TOP STORY

Pursuant to GASB 75, a liability for "other post-employment

benefits" must be booked on the participating employer’s financial

statements for the year ended June 30, 2018.

OPEB includes the subsidy that retirees receive ($105) towards their

health insurance premium. That OPEB is

calculated through the pension systems.

The GASB 75 report available on OPERS’ website includes the information

necessary for the footnote in total for the state and a listing of agencies

with each agency’s percentage of the total.

Another aspect of OPEB pertains to the statutory requirement

that health insurance premiums through EGID be the same for active employees

and pre-Medicare retirees. If these

retirees were rated separately the premium would be higher. The difference is known as an implicit rate subsidy. EGID’s actuaries have calculated the OPEB

liability attributable to the implicit rate subsidy for the state’s CAFR. Agencies that prepare individual GAAP financial statements may use this

calculation to report the agency’s OPEB liability from the implicit rate

subsidy by applying the percentage attributable to the agency to the

information reported for the state as a whole.

Only agencies (or component units) who participate in the

group insurance offered by EGID and whose

payroll goes through the state system will be included in this

calculation. Other component units or

entities that produce GAAP financials are responsible for their own OPEB

calculation for the implicit rate subsidy.

To request a copy of the actuarial valuation for OPEB

related to the implicit rate subsidy and the allocation by agency, contact Matt

Clarkson at matt.clarkson@omes.ok.gov.

>> Back to Top

BUDGET

Some agencies have questioned why

certain benefit allowances have changed while others remain at the current

level. Premium rates for different tiers

(i.e. member, spouse, 1 child, and 2 or more children) do not increase at the

same rate every year, so some tiers will surpass the frozen 2012 levels in

different years. Since the average

spouse premium for Plan Year 2012 remains higher than the HealthChoice spouse

rate, the benefit allowances with the spouse have not changed.

The benefit allowance for budget

purposes was based upon an assumption of a 5 percent increase of the

current HealthChoice High Option premium.

The actual premium increase and

benefit allowance will not be known until Aug. 17, 2018. For appropriated agencies, the

legislature included the projected

increase for each agency into their appropriation based upon the current

elections of their employees.

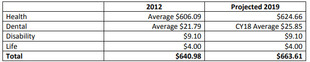

The benefit allowance consists of 4

components: The health premium (the

greater of the Plan Year 2012 average or the HealthChoice High Option), the

average dental premium, the disability premium and the basic life premium. According

to 74-1370 Section C, the benefit allowance shall not be LESS THAN the Plan

Year 2012 benefit allowance. This

article will give a few examples of the benefit allowance calculations and why

certain ones did not change.

For the member-only benefit

allowance, the amount projected for Calendar Year 2019 is in accordance with

74-1340 C.1. The current HealthChoice

High Option premium is $594.90. A projected

5 percent premium increase would be $624.66.

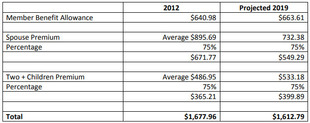

If a member has dependents, the benefit allowance is the members benefit allowance PLUS:

- for a spouse, 75 percent of the HealthChoice High Option plan, available for coverage of a spouse,

- for one child, 75 percent of the HealthChoice High Option plan, for coverage of one child,

- for two or more children, 75 percent of the HealthChoice High Option plan, for coverage of two or more children,

- for a spouse and one child, 75 percent of the HealthChoice High Option plan, for coverage of a spouse and one child, or

- for a spouse and two or more children, 75 percent of the HealthChoice High Option plan, for coverage of a spouse and two or more children.

For the member with one child benefit allowance, the amount projected below for Calendar Year 2019 is in accordance with 74-1340 C.2. The current HealthChoice High Option premium for One Child is $229.24. A projected 5 percent premium increase would be $314.20.

For the member with a spouse and two or more children benefit allowance, the amount projected below for Calendar Year 2019 is in accordance with 74-1340 C.2. The current HealthChoice High Option premium for a spouse is $697.50. A projected 5 percent premium increase would be $732.38. The current HealthChoice High Option premium for Two or More Children is $507.80. A projected 5 percent premium increase would be $533.18.

OMES has permanently discontinued use of Hyperion for the budgeting process. The security forms will be taken offline – 301EPLAN and 301UPK. As always, if you have questions about this or the new spreadsheet processes implemented in place of Hyperion, contact your OMES budget analyst.

>> Back to Top

ACCOUNTING

When an agency is authorized to have an ASA or 700 class

funding, the account must be strictly used for the authorized purpose. Authorization to have one of these accounts does

not exempt the agency from any other requirements for which the agency does not

have a specific exemption, for example, the Central Purchasing Act and

encumbrance requirements. The structure

and process for these accounts does not allow OMES to review or query to

determine whether purchasing procedures were properly followed. However, if issues are found upon an audit

the fact that the transaction was made through an ASA or 700 fund is not a

defense.

>> Back to Top

In October 2017 there was an article in the CAR

newsletter regarding notices that agencies had begun getting from the System of

Award Management. Because there is

still confusion about the Taxpayer Offset Program, we felt that

additional information needed to be distributed.

The Taxpayer Offset Program reviews payments to be made by

the federal government for either grant draws or vendor payments to see if the

payee has an outstanding debt to the federal government. Because the TOP uses the state’s federal

employment number (FEI), which for the State of Oklahoma covers all state

agencies, the offsets for debt may reduce payments to a different agency than

the one that owes the debt.

There are several notifications, which if addressed

properly, can relieve some of the issues related to TOP. These notices are detailed below:

-

Notice of debt – This is a notice that is sent

to the delinquent debtor by the federal agency that is owed. It will go to the last known address of the

agency prior to the debt being turned over to TOP. This is the first opportunity to pay or

negotiate with the federal agency that is notifying the debtor.

-

U.S. Department of the Treasury Notice of Debt –

This notice is sent to the address of the debtor when a collection item is

turned over to TOP. The agency has an

opportunity to make the payment to the Department of Treasury prior to offsets.

-

SAM Notification of Debt Subject to Offset –

This notice is sent to agencies with DUNS numbers registered with the state’s

FEI when debt has either been put into the TOP system, or has been cleared from

the TOP system. This debt may not be

related to the agency receiving the notice.

-

TOP Offset Notice – This communication from the

Department of the Treasury will indicate that an offset has happened and will

show the amount of the original payment to be made and the amount that was

offset. This notice has important information

that will help OMES determine whose payment was offset and which agency had the debt.

If an agency receives either a Notice of Debt or an Offset Notice from the Department of

Treasury, please forward

copies of the notices to CAR. OMES

receives reports from TOP which may match up to those notices and assist us in

resolving offset issues.

Some states participate in a reciprocal TOP program where

the state may offset its payments to vendors for federal debt. With those agreements, the Federal TOP will

also offset federal payments for debts owed to the reciprocating state.

PAYROLL

The schedule for running the FY Combo Code Conversion

process is:

- Evenings of June 29 and June

30, 2018 – Department of Human Services. This process must be run prior to

running the July 13, 2018, payroll.

-

Evening of June 29 and June 30,

2018 – All state agencies having bi-weekly payrolls. This process must be

run prior to running ‘B01’ or ‘C01’ payrolls which pay on July 20, 2018.

NOTE: This date includes agencies that run both monthly and

bi-weekly payrolls. All supplemental and off-cycle payrolls must be

completed and processed to GL by 3 p.m. on July 05, 2018. The EBS payroll team

will monitor agencies to help ensure payrolls are completed before the

conversion begins.

- Evenings of July 10 and 11,

2018 – All monthly anticipatory agencies. Do not begin processing M01

until July 16, 2018.

NOTE: As

soon as all on- and off-cycle payroll processes are completed for the June pay

period, please notify Enterprise Business Services by creating a service desk

case asking for the case to be assigned to the IS-HCM payroll group. This

will enable the EBS team to try and schedule the agency’s FY Combo Code

Conversion Process earlier. Questions may be directed to Carol

Barton at 405-522-4371 or carol.barton@omes.ok.gov.

>> Back to Top

Processing of the statutory pay raises included in HB 1024

will begin June 30 and should be completed by July 1. Agencies will need to

refrain from entering any information in the job record that is dated July 1,

2018, or forward until after the pay raises have been added. The processing of

the pay raises will begin with the Department of Human Services, then agencies

with bi-weekly payrolls and conclude with the monthly payroll agencies. For

questions related to the pay raise processing, please create a service desk

case asking for the case to be assigned to the IS-HCM payroll group.

>> Back to Top

The rate certified for the administrative

cost which will be calculated in payrolls submitted for the fiscal year

beginning July 1, 2018, has changed to $2.13 per month for any qualified

participant. The equivalent amount for a bi-weekly pay period is $0.98. This

change will be reflected in any payrolls submitted with a pay period code of

M01 or B01.

>> Back to Top

The rate certified for the

administrative cost which will be calculated in payrolls submitted for the

fiscal year beginning July 1, 2018, has changed to $1.13 per month for any

qualified participant. The equivalent amount for a bi-weekly pay period is $0.52.

This change will be reflected in any payrolls submitted with a pay period code

of M01 or B01.

>> Back to Top

The amount the State of

Oklahoma pays for employee retirement will remain at 16.5% for FY 2019.

>> Back to Top

The employer contribution

rate for the Uniform Retirement System for Justices and Judges will increase

effective July 1, 2018, from 20.5 percent to 22.0 percent beginning with any payrolls

submitted with a pay period code on M01 or B01.

>> Back to Top

The amount the State of

Oklahoma pays for employee retirement will remain at 11.0 percent for FY 2019.

>> Back to Top

The Federal matching

contribution rate for the Teachers Retirement System will decrease effective

July 1, 2018, from 7.80 percent to 7.70 percent beginning with any payrolls submitted with a

pay period code on M01 or B01. The federal matching contribution rate

must be paid when salaries are paid by federal funds or externally sponsored

agreements such as grants, contracts and cooperative agreements. Other TRS

contribution rates remain the same for FY 2019. For a complete list of

rates, please see the TRS website.

>> Back to Top

Please distribute the FY-2019

Pay Date schedules found at ScheduleOfFY19PayPeriods

to Payroll and Human Resource

directors. Questions on the codes may be directed to Lisa Raihl at

405-521-3258, lisa.raihl@omes.ok.gov

or Jean Hayes at 405-522-6300, jean.hayes@omes.ok.gov.

>> Back to Top

When processing non-paying taxable

fringe benefits for employees through payroll, only include

the amount when processing payable wages. Non-paying taxable fringe benefits

such as vehicle usage (CAR/VEH), cash tips (CAT), moving (MOV), miscellaneous (MIS)

are subject to taxes and require payable wages in order to collect the employee

share of taxes. Questions may be directed to Lisa Raihl at 405-521-3258, lisa.raihl@omes.ok.gov or Jean Hayes at

405-522-6300, jean.hayes@omes.ok.gov.

>> Back to Top

Military differential wage

payments are payments made to an employee during the period the individual is

performing service in the uniformed services while on active duty for a period

of more than 30 days and represents all or a portion of the wages an employee would

have received from the employer if the individual was performing services for

the employer.

Military differential pay is

includible as wages for income tax purposes on Form W-2, but is excludable from

social security and Medicare taxes. To correctly report military

differential wage payments, Time Reporting Code ‘MILDF’ (earnings code ‘MLD’)

must be used.

The military differential

pay is also included in for OPERS, OLERS, and URSJJ retirement contributions

and must be correctly coded in order for the information to be sent to the

retirement systems correctly.

Please refer to Title 72 O.S. §48

and OAC 260:25-15-44,

for additional information related to leave of absence due to military service.

>> Back to Top

When earnings are payable

after the death of an employee, the Payroll

Processing for Death of an Employee manual must be followed to ensure

proper processing. For payments to a spouse,

dependents, guardians or beneficiaries of a deceased employee that are made

through AP, the recipient(s) must be set up in the vendor file. Processing Step

1 in the manual states the agency can request a Vendor ID using the ‘Vendor

File Additions/Changes for Employees/Board Members’ form. This form has been

modified and is no longer valid for this type of vendor setup. Please submit a

completed IRS Form W-9

to Vendor Maintenance for payments to be made to a spouse, dependents,

guardians, or beneficiaries of a deceased employee. Requests to add or update

an employee Vendor ID made payable to the “Estate of …” an employee, may

continue to be submitted using the Form Adding Employees CORE Vendor Database. All forms should be submitted to Vendor Maintenance via

email to vendor.form@omes.ok.gov.

Forms may also be faxed to the updated number 405-521-3663 Attn: Vendor File

Maintenance.

>> Back to Top

Beginning in 2012,

the IRS mandated

Box 12 reporting

for the cost

of employer-provided health

coverage. The W-2 must show the amount in Box 12 with Code DD. To

correctly report the

cost of health

coverage, all payments (both employee and employer) made

for health insurance

must process through

the payroll system.

Failure to process

through payroll will

result in incorrect

reporting on the

W-2.

This reporting to employees

is for their information only. The

amount reported is not taxable and is only intended to inform them of the cost

of their health care coverage.

For questions

or more information, please

contact Lisa Raihl

at (405) 521-3258

or lisa.raihl@omes.ok.gov, or Jean Hayes at 405-522-6300 or jean.hayes@omes.ok.gov.

>> Back to Top

HIGHER EDUCATION PAYROLL

Payroll

claims for hours worked in fiscal years 2018 and 2019 on one payroll fund

transfer file will record payroll expenses to the institution’s operating

funds with bud refs 18 and 19. The claim number will begin with 19, which will

require that all class 78900 transactions on the PFT file be recorded with bud

ref 19. The first two digits of the claim number determine which 78900 budget

is used for the net payroll vouchers, so all 78900 transactions on the PFT must

be recorded with bud ref 19 to ensure the same allotment budget is used.

Please

ensure the FY 2019 78900 allotment budget is sufficient for the FY 2018

expenses paid in July and August 2019.

If

a payroll contains only FY18 expenses, then the claim number will be 18aaaxxxxx and

the PFT bud ref will be 18.

If

a payroll has FY18 and 19 expenses, then the claim number will be 19aaaxxxxx

and the PFT bud refs for the operating funds (290, 430, 700) will be as

applicable and the 789 bud ref must be 19.

If

a payroll contains only FY19 expenses, then the claim number will be 19aaaxxxxx and

the PFT bud ref will be 19.

>> Back to Top

HUMAN CAPITAL MANAGEMENT (HCM)

Effective July 1, 2018, Globe

Life and Accident Insurance Company and Family Heritage Life Insurance

Company will no longer be members of the Voluntary Payroll Deduction

program for the State of Oklahoma.

Employees should make alternative arrangements before ending

deductions through the payroll system for the State of Oklahoma. The individual

companies will be responsible for notifying policyholders about other methods

for paying premiums going forward after July 1, 2018. If you would like to

contact your representatives with these companies, they are as follows:

Globe Life and Accident Insurance Company

Payroll Code: AI65

Kathie Jenkins

Email: kjenkins@torchmarkcorp.com

Phone: 972-569-3278

Family Heritage Life Insurance Company

Payroll Code: AI66

Tray Warrior

Email: twarrior77@gmail.com

Phone: 918-617-3401

If you have questions about the VPD program,

please contact us at vpd@omes.ok.gov or 405-522-6970.

*These companies are

supplemental plans and do not affect the Life Insurance or Dependent Life

Insurance that is part of your yearly benefits enrollment.

>> Back to Top

TRAVEL

Effective

immediately all lodging receipts (original or copy) must be included with any

Form 19 travel voucher that pertains to overnight travel, even if the lodging

was an agency direct payment or paid with p-card. Lodging payments are limited to the allowed

rates. If the lodging cost is greater

than the amount allowed, the traveler should make the payment and be reimbursed

only for the allowed amount. The agency

should not make payments over the allowed amount, but if this happens the

employee’s reimbursement for other travel costs must be decreased by the

overpayment. Overnight travel claims received without

documentation of the cost of lodging will be rejected until the agency provides

the documentation and adjusts the voucher as appropriate.

>> Back to Top

ACCOUNTS PAYABLE

Central

Purchasing’s Ratification Agreement

and the Budgetary Agreement of Prior

Year Obligation processes are often confused. These documents are each required in certain

circumstances and if both situations exist, both documents are required.

The

Ratification Agreement is strictly a purchasing document to be

used when an agency fails to encumber funds for an expenditure by setting up a

purchase order. The agency must complete

a ratification form and submit a copy to the state purchasing director for

his/her records (not approval). A copy of the ratification agreement must be

attached to the voucher and it is paid unencumbered.

The

Agreement of Prior Year Obligation process is strictly a budgetary

issue for an expenditure that must be paid against a prior year where there is

no remaining budget because it was either used or lapsed. Agencies must complete an Agreement of Prior

Year Obligation form and submit it to their OMES budget analyst. The expenditure must be approved by the state

budget director. If approved, the

expense is considered a current year obligation and current year budget would

be used to make the payment. The payment is made unencumbered. A copy of the approved Agreement of Prior

Year Obligation form must be included with the voucher.

If

there are any questions on these “settlement” type processes, please send an email

to OMESTPAccountsPayable@omes.ok.gov.

>> Back to Top

A

reminder that there are no exceptions to the “Tax Snags” often levied on

vendors used by state agencies. When a vendor is snagged by the Oklahoma Tax

Commission via a tax warrant, agencies can’t enter into new contracts

with the vendor and any payments to the vendor are held for the vendor to work

out arrangements with the OTC. Any scheduled payments to the vendor may be subject

to assignment to the OTC if an agreements is not made between the taxpayer and

the OTC. This also applies to employees’ travel and other reimbursements when

there are tax snags on the employees (payroll excluded).

For

additional detail on these procedures, see the OMES Statewide Accounting

Manual, Chapter 50.90.04 OTC Tax Warrant Program (Vendor Snag Program), or send

an email to OMESTPAccountsPayable@omes.ok.gov.

>> Back to Top

|