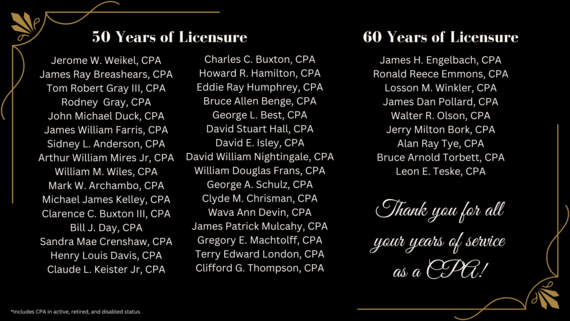

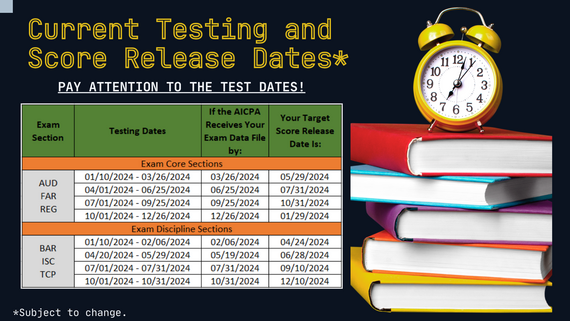

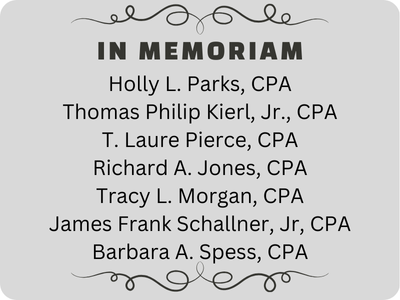

|

MEMBERS OF THE BOARD

Bryan Storms, CPA, Chair

Mark Whitman, CPA, Vice Chair John Curzon, CPA, Secretary

Sandy Siegfried, CPA

James "Rusty" Minnix, CPA

Jody Manning

Taylor Green

BOARD STAFF

Ashley Plyushko, CPA Executive Director

Rebekah Flanagan

Chief Accountant

Heather Grable

CPE Coordinator

Lauren Norcom

Licensing Coordinator

LaLisa Semrad

Enforcement Coordinator

Matthew Sinclair

Records Coordinator

Joey Wash

Peer Review Coordinator/CPO

Symone Chambers Examination Coordinator

Jason Zaragoza CPE/Enforcement Assistant

Melanie King

Office Manager/CPO

Mykal Kephart

Technical Assistant

CONTACT INFORMATION

Oklahoma Accountancy Board

201 N.W. 63rd Street, Ste. 210 Oklahoma City, OK 73116

Local: (405) 521-2397

Fax: (405) 521-3118

Website: oklahoma.gov/oab

The Oklahoma Accountancy Board Bulletin is the official publication of the Oklahoma Accountancy Board.

Need Help? Check Out These Guides!

|

Oklahoma Accountancy Board Elects New Officers for 2024-2025 Year

During the June 2024 meeting, the Board voted unanimously to elect three members to officer positions. Bryan Storms, CPA, was elected as Chair. Mark Whitman, CPA, was elected as Vice-Chair, and John Curzon, CPA, was elected to the Board Secretary position. These members will serve as officers from July 1, 2024, until June 30, 2025, when the Board will elect officers for the next year. We congratulate them on this achievement and thank them for their service!

Board Thanks Robin Byford, CPA

for Her Service

Robin Byford, CPA, was recognized by the OAB, during the June Board meeting, for her dedicated service to the Board as a member from July 1, 2019, through June 30, 2024. Ms. Byrd served as Board Chair from July 1, 2021, through June 30, 2022. She also served as a valuable member of several committees including the Executive Committee, Enforcement Committee, and the CPE/Experience Verification Committee. OAB members and staff wholeheartedly thank her for her service to the Board and the CPA profession.

|

2024 Quarter 1 Exam Statistics

Interested in seeing how candidates from Oklahoma and across the country did on the CPA exam during the first quarter of 2024? Click on the button below to see a deep dive

|

|

Competence:

More Than Just A Buzzword

Certified Public Accountants are held to a high standard. Many professions call for a well-educated competent workforce, but few have this call as part of their ethical code. Those holding the designation of CPA are one of the few. Under the AICPA Code of Professional Conduct, the requirement to complete one’s work competently and continually maintain said competency is laid out in the Principles of the Code under Due Care. Due Care defines competency as a combination of education and experience only starting with initial licensure. The requirement of continuous learning and improvement is life-long. The Code calls upon CPAs to maintain their competency in a way that will allow them to uphold the principles outlined.

The General Standards of the Code bring the concept of competency into tighter focus. Competency is that the member or their staff have the knowledge to perform the services or supervise those performing the services. This knowledge includes the professional standards, the technical subject involved, and the ability to apply sound judgement. If a CPA accepts an engagement, they are communicating to the client that it will be done competently. It is important to note that it is not expected that a CPA will not need to perform research during the engagement; however, it is expected that, with such activity, they will reach the point of competence as defined above. If a CPA is unable to do so, it may be time to refer the client elsewhere as outlined in the Due Care principle. It is up to the individual CPA to recognize where their competency ends and a referral is needed. The Scope and Nature of Services principle echoes this limitation.

The competency requirement applies to all CPAs both in public and private practice and regardless of whether the work being performed is paid or unpaid. Furthermore, it applies to all CPAs even those who are not holding out to the public.

How does the Board fit into this? Under Oklahoma Administrative Code 10:15-39-1, all Oklahoma registrants must conform in fact and appearance with the AICPA Code of Professional Conduct. This includes the requirements outlined in the Due Care, Nature and Scope of Services, and General Standard sections of the Code. As such, it is more than an ethical code for the profession. It is also required by the state of Oklahoma.

|

Josh Benefield, CPA (#18668)

Did you take the test on paper or on a computer? What is one of your best testing stories?

I was fortunate to get to take it on the computer. My test taking story was not the ‘best’, but it was memorable. I took one test in the first window of the year to get an experience of what the real test entailed. I had used a study program, and I am thankful I did, but there is nothing like taking the real thing. When the second window opened, I scheduled to take the other portions a month apart. I had planned to take the last test I needed at the end of the testing window. Nine days before my test, I was notified that the OKC testing center was going to shut down that day. The only other available appointment before the end of the window was going to be in Tulsa, 2 days after I found out that my first appointment was cancelled. Needless to say, I took that appointment, and my planned study schedule was destroyed.

Did you earn your experience while testing or after passing all the parts?

I earned my experience while testing. I tell people that studying for the CPA exam was a second job. After working all day, I would get back in front of the computer and study the rest of the evening, even on work trips. I’d like to think working and studying in tandem is what helped me pass the exams.

Do you work in public, government, industry, or academia?

Why did you choose that area?

My primary work is currently in government. I am the Deputy Chief Financial Officer for the National Indian Gaming Commission. I would say that my career chose me. I took the non-traditional route to becoming a CPA. After a few years teaching, I found my way into Tribal Gaming working for a CPA firm. After a couple of years doing that, I was able to get on with the NIGC as an auditor, finished the CPA, and rose through the ranks to my current position. I think it is easy to say that I would not be where I am if I hadn’t become a CPA.

What are your top tips for making sure a CPA’s renewal is completed on time?

The OAB reminders are helpful to make sure I don’t miss the deadline. I also have a renewal period that coincides with tax season, so between those two I haven’t had any issues with getting the renewal completed on time.

How do you keep track of your CPE? Excel spreadsheet, OAB Portal, or something else?

Before the portal, I was using the Excel spreadsheet, but the Portal has made it even easier to track. I save my CPE transcripts to a folder and at least once a quarter I go to the portal to report and upload my credits. When the end of the year comes around, I don’t have very much to log and know that I have met the requirements.

What is your preferred method of contact? Do you still prefer phone calls over email? My preferred method of contact depends on the topic of discussion and how much it is going to take to communicate the information. If it is a little, email is perfect. If it is a lot, then I find it easiest to pick up the phone and get it taken care of. Too much back on forth on emails gets annoying.

For Our Candidates

The What, When, and Where of the Jurisdiction ID

The Jurisdiction ID is used to assist NASBA in verifying that you are an approved Oklahoma candidate. A candidate will use this number one time when you set up your NASBA CPA Candidate account after the OAB has approved your first exam app and sent it to NASBA. It can be found in the approval email sent by the OAB once your Qualification Application is approved. If you are unable to find your approval email, you may call us for your Jurisdiction ID.

|

Upcoming Board Meeting

The next board meeting is August 16th at 10:00 AM in the Oklahoma Accountancy Board Boardroom at 201 NW 63rd, Ste 210, Oklahoma City, OK 73116.

These meetings are open to the public. If you wish to speak, you must notify the Executive Director before the meeting of the desire to speak and the topic to be addressed.

|

|

|

|

|

|