PAYROLL

In

planning your work for October, it is important to remember that Columbus Day

is Monday, Oct. 10. Although not a state holiday, Columbus Day is a

federal/bank holiday. As a reminder, all payrolls and documents must be

received five business (5) days prior to the actual pay date to ensure adequate

time for audit and processing. Adherence to this policy will ensure payrolls

are processed to pay timely.

>> Back to Top

The

earnings codes listed below are setup in the HCM system to properly process

payments made to employees under a RIF or VOBO. Please contact Enterprise

Business Services (CORE) if your agency needs additional earnings codes.

VBO – VOBO/RIF

RBA Amounts - 18-month cost of health insurance (for employee only amount)

SEV –

Severance – lump sum payment up to $5,000

RLO -

Longevity (RIF, Retire) – prorated longevity amount for those individuals who

are retiring and are leaving under a RIF or VOBO. Because they are retiring,

the prorated amount is subject to retirement contributions.

LNS -

Longevity Severance – longevity amount for those individuals not retiring and

leaving under a RIF or VOBO. Additionally, used for the remaining amount a retiring

individual is receiving above the prorated amount subject to retirement.

NOTE: Only the

prorated longevity (RLO) amounts for those employees retiring are subject to

retirement wage reporting and contributions. Please be sure to use the correct

earnings codes for employees to receive their retirement credit. If an

incorrect earnings code is used and later discovered, the agency could be

responsible for paying both the employee and employer shares along with any

potentially lost earnings to the retirement system.

>> Back to Top

As a

reminder to agencies, certain types of earnings are eligible for deferral to

SoonerSave while others are not considered eligible compensation.

Annual

leave payout is generally eligible for SoonerSave deferral on termination of

employment. However, payments on severance from employment do not qualify

as compensation for SoonerSave deferrals. Therefore, payments under

voluntary buyouts (VOBO) and reductions in force (RIF) would be excluded from

deferral consideration.

Only compensation from an

agency that is attributable to services performed for the agency may be

considered as earnings from which SoonerSave deferrals can be

taken. This would include regular pay, overtime, shift differential and

other similar payments based on employment. If an amount would have been

paid had the employment continued, such as annual leave, then deferrals can be

taken.

Please

advise employees that changes in deferral amounts must be submitted to the

SoonerSave Administrator and approved before processing through payroll.

For additional information, agency personnel should contact their SoonerSave

Coordinator or the SoonerSave Administrative office at 1-800-733-9008 or

405-858-6781.

>> Back to Top

As we

approach the end of the calendar year, be reminded that the payroll system has

been structured to accommodate the reporting of non-cash, taxable fringe

benefits. Of specific concern to state employees, the following benefits should

be reviewed to determine if W-2 wage adjustments are necessary:

Group Term Life Insurance

Employee Use of State Vehicles

Maintenance, Car and Housing Allowances

Additional non-cash benefits

Reporting

of these benefits is required by state and federal law, and it is the

responsibility of the individual agency to ensure compliance. If the item is

not run through the payroll system in the current year, the employer can deduct

the taxes associated with the wage item on a following paycheck in the next

year, as a miscellaneous deduction. The state is responsible for timely

depositing the taxes. Any taxes associated with items not run through the

payroll system will need to be sent to OMES in a timely manner so the tax

deposits can be made and the items posted to the employee’s earnings record.

Under IRS

rules, an employer can choose to pay the employee’s share of taxes on group

term life, auto fringe, and other non-cash benefits. If the employer pays these

taxes without deducting them from the individual, those taxes must be included

as wages for federal, state, social security and Medicare wages (boxes 1, 3, 5,

and 16). This increase in the employee’s wages is also subject to employee

social security and Medicare taxes. This again increases the amount of

additional taxes the employer must pay.

Example:

Tom received a non-cash benefit valued at $100.00. The agency decides to pay

the employee’s taxes on all non-cash benefits. The employee’s taxes would be $7.65

[(100 x 6.2%) + (100 x 1.45%)]. This amount that the employer is paying for the

employee is another benefit to the employee and must be taxed [(7.65 x 6.2%) +

(7.65 x 1.45%)] = $0.58. This additional $0.58 is again taxable to the employee

[(0.58 x 6.2%) + (0.58 x 1.45%)] = $0.05. Total taxes to the employee are

$8.28, for total wages of $108.28. An easier way to calculate, is to “gross up”

the benefit. The benefit amount is divided by 92.35% (100% - 6.2% - 1.45%) and

the outcome is the gross wages to report. From this amount, the social security

and Medicare taxes are calculated. 100.00/92.35% = $108.28 (the taxable wage

amount). [(108.28 x 6.2%) + (105.28 x 1.45%)] = $8.28 (taxes).

Please

refer to the W-2 instructions and Publication 15A, Employer’s Supplemental Tax

Guide for additional information if needed. Also, please refer to OMES Human

Capital Management Division rules to determine whether these payments are a

valid pay plan for a particular agency.

>> Back to Top

Employee

overpayments that are collected in the next calendar year are to be repaid at

the gross overpayment amount in accordance with Internal Revenue Service

regulations. If an employee owes the agency, please be certain to let the

employee know if the amount is not paid in full by Dec. 31, 2016, the amount

they owe will increase to the gross amount.

In

accordance with 74 O.S. § 840-2.19, the agency must send a notice to the

employee within 10 days of identifying an overpayment. The employee then

has 30 days to respond to this notification. Employees have several

options for repaying overpaid payroll amounts:

- reduction of annual leave (for the

gross overpaid),

- reduction of current gross salary

(for the gross overpaid) in a lump sum or installments over a term not to

exceed the term in which the overpayment(s) occurred,

- lump-sum cash repayment,

- miscellaneous payroll deduction

(for the net overpaid) in a lump sum or installments over a term not to

exceed the term in which the overpayment(s) occurred,

- any combination of the above

options.

With the

calendar year end so close, the collection of any outstanding overpayments is

especially important and must be conveyed to employees who owe any monies back

to the agency. When an overpayment is paid back in a subsequent year, IRS rules

state that the employee must pay back at the gross amount because they had use

of the funds in the prior year and as such, they are taxable to that year.

Additionally, federal and state wages and taxes cannot be reduced for prior

years when repayments are made after the end of that calendar year.

For

example, John Doe was overpaid in August by $1,000.00 regular wages. This was

discovered in September and the agency calculated what the correct payroll

should have been. The net check difference is $743.50; the amount the employee

owes the agency if paying back by personal check or miscellaneous deduction in

the current year. If the employee does not pay this net amount back by Dec. 31,

2016, the employee owes the agency the full $1,000.00 gross overpayment.

If the

employee pays the gross amount back after year end, the applicable W-2,

Corrected W-2, or W-2C will only reflect a change in the Social Security and

Medicare wages and taxes. Since the employee received and had use of the funds

during the year of overpayment, the amount is still taxable for federal and

state purposes. The W-2 form will not correct Federal or State taxable wages or

income taxes. The employee may be entitled to either a deduction or credit on

their current year Form 1040, and should be advised to speak to their tax

accountant.

>> Back to Top

When an

employee chooses to pay back an overpayment using annual leave, the amount of

annual leave reduced should equal the gross amount of overpayment. In the past

there have been instances where agencies have incorrectly reduced the annual

leave by the net amount of the overpayment.

If an

employee pays back an overpayment using terminal leave, an OMES Form 94P must be

submitted to correct the retirement amounts reported on the check that included the overpayment. Terminal leave is not included in retirement wage

calculations; therefore, a payroll earnings adjustment is required.

>> Back to Top

The OMES

Form 94P has been updated and is available on the OMES website. The updated form, revised

7/15/2016, contains new fields for reporting the Pathfinder retirement plan.

The instructions have been updated as well. Please be sure to use the new

form on all overpayment refund requests.

>> Back to Top

ACCOUNTING

There are reports in the State Accounting System that relate to federal program reporting. These reports can be found within

the navigation for General Ledger reports – General Ledger > General

Reports. These reports can be very useful when reporting federal

expenditures for the Single Audit Report. However, they are only useful

if agencies are properly including the CFDA number on their transactions.

SEFA Expenditures

SEFA Revenue Report

SEFA Transactions Report

The CFDA numbers established by the US Office of Management

and Budget are five-digit numbers in the format of two digits for the federal

granting agency followed by a period then three digits assigned to the program

(XX.XXX). For example, CFDA number 10.555 is assigned to a program administered

by the US Department of Agriculture. The specific program is the National

School Lunch Program.

In the State Accounting System, the CFDA number is a nine

digit field using primarily numeric data. The first five digits correlate

to the federal CFDA number without the period ‘.’, and the last four are for

state agency use (XXXXXXXXX). Some agencies use the last four digits to

designate whether the expenditure is part of the federal share or the state

matching share. If the last four digits are not specifically assigned,

they are filled in with zeros.

If you receive a grant for which the CFDA number does not

exist in the State Accounting System, you can submit a case through the OMES service desk to have it added to the system. If you want to use the last

four digits for further breakdown, be sure to include that in your

request. For example:

105550001 – Nat’l School Lunch - Program Costs

105550008 – Nat’l School Lunch – Admin Costs

The State Accounting System allows a voucher to process with

a valid CFDA number. Although the CFDA field is not a required field in the

State Accounting System, the federal CFDA number should be included for

tracking and reporting purposes. The CFDA number can be set up in the purchase

order or the voucher can be populated with the CFDA number if the purchase

order does not contain it. This procedure allows the processing of the voucher

without having to submit a change order to add or correct the CFDA number on

the purchase order when ready to pay the voucher.

In addition to using the CFDA number on the disbursements,

deposits of federal funds should also include the CFDA number.

So the simple answer to the initial question is that you

should use the CFDA number anytime you are receipting or expending funds

related to federal grants or programs.

>> Back to Top

Effective immediately, agencies should submit their Forms 11

and 11a electronically. The completed and signed forms, with the required

backup, should be sent to the Central Accounting and Reporting group using the

following email. Hard copy submissions are no longer required and forms

should not be submitted using a facsimile machine (FAX).

accounting@omes.ok.gov

A single PDF file should be submitted for each account and

the file should include the required supplementary reports or

information. Optional backup detail can be included as well.

Multiple files can be attached to a single email submission. The file

name should follow a specific naming convention to allow for electronic filing

and sorting. The appropriate naming convention contains the following

elements: five-digit agency number; class funding number; month and year

(spaces are allowed in the file name). Examples of naming conventions are

shown below.

09000 79901 Aug 2017

09000 8090B Sep 2017

If you have any questions, contact Vivian Day at Vivian.day@omes.ok.gov.

>> Back to Top

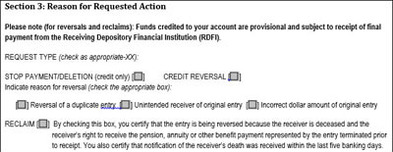

When submitting an OMES Form EWC - Electronic Warrant

(Payment) Cancellation, to cancel EFT payments, be sure to complete all

sections. This includes Section 3 - Reason

for the Requested Action, with the appropriate information.

Also, we have revised the EWC form to remove the Debit

Reversal option since it is not utilized for AP and Payroll EFTs. (Pages 1 and

2 of the EWC Form are revised)

Please refer to the following for selecting the

appropriate boxes for Section 3:

Select

the type of correction:

1) Stop

Payment/Deletion

2) Credit

Reversal

Select

the status of the Receiver (reason for cancellation)

a. Reversal

of a duplicate entry

b. Unintended

receiver of original entry

c. Incorrect

dollar amount of original entry

3) Reclaim

NOTE: Under the DCAR Forms, see the revised EWC form

and the EWC instructions for descriptions of the type of corrections, if

needed.

>> Back to Top

MISCELLANEOUS

Fraud attempts are increasingly targeting individuals within

businesses, government agencies and educational institutions to influence their

behavior. State agencies must be vigilant as they perform procedures to

verify requests for money movement (wire or ACH). Payment industry

experts say there has been a 91% year over year increase in the number of

targeted phishing attacks recorded globally. Many of these attacks are in the

form of email spoofing. Never initiate a payment or money transfer based solely

on email or telephone instructions, even from trusted sources. Validate by calling

the individual or entity requesting the payment at their known telephone

number. Never call a number provided via an email or popup message. Always

validate the sender’s email address and hover over the email address and/or hit

reply and carefully examine the characters in the email address to ensure they

match the exact spelling of the company domain and the correct spelling of the

individual’s name. Never give any banking or other confidential information to

an unexpected or unknown caller.

The Office of the State Treasurer (OST) has processes in

place to validate payment requests received from state agencies, but the

success of these processes depend on agency personnel properly validating

payments before they are submitted to OST for processing. If there are any

questions related to electronic payments, payment requests or OST processes

please contact Diedra O’Neil at diedra.oneil@treasurer.ok.gov.

>> Back to Top

On Sept. 23, 2016, an amendment to the NACHA Operating

Rules will become effective enabling same-day ACH payments. This amendment will

provide the option to financial institutions to originate certain same-day ACH

payments and mandate all receiving financial institutions to receive same-day

ACH payments. ACH credit transactions, except for international

transactions (IATs), payments to the federal government, and transactions above

$25,000, will be eligible for same-day processing.

Initially same-day ACH payments will be significantly more

expensive to process than future dated entries to allow financial institutions

to recover their costs for enabling and supporting this function. The Office

the State Treasurer (OST) will only originate same-day ACH credits on an

emergency basis. If your agency ever has such an emergency please contact the

Director of Banking and Treasury at OST, Diedra O’Neil (diedra.oneil@treasurer.ok.gov).

Agencies should NOT begin sending same-day effective dates in their payment

files, the entries will continue to be processed on the next valid, future

effective date.

>> Back to Top

|