|

Dear Colleague,

In today's edition we focus on COVID-19 and the global economy, USD and foreign exchange reserves, reforming international corporate taxation, the uneven recovery from the pandemic, the concentration of power among Big Tech, the impact of the pandemic on women, a digital Africa and more. On that note, let's dive right in.

AN OPPORTUNITY FOR CHANGE

IMF Managing Director Kristalina Georgieva discussed how the crisis presents an opportunity for how we deal with tax policy reform, climate change, inequality and other challenges. In a wide-ranging discussion (starting at 7h:25) with Alexander Stubb, director of the School of Transnational Governance at the European University Institute.

The MD also weighed in on how she views this week's news that the US would support negotiations to waive patent protections for the COVID-19 vaccine as a way to ramp up production of the shots.

"At the IMF we have been very clear that the economic argument for removing obstacles to accelerate production and to speed up vaccination is very strong," she said.

Two conditions: But the MD added that a waiver of intellectual property rights would only work if it was accompanied by a transparent process of allocating production and distribution of vaccines and measures to combat counterfeiting of vaccines.

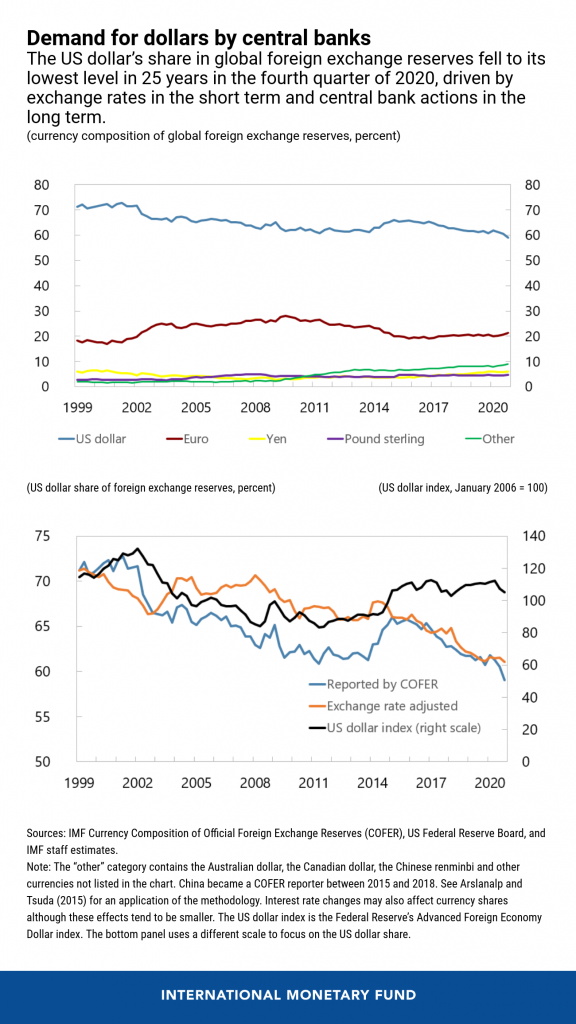

US DOLLAR SHARE OF GLOBAL FOREIGN EXCHANGE RESERVES DROPS TO 25-YEAR LOW

The share of US dollar reserves held by central banks fell to 59 percent—its lowest level in 25 years—during the fourth quarter of 2020, according to the IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) survey. Some analysts say this partly reflects the declining role of the US dollar in the global economy, in the face of competition from other currencies used by central banks for international transactions. If the shifts in central bank reserves are large enough, they can affect currency and bond markets.

Our Chart of the Week shows that the share of US dollar assets in central bank reserves dropped by 12 percentage points—from 71 to 59 percent—since the euro was launched in 1999 (top panel), although with notable fluctuations in between (blue line). Meanwhile, the share of the euro has fluctuated around 20 percent, while the share of other currencies including the Australian dollar, Canadian dollar, and Chinese renminbi climbed to 9 percent in the fourth quarter (green line).

Turning to this past year, once we account for the impact of exchange rate movements (orange line), we see that the US dollar’s share in reserves held broadly steady. However, taking a longer view, the fact that the value of the US dollar has been broadly unchanged, while the US dollar’s share of global reserves has declined, indicates that central banks have indeed been shifting gradually away from the US dollar.

Some expect that the US dollar’s share of global reserves will continue to fall as emerging market and developing economy central banks seek further diversification of the currency composition of their reserves. A few countries, such as Russia, have already announced their intention to do so.

Despite major structural shifts in the international monetary system over the past six decades, the US dollar remains the dominant international reserve currency. As our Chart of the Week shows, any changes to the US dollar’s status are likely to emerge in the long run.

Read the full blog here by Serkan Arslanalp and Chima Simpson-Bell.

CORPORATE INCOME TAXES UNDER PRESSURE

In launching a new book about corporate tax reform by the IMF's Ruud A. de Mooij, Alexander D. Klemm, and Victoria J. Perry, managing director Kristalina Georgieva kicked off the event with brief remarks, an excerpt of which are below:

Looking back, the greatest historical driver of tax policy innovation has been war. The cost of World War I and post-war reconstruction helped create modern corporate taxation. Now, we face the two disastrous and very expensive crises of COVID and climate change.

These urgent needs, combined with a renewed spirit of multilateralism, give us a unique opportunity to rethink and fix the international tax system – to create a system that is truly fit for the 21st-century. Here the IMF fully supports the OECD’s Inclusive Framework on Base Erosion and Profit Shifting. It involves 139 economies, offering a chance to head off conflicting actions among these countries. And Janet Yellen energized the international tax reform conversation last month by announcing a push with G20 nations for a global minimum corporate tax rate.

This type of multilateral approach is the only way to ensure that highly profitable multinational firms both pay sufficient tax and pay it to countries where they have significant engagement, including in low-income developing countries. We are particularly optimistic for a global agreement on corporate income taxation in 2021. And it is urgently needed to avoid, down the road, the risk of spiraling into a chaotic tax or trade war where everyone loses.

Learn more about the book here (available for free), and watch the launch panel discussion here.

DIVERGENT RECOVERIES FROM THE PANDEMIC

IMF Chief Economist Gita Gopinath joined Bruegel Director Guntram Wolff for a live podcast event discussing the uneven recovery from the pandemic. She warned of uncertainty ahead, especially given the crisis India is now facing and the risk for other parts of the world where health systems and vaccine rates are low.

US inflation: The US economy appears to be entering into a more sustained recovery and people are benefitting from more government stimulus. Gopinath acknowledged a transitory uptick in inflation but downplayed the chance that this will become a persistent overshooting of the US Federal Reserve's 2 percent average inflation target. A rise in inflation could push the Fed to raise interest rates, which could have global implications.

"The $1.9 trillion package while large is still temporary and it's transitory. The supply side bottlenecks that we are seeing that also puts pressure on prices is also transitory in nature and in the second half of this year it should smooth out. The concern would be if there were new spending packages that were announced that were unfunded that gave you the expectation that this was a deficit financed increase in spending for multiple years," she said.

"When it comes to these newer packages, at least everything that's been announced so far signals that it will be financed through increasing revenues," she added.

RANA FOROOHAR ON THE ECONOMIC & SOCIAL FORCE OF BIG TECH

"Over the last decade or so, there has been a huge wealth transfer from Wall Street to Silicon Valley, so that you now have a situation where about 80% of corporate wealth is living in 10% of companies that are the richest in data, software, and intellectual property."

🎙️ In a new podcast, Rana Foroohar says the concentration of wealth and power among Big Tech firms has grown exponentially over the course of the pandemic. Foroohar is Global Business Columnist and Associate Editor at the Financial Times. She was invited to speak at the Institute for Capacity Development about her book Don't be evil, which examines the implications for society of the growing influence of Silicon Valley tech giants in all aspects of the economy.

Listen here or skim the transcript. For more on these themes, check out the Spring 2021 issue of F&D magazine on the digital future.

COVID-19: THE MOMS’ EMERGENCY

While the pandemic’s effect on workers has varied worldwide, the new reality has left many mothers scrambling. With schools and daycares closed, many were forced to leave their jobs or cut the hours they worked. New IMF estimates confirm the outsized impact on working mothers, and on the economy as a whole. In short, within the world of work, women with young children have been among the biggest casualties of the economic lockdowns.

Given the disproportionate impact of lockdowns and containment measures on mothers—especially those with young children, targeted measures are needed to ease their return to work.

-

Financial support: Measures such as tax credits for low-income households with children, extension of unemployment benefits, and childcare assistance.

-

Childcare and schools: Governments should also incorporate considerations for school reopening when formulating vaccination priority lists. The availability of childcare is crucial to enable mothers to participate in the labor market.

-

Reallocation policies: Mothers, and women in general, are more likely to occupy jobs that require face-to-face interaction. COVID-19 has disproportionately destroyed such jobs, and some of them won’t return. Therefore, governments should support workers in finding other jobs through hiring subsidies and training programs, including tech training.

-

Access to finance: Increasing access to financial services could greatly help women to start/maintain their businesses. Equal access to digital infrastructure, such as access to mobile and internet coverage—as well as greater financial and digital literacy—can be a game changer for women.

Read the full blog here by Kristalina Georgieva, Stefania Fabrizio, Diego B. P. Gomes, and Marina M. Tavares.

F&D: A DIGITAL AFRICA

In our latest issue of F&D, special adviser on Africa to United Nations Secretary-General António Guterres and former finance minister of Cabo Verde Cristina Duarte writes that in rebuilding after COVID-19, policymakers in Africa must invest in innovative technology to leapfrog obstacles to inclusive development.

Africa has enjoyed strong economic growth for most of the 21st century, mainly because of robust global demand for primary commodities. But the “Africa Rising” narrative that accompanied this growth is mostly a story of rising GDP, which is overly one-dimensional. In fact, Africa’s economic growth has failed to generate many good jobs—postponing, once again, the benefits of the demographic dividend of a large working-age population. Because there are fewer old and young people that require support than people of working age, the dividend is supposed to free up resources that can be devoted to inclusive development.

Instead, African policymaking continued its now nearly half-century belief that achieving “development” is limited to managing poverty—in other words, equating the business of development to poverty reduction. The shift from the industrialization agenda of the early post-independence period to one of poverty reduction is a major reason for the continent’s economic malaise. As the African Innovation Summit (2018) put it, the development agenda shifted from socioeconomic transformation to the lowest common denominator, managing poverty.

To generate economic growth that leads to sustainable development, Africa must shift its focus to retaining and creating wealth, better managing its resources, fostering inclusiveness, moving up on global value chains, diversifying its economies, optimizing the energy mix, and placing human capital at the center of policymaking.

📣 Did you know that the IMF’s African Department was created 60 years ago, on May 1, 1961? To commemorate this anniversary, President Alassane Ouattara of Côte d’Ivoire will join Managing Director Kristalina Georgieva for a conversation on Monday, May 10, 2021 at 9:00 AM ET. President Ouattara will share his remarks on how the IMF and Africa have changed, and sub-Saharan Africa’s post-pandemic recovery.

IMF AROUND THE WORLD

The IMF Executive Board this past week concluded an Article IV economic assessment consultation of New Zealand and a review of Colombia's performance under the Flexible Credit Line arrangement.

IMF Staff this week concluded a review mission for Rwanda. Staff also issued statements concluding Article IV missions for the Dominican Republic, Guatemala, Hungary, Saudi Arabia, and Guinea.

IMF Staff also reached agreements with Senegal on the third review under the Policy Coordination Instrument and new 18-month, roughly $650 million financing arrangement. Staff also reached agreement with Honduras on the fourth review of the Stand-By Arrangement and Stand-by Credit Facility, proposing an increase of Fund support to $769 million.

RESPONDING TO THE CRISIS: To date, 86 countries have received more than $110 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note.

And if you're on LinkedIn, subscribe to this newsletter in a more 📈 visual format.

Sincerely,

|