|

APRIL 2025

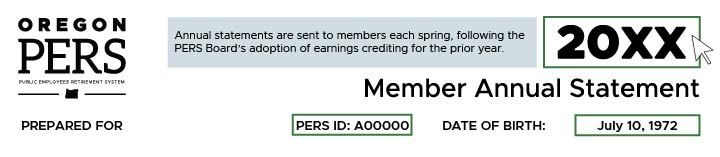

2024 member annual statements on their way in May

Member annual statements for 2024, reflecting data submitted by your employer as of December 31, 2024, will be mailed by the end of May.

When you receive your statement, check that all of your personal information is correct. If not, contact your PERS-participating employer. If you are not currently employed by a PERS-participating employer, you can submit an Information Change Request form or request changes through Online Member Services (OMS).

As an Oregon Public Service Retirement Plan (OPSRP) member, you have two parts to your PERS retirement: a pension and an Individual Account Program (IAP) account-based benefit. Both parts will be included on your statement.

Additionally, if you have an Employee Pension Stability Account (EPSA), that information also will be included on your statement. (Read more about EPSA in "Things to know about Member Redirect and your IAP" in this newsletter.)

Why send annual statements in May?

PERS cannot finalize 2024 statements until after the PERS Board adopts 2024 final earnings crediting, which occurred on March 31.

What resources can help me understand my statement?

Annual statement FAQs and resources are available on the PERS website, and the FAQ webpage is updated each year in spring.

Three key areas to review on your statement are:

-

Your birthdate and other personal information, such as your address, hire date, and membership date. Your birth date is used to establish which age-based target-date fund (TDF) your IAP is invested in.

-

Your retirement credit. Your years of service — also known as your retirement credit — are used to calculate your monthly pension benefit. Create a benefit estimate in Online Member Services (OMS) or use the formula listed on your statement to get an idea of what your monthly pension could be.

-

Your IAP information. This area shows you the investment returns for your target-date fund. Each fund has its own mix of investments, set by the Oregon Investment Council. Your investment returns may differ from other members who are in different TDFs.

|

|

Free federal and state tax filing options available

Do you still need to file your 2024 state and federal income taxes?

If you do, check out whether you are eligible to file electronically for free through IRS Direct File and Direct File Oregon.* If you live outside of Oregon, check with your state's taxing agency to see if they offer a direct-file option.

The Internal Revenue Service (IRS) offers a tool you can use to check your eligibility.

Read more about the IRS' and Oregon's direct-filing options on the Oregon Department of Revenue’s (Revenue) website. For more information, contact Revenue or the IRS.

*The Oregon Department of Revenue continues to assess federal changes and any impacts on Oregon. As of Perspectives' deadline, Direct File was open, and Oregonians were successfully using IRS Direct File and Direct File Oregon to file their 2024 taxes. Revenue advises Oregonians to use the IRS eligibility tool linked to above to check whether they can directly file.

|

|

|

Annual reports detail PERS' finances and more

Do you like details? Have you ever wanted to dive into the nitty-gritty of your pension system?

Well, PERS has some reports for you.

Each year, PERS, the agency, publishes several documents about the finances and operations of the PERS system. They are:

-

PERS by The Numbers — This annual report highlights financial, administrative, and demographic information from the past year. It’s published each December.

-

Annual Comprehensive Financial Report — As the name indicates, this report provides a complete look at all financial, actuarial, and statistical aspects of the PERS system for the fiscal year ending each June. It’s published each December.

-

Popular Annual Financial Report — This report is a summary of the Annual Comprehensive Financial Report written for a more general audience. It was launched in 2024 and will be published each December.

-

Economic Impact Study — This short report tells the tale of how benefits paid to PERS retirees affect Oregon’s economy. It’s published each summer.

Besides these reports, PERS publishes one more document you can explore to learn how the pension system started and evolved into what it is today: PERS History. This document is now in its third edition, having been last updated in 2021.

|

|

|

We want to hear your thoughts about PERS

The PERS annual Member Satisfaction Survey is coming next month. Share your feedback and help PERS, the agency, improve our member services.

Starting May 1, you can complete the survey online. PERS will send a reminder about the survey once it's available.

You will have until May 31 to complete this online-only survey.

|

|

|

Retiring soon? Sign up for our retiree newsletter

If you plan to retire soon (or have just retired), take a moment to update your topic subscriptions in our news alert system, GovDelivery.

You can subscribe to our retiree newsletter and other retiree news topics to stay connected with us as you transition into retirement.

PERS can't automatically update your existing subscriptions for you, so be sure to review your subscriber preferences and make changes accordingly.

|

|

Member Choice: If you opted to change your TDF ...

Any changes you made to your Individual Account Program (IAP) target-date fund (TDF) by September 2024, took effect on January 1, 2025, and you cannot make any new changes in Online Member Services until the next Member Choice window in September 2025.

Changes that took effect in January will not be reflected on the member annual statement you receive this spring because the cut-off date for account information that goes into your statement was December 31, 2024. You will see January 2025 changes on your spring 2026 statement.

Find full information about Member Choice on the IAP target-date funds webpage.

|

|

|

If you earn more than the annually adjusted monthly salary threshold*, a portion of your 6% IAP contributions is now redirected into your Employee Pension Stability Account (EPSA). EPSA contributions and earnings from 2024 will be shown on your 2024 member annual statement, which you will receive in spring 2025. The redirect to EPSA remains in effect when the PERS system is less than 90% funded**.

To offset the redirect, you can opt to make a post-tax 0.75% voluntary contribution to your IAP or consider increasing your retirement savings elsewhere, such as with the Oregon Savings Growth Plan (OSGP). Remember that you can begin or end voluntary IAP contributions by logging into your Online Member Services (OMS) account.

Find full information about Member Redirect on the IAP redirect webpage.

*The link will take you to an EPSA overview webpage. Once there, click on the “Does EPSA apply to every PERS member?” accordion to access threshold information.

**The latest actuarial valuation shows that PERS’ funded status including side accounts was 77% as of December 31, 2023.

|

|

|

Salary limit increased for benefit calculations

In January 2025, the limit on subject salaries used in benefit calculations increased to $238,567* per year.

PERS uses subject salaries to determine member IAP contributions, employer contributions to fund the pension program, and the final average salary for calculating retirement benefits under formula methods.

If you plan to retire in the first few months of 2025, be aware that salary limitations also apply to working partial years. Read more about Senate Bill 1049 salary limits and partial year salary limits online.

*Indexed annually to the Consumer Price Index

|

|

|

If you are no longer working for a PERS-participating employer and considering whether to withdraw your Individual Account Program (IAP) balance, read our webpage about OPSRP withdrawals first.

Since July 1, 2020, withdrawing an IAP balance will result in the loss of OPSRP membership. That means you forfeit your rights to all future PERS benefits — including your pension.

You will not be paid any pension benefits in retirement nor the actuarial equivalent of your pension when you withdraw. You will only receive the balance of your IAP (and Employee Pension Stability Account, if applicable).

You also will lose all of your accrued OPSRP retirement credit, and you will not have the option to restore it at a later date.

|

|

|

Your retirement future is up to you. How you plan and save for your retirement can determine your retirement security.

To check whether you’ll have the money you need for a secure retirement, begin by gathering benefit estimates for your retirement accounts and Social Security. Two available estimation tools are:

Also check the value of your Individual Account Program (IAP) on your member annual statement or by logging into your IAP account online.

Add up your estimates, consider your IAP, and compare your total estimated income to what financial experts say you’ll need when you retire: 80% of your working income.

If your total estimate falls short, you may consider saving additional money in other retirement accounts.

One option for saving more is the Oregon Savings Growth Plan (OSGP). OSGP offers both pre- and post-tax retirement savings options and various free educational workshops. Check with your employer to see if OSGP or other voluntary retirement savings options are available to you.

|

|

|

Preparing for retirement requires many steps — from estimating whether you’re saving enough to designating beneficiaries as applicable to your membership type.

Something else to plan for is who will act on your behalf in the event of severe illness or death. Check out these resources:

-

Authorization to Release Account Information* — This form will allow you to name other parties who can receive information about your PERS benefits, including account balances and benefit estimates.

-

Special Power of Attorney for PERS* — This form will allow you to designate others who can make decisions about your PERS benefits on your behalf.

Also be aware that when you die, a family member, beneficiary, or caregiver must notify PERS. More information about member deaths and death benefits is available on the PERS website.

*Note that the account information release and special power of attorney (POA) forms are only valid while the member is alive. You can cancel the release and special POA at any time.

|

|

|

As you ponder your future retirement, don’t forget about health care.

Many public employees have the majority of their health insurance costs covered by their employers while they are still working. In some cases, employers may cover up to 99% of medical, dental, vision, and basic life insurance premiums. When you stop working, the cost of your insurance coverage will rest solely with you.

Depending on your age and other factors at retirement, you may or may not yet be eligible for Medicare coverage. Even when you are eligible, Medicare does not cover all health care costs, and you may wish to have supplemental coverage to bridge the gap.

Once you become a PERS retiree, several health insurance options will become available to you through the PERS Health Insurance Program (PHIP). PHIP offers Medicare and non-Medicare plans, as well as dental options.

Visit the PHIP website or call 800-768-7377 for more information about the program.

Additional information about health care coverage and costs

- Some industry estimates say the average health care costs in retirement amount to hundreds of thousands of dollars.

- Estimator tools can help you explore possible health care costs. Fidelity, a financial services corporation, offers one such tool. This tool is for general information only and not a guarantee of future costs.

- If you have questions about Medicare, check out the Oregon Senior Health Insurance Benefits Assistance (SHIBA) program. SHIBA offers certified, local counselors who can help.

|

|

|

Are you planning to retire in the near future? Don’t wait until the last minute to prepare.

Check out these helpful resources from PERS to get ready:

Also, keep the following important points in mind:

- Retirement applications may be submitted to PERS within 90 days of your retirement day.

- It can take up to 92 days from your retirement date (not the date of your application submission) for your first pension benefit to be paid.

- Once PERS receives your application, we will review your account information and reconcile data with your employer(s) as needed. Data discrepancies can sometimes cause your finalized benefit amount to differ from benefit estimates you received earlier. Remember that benefit estimates are just that — estimates.

- Filling out your application correctly, checking your personal information in OMS or on your member annual statement, requesting benefit estimates, and responding to requests from PERS for additional information can help you avoid delays in the processing of your application. If you are working for a PERS-participating employer and find errors in your personal/account information, contact your employer for corrections. If you are not working for a PERS-participating employer, read the inactive member section on our Change your address webpage for instructions.

-

Individual Account Program (IAP) retirement benefits can typically take from 90 to 120 days to process and complete payments or rollovers. Processing is done both by PERS and Voya, which administers IAPs for PERS.

If you have questions, contact Member Services for assistance.

|

|

|

By Dr. Elizabeth Steiner

Oregon State Treasurer

I’m honored to serve as Oregon’s new state treasurer. As a physician, mom, and legislator, I bring a wide range of experiences to my job. Yet in all these roles, I’ve seen how financial stability and well-being are important to a secure and fulfilling life.

A financially secure Oregon is a healthy Oregon.

Protecting your retirement — and the retirements of all Oregon’s public employees — is the most important part of Oregon State Treasury’s mission.

I’ve traveled to communities in every corner of the state. I know the many ways in which public employees protect public safety; keep us healthy; educate our children; care for the elderly, disabled, and vulnerable; build and maintain our roads; conserve our natural resources; and otherwise support their communities.

I’ve seen the dedication you’ve displayed in your public service career — whether it’s responding to an emergency call in the dead of night or connecting a family struggling to put food on the table to the nutrition benefits they need. I appreciate everything you do to keep Oregon safe, healthy, and thriving.

As treasurer, I’m focused on:

- Growing the Oregon Public Employees’ Retirement Fund (OPERF) and other investments while moving away from carbon-intensive investments that create long-term return risks.

- Strengthening the financial well-being of all Oregonians — especially families — by expanding the number of children with college savings accounts, ensuring that every eligible Oregonian is enrolled in OregonSaves and saving as much as possible, and exploring the creation of savings accounts for children.

- Expanding financial empowerment programs so every Oregonian has the knowledge to take charge of their financial future.

At this time of change and uncertainty, I will be vigilant in calling for national and state priorities that support the financial well-being of Oregonians — or challenging efforts that could undermine the financial stability of state residents, OPERF, or state services.

As treasurer, I will keep you informed about how we are managing OPERF and keeping your retirement security at the forefront of everything we do. I’m looking forward to continuing to visit communities across the state. I hope to meet many of you.

Thank you again for all you do for Oregon.

|

|

|

The Oregon Public Employees Retirement Fund (OPERF) earned 5.71% in investment returns for 2024.

However, annual earnings credited to member accounts will be different than this rate. They differ because of administrative expenses and various requirements set by state law, administrative rules, and PERS Board actions.

The board approved the 2024 annual earnings crediting to member accounts at its March 31, 2025, meeting. You can find the rates credited to various accounts on the 2024 earnings crediting webpage. The accounts include Tier One/Tier Two regular accounts, the Individual Account Program target-date funds, and Employee Pension Stability Account.

The 2024 earnings credited to your accounts will be reflected in your upcoming 2024 member annual statement. You should receive this statement by the end of May.

OPERF is managed by Oregon State Treasury under the direction of the Oregon Investment Council (OIC).

|

|

|

As a PERS member, you may wonder how your pension system keeps track of its financial health.

Each year, PERS calculates its “funded status,” which compares projections of how much money the PERS system will have versus how much it is expected to pay out in retirement benefits within a certain timeframe.

To calculate the funded status, PERS follows a process called an “actuarial valuation.”

The latest actuarial valuation* shows that PERS' funded status is 77% as of December 31, 2023. This valuation includes funding from employer sources known as "side accounts."

Every two years, the PERS Board examines how much money is coming into the system through employer sources. Based on the actuarial valuation and other data, the board decides whether to change employer contribution rates (C) to ensure that money coming into the system — along with projected earnings from investments (E) — will be enough to cover benefit payments (B).

On the earnings side, 73% of benefit payments since 1970 have been paid for by long-term investments in the Oregon Public Employees Retirement Fund (OPERF).

*The next actuarial valuation will be for the year ending December 31, 2024. It will be released in fall 2025.

|

|

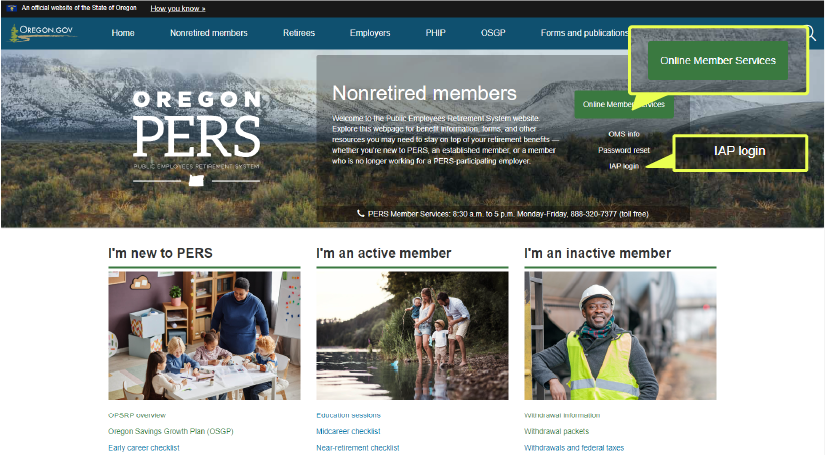

You can access logins for Online Member Services (OMS) and the Individual Account Program (IAP) from the webpage for nonretired members.

Need to check your retirement credit, register for an education session, or update your address or contact information? PERS has you covered with a number of self-service tools.

Online Member Services

Online Member Services (OMS) is where to go to:

- Review your employment history, including your salary and retirement credit.

- Generate online benefit estimates for your pension.

- Check your contact information, including your address, email, and phone number. You can update your email and phone information yourself in OMS. Your address is submitted by your employer, and you will need to contact your employer to update it.

-

Begin or end voluntary contributions to your IAP.

If you need to set up an OMS account, check out our What is OMS? webpage.

Individual Account Program (IAP)

Use the Individual Account Program (IAP) portal to check information about your IAP account, such as your IAP balance and ongoing contributions.

Note that employer reporting cycles and other factors can sometimes delay updates to your IAP information from being displayed in the IAP portal.

And if you’ve never logged into your IAP before, you’ll need to contact Member Services to request an initial login PIN. Further details can be found on PERS’ IAP account log-on information webpage.

Oregon Savings Growth Plan (OSGP)

Do you want to save more for retirement? Learn how you could supplement your retirement savings through the Oregon Savings Growth Plan (OSGP).

Find your forms

Want to designate your beneficiary, request a benefit estimate, or apply for retirement? There’s a form for that.

Find the form you need on PERS’ Most requested forms and OPSRP forms webpages.

When retirement nears

If you’re close to your desired retirement age, it’s time to review the steps you need to take to retire.

PERS recommends you start these preparations early to avoid delays in your retirement process. Preparations should include getting online or written benefit estimates of what your pension payments could be and participating in a PERS education session.

Post-retirement health plans

How will your health care needs be covered in retirement? Learn about Medicare and non-Medicare plans and options for supplemental medical and dental insurance through the PERS Health Insurance Program.

|

|

PERS will not call you and ask for money, donations, your account login, or your financial information.

However, PERS may call you in response to a request you made, a form you submitted, or another action you took.

Other examples of when PERS may call you include:

- You are a retiree living internationally or are age 80 or older. We do this to confirm that we are still correctly paying members their benefits and to check for unreported deaths.

- You must take a required minimum distribution (RMD), and we need you to submit RMD-related documents.

- We found that you should be receiving additional funds in your retirement benefits or as part of a previous withdrawal.

If you are unsure whether someone contacting you is from PERS, call Member Services directly at 1-888-320-7377 to check.

Read more on our Protect yourself from fraud webpage.

|

|

|

|

|

Stay informed with PERS email or text updates |

|

|

You can get alerts on topics that include:

- Member news

- PERS Health Insurance Program

- Legislation affecting members

- PERS Board meetings

- PERS administrative rulemaking

|

|

|

Mailing address:

PERS

PO Box 23700

Tigard, OR 97281-3700

Physical address:

11410 SW 68th Parkway Tigard, OR 97223

Phone: 888-320-7377

TTY: 503-603-7766

Phone lines open 8:30 a.m. to 5 p.m. Monday through Friday, except holidays.

|

|

We serve the people of Oregon by administering public employee benefit trusts to pay the right person the right benefit at the right time.

Chair: Jardon Jaramillo

Vice Chair: John Scanlan

Members: John Scanlan, Suzanne Linneen, Bob Hestand, and Kristen Connor

Director: Kevin Olineck

Deputy Director: Yvette Elledge-Rhodes

Chief Financial Officer: Richard Horsford

Chief Information Officer: Jordan Masanga

Chief Compliance, Audit, and Risk Officer: Jason Stanley Chief Operating Officer: Sam Paris

For more information contact:

PERS | PHIP | OSGP

|

|

|

Perspectives is published by the Oregon Public Employees Retirement System for the benefit of members and employers. It is emailed three times a year.

|

|

|

|

|