|

Dear Colleague,

We just published a new blog—please find the full text below. Translations coming soon.

YOU’VE GOT MONEY: MOBILE PAYMENTS HELP PEOPLE DURING THE PANDEMIC

By Sonja Davidovic, Delphine Prady and Herve Tourpe

The practical challenge of quickly getting financial support in the hands of people who lost jobs amid the COVID-19 economic crisis has baffled advanced and developing economies alike. Economic lockdowns, physical distancing measures, patchy social protection systems and, especially for low-income countries, the high level of informality, complicate the task. Many governments are leveraging mobile technology to help their citizens.

Togo, a small West African nation of 8 million, was able to quickly distribute emergency financial support to half a million people in less than two weeks using mobile phones. The technology helped deliver benefits to women in particular, and it supported a transparent rollout of the program. Informal workers in Morocco are also receiving government help through their phones quickly and efficiently.

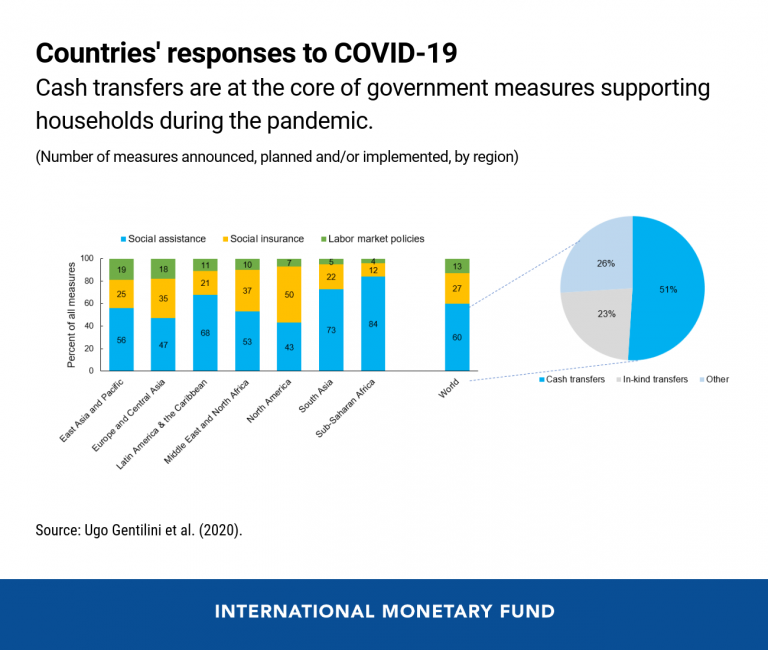

Social assistance and cash transfers

Many emerging and low-income countries are scaling up direct support to households and individuals because they cannot directly protect jobs. Missing data on employment status and blurry lines between corporations and individuals in the informal sector hinder the effectiveness of labor market policies. Therefore, governments bet on cash transfers when trying to boost their social protection systems, while trying to expand their coverage.

In sub-Saharan Africa, over 80 percent of measures announced since the beginning of the pandemic are in the form of transfers, and only 4 percent were labor market policies. Globally, 30 percent of all the initiatives taken by countries are cash transfers.

Typically, the delivery of income support targeted to the most vulnerable households relies on a robust national identification (PDF) system linked to socioeconomic information, and requires a variety of approaches in distributing cash to those most in need. Missing any one of these components in their immediate response to the crisis can generate difficult challenges (PDF): for instance, if a government cannot target beneficiaries due to the lack of socioeconomic information, it may have to choose between either spending more to cast a wider safety net or keeping the budget in check and excluding households in need of support.

Effective cash transfer mechanisms

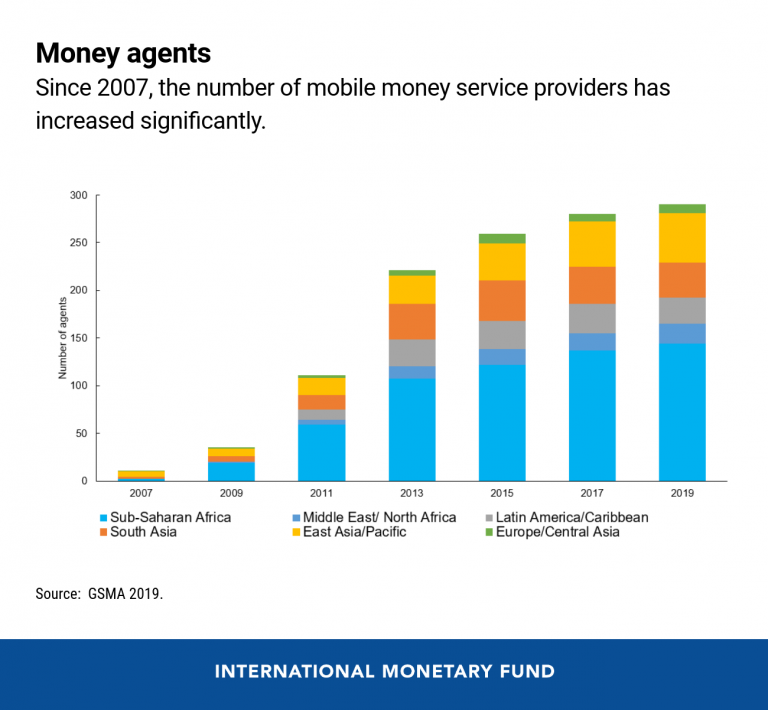

Mobile money is as an effective and physical-distancing-friendly option to deliver cash transfers in large scale, given that ownership and use of mobile phones in emerging and developing economies is very high, and globally, there are 228 mobile money agents (the small retailers where customers can deposit or withdraw cash in and out of mobile accounts, buy phone airtime cards, etc.) per 100,000 adults compared to only 11 banks and 33 ATMs. Mobile money can therefore help rural and remote populations gain access to government transfer programs without traveling long distances or waiting in lines, or even having a bank account—a critical advantage in a world where 1.7 billion still don’t have access to formal financial institutions.

The pandemic has led many countries to strengthen their mobile money ecosystems and address specific constraints. Governments with more developed operations were able to react faster.

Ecuador doubled the number of licensed cash agents in two weeks. Malaysia expanded free mobile internet access. Nigeria partnered with mobile network operators to identify vulnerable informal workers in urban areas through airtime purchase patterns. Saudi Arabia reduced mobile usage fees to encourage mobile payments. Some years ago, Peru fostered the creation of a platform that allows transfers across three leading mobile operators and 32 banks.

Mobile money does have risks and limitations. People in rural and remote areas may lack mobile coverage, easy access to money agents, or simply electricity. Exchanging mobile money for cash can still be expensive. And digital and financial illiteracy are known to hinder adoption of digital mobile services.

In many countries, the pandemic has forced policymakers to react quickly to reduce regulatory weaknesses around mobile money issued by telecom or fintech firms, whose customers are often not protected by regulation in the same way as banks’ clients. It’s important to ensure that the risks of accelerating mobile money, including cyber-risks and digital fraud, don’t outweigh the benefits.

A mobile-money framework

Beyond the crisis horizon, many countries have sought to boost mobile payment platforms to reduce corruption, improve efficiency and budget transparency, and broaden financial inclusion, especially for the informal sector and women.

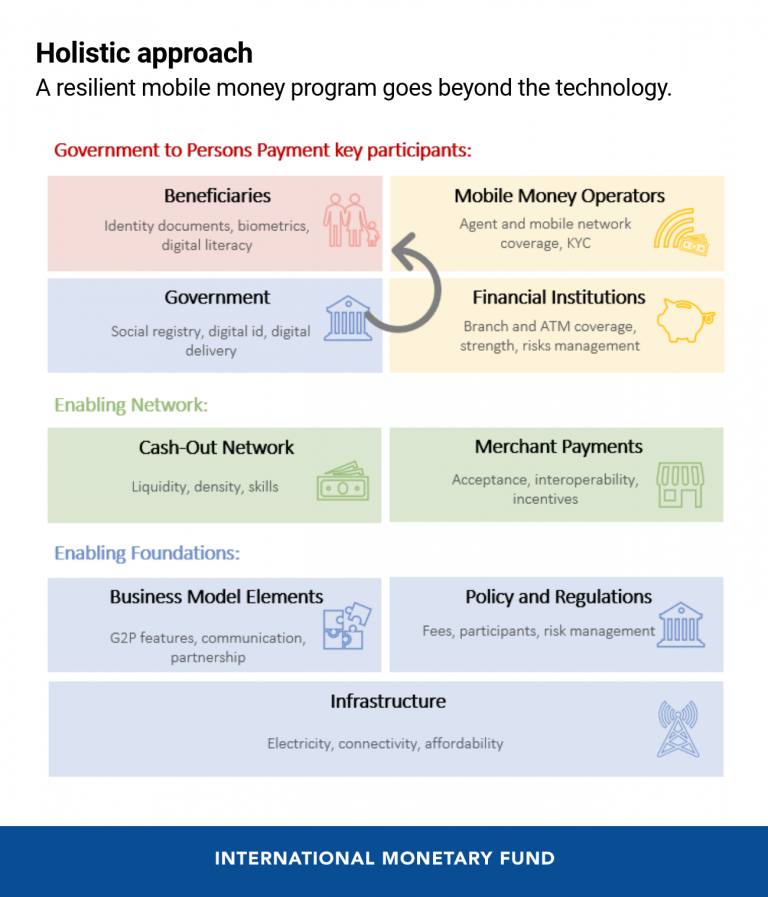

While scaling mobile cash transfers quickly to help alleviate the impact of the pandemic, governments should take a broad approach that goes beyond the technology and consider the whole ecosystem behind a robust and resilient mobile program.

A holistic approach should be considered by policymakers and the industry to integrate all the “building blocks” of a sustainable mobile-money platform, including stakeholders and design and policy elements that help maximize benefits against risks.

As countries move from crisis mode to a new normal, it’s a good time to also take note of the impediments they encountered in expanding support to people suffering the economic consequences of lockdowns. At the same time, they can build on solutions that worked best to make up for income losses, focusing on sustainable solutions instead of workarounds deployed at the height of an emergency. This should be part of broader government strategies to strengthen social protection systems in the medium term through technology.

*****

Are you on LinkedIn? Subscribe to the IMF Weekend Read LinkedIn newsletter to get notified of the latest analysis on global economics, finance, development and policy issues shaping the world. And feel free to leave comments each week to connect with colleagues and continue the conversation.

Take good care,

P.S. Have you seen our latest issue of F&D magazine? It focuses on economic policymaking and politics in light of the pandemic. Every week, our F&D newsletter digs deeper into each article so update your subscriptions (enter your email) and select IMF Finance & Development to learn more.

_____

Surprise a colleague: forward this email

First-time reader? Sign up here

Update your profile for tailored content

View all IMF newsletters

Unsubscribe from IMF Blog here

|