|

Dear Colleague,

We just published a new blog—please find the full text below. Translations coming soon.

AGING ECONOMIES MAY BENEFIT LESS FROM FISCAL STIMULUS

By Jiro Honda and Hiroaki Miyamoto

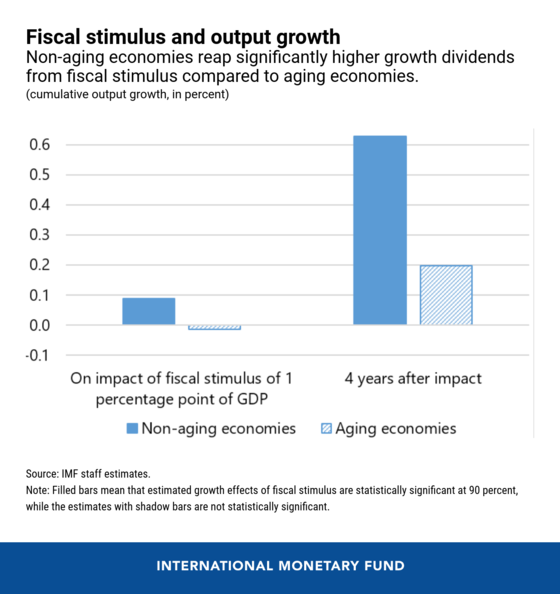

In the midst of the current COVID-19 pandemic, policymakers around the world are undertaking fiscal stimulus—a combination of spending increases and tax reductions—to support their economies. Even before the present crisis, the importance of fiscal policy has been increasing, with monetary policy constrained by near-zero interest rates. Yet our new staff research finds that age also matters when considering fiscal stimulus. Specifically, we find that fiscal policy isn’t as effective in boosting growth in economies with older populations, compared to economies with younger populations.

As our chart shows, fiscal stimulus in economies with a younger population has a significantly positive effect on growth, but the effect is much weaker in aging economies. We looked at 17 OECD countries from 1985 to 2017, and split the sample into two groups by looking at the ratio of old people among population. In the aging economies, the average old-age dependency ratio (defined as the ratio of people 65 and older to those between 15 and 64 years old) is 26.5 percent whereas in non-aging economies it is 18.9 percent.

|

On a more granular level, an aging economy behaves this way because its labor force isn’t growing, while its public debt tends to be high, and, therefore, fiscal stimulus has weaker effects on private consumption and investment. This is because the working age population is more likely than retirees to benefit from fiscal stimulus through effects such as increased corporate hiring. Furthermore, many pensioners are on fixed incomes whose consumption remains steady or even declines over time. In addition, population aging could reduce potential growth (by lowering labor input and productivity), with which fiscal stimulus may induce less private investment. The “older” the economy and the higher its debt, the less impact fiscal stimulus has on growth.

These findings complement existing observations that countries with aging populations have relatively low growth and higher public debt. Yet our findings are especially important because old-age dependency ratios have been rising for several decades and are projected to increase further. Within the next 30 years, more than 20 countries across the world would exceed the old-age dependency ratio of 50 percent—an unprecedented level in global history—with some even reaching 70 percent.

In other words, population aging is posing significant challenges to policymakers. How can we support aggregate demand with the weaker growth impact of fiscal stimulus in aging economies? The paper draws the following implications for policymakers to consider:

- A larger fiscal stimulus may be required to support aggregate demand during recessions.

- Given the lower output effects of fiscal stimulus, other economic policies (including structural reforms) would need to play a more important role in supporting domestic demand. Policy measures to enhance labor supply (for example, through stronger female labor force participation or labor market needs-based immigration) would help increase the output effects in aging societies.

Secure sufficiently large fiscal space (room to raise spending or lower taxes more than previously planned, without endangering debt sustainability or access to capital markets) during booms, in order to prepare for a larger fiscal stimulus during recessions, without creating concerns for fiscal sustainability.

*****

Thank you again for your interest in IMF Blog.

Take good care,

P.S. Are you on LinkedIn? Subscribe to our new Weekend Read visual newsletter.

_____

Surprise a colleague: forward this email

First-time reader? Sign up here

Update your profile for tailored content

View all IMF newsletters

Unsubscribe from IMF Blog here

|