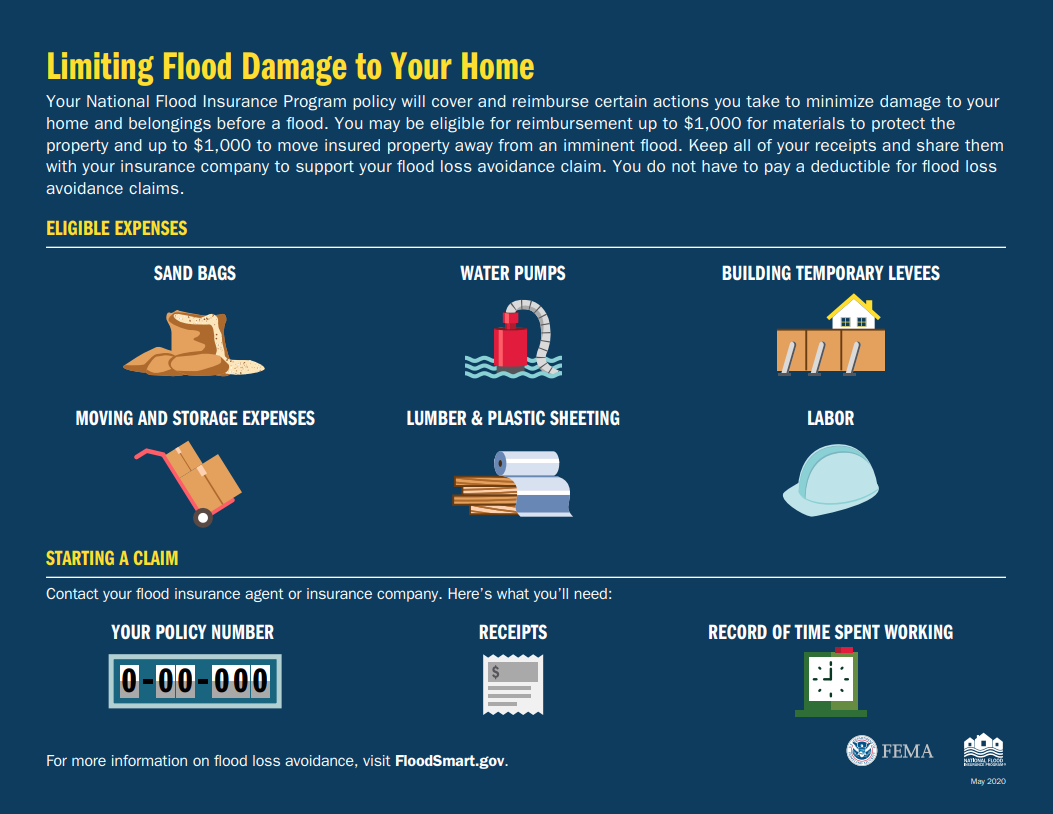

For NFIP policyholders: Flood loss avoidance coverage may reimburse pre-flood actions.

Learn what's covered, and make sure to save your receipts. For more information, view the fact sheet Understanding Flood Loss Avoidance or reference the NFIP Claims Manual (pages 47-48, 65, 111-112, 171-172).

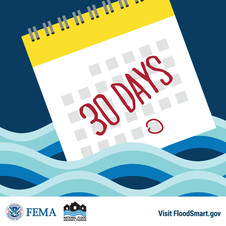

For NFIP policyholders with recently expired policies: You may be able to renew and be covered for a loss.

NFIP policies have a 30-day grace period after they expire. Claims for losses that occur in this grace period will be honored, provided that the full renewal premium is paid and received by your insurer before the end of the 30-day grace period.

Call your insurance agent or the NFIP Call Center at (877) 336-2627 to see if you are still in a renewal grace period.

|

For those looking to buy flood insurance: There is a typical 30-day waiting period.

National Flood Insurance Program (NFIP) policies typically take 30 days to go into effect from the date of purchase. But, there are some exceptions:

No waiting period:

- If you purchase flood insurance while making, increasing, extending, or renewing your mortgage loan.

- If you change your flood insurance coverage on your insurance policy renewal bill.

- In the event of flooding after a wildfire, if a property is impacted by flooding on burned federal land and the policy is purchased within 60 days of the wildfire-containment date. Waiving of the waiting period is determined at the time of claim.

1-day waiting period:

- If a home or business is newly designated to be in the high-risk flood area and you purchase flood insurance within the 13-month period following a map update.

If possible, don't delay in getting flood insurance coverage. Call your insurance agent today. There is a flood-in-progress exclusion that primarily affects applicants or policyholders who wait to purchase flood insurance or increase their coverage until flooding is imminent.

|

For anyone at risk of flooding: Follow these tips.

- If flooding is imminent, turn on sump pumps, close backflow valves, shut off electricity at the breaker, and use sandbags and other flood barriers.

- Move paperwork and valuables to upper floors or off the ground if possible.

- Elevate major appliances onto concrete blocks.

- Click here to read more about ways to protect your home.

|