assessment missions for Ghana, Panama, Estonia, Timor-Leste, Slovakia, and Germany. Staff also concluded a virtual visit to North Macedonia.

RESPONDING TO THE CRISIS: To date, 86 countries have received more than $110 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note.

And if you're on LinkedIn, subscribe to this newsletter in a more 📈 visual format.

Sincerely,

|