Update on New York’s Unemployment Insurance Trust Fund: Challenges Continue

Devastating job losses caused by the COVID-19 pandemic led to a record number of unemployment insurance (UI) claims in New York and other states. Benefits paid through such claims are part of the safety net, and are financed with federal and state payroll taxes collected from employers. As detailed by the Office of the State Comptroller in a September 2021 report, New York’s UI fund did not have sufficient funds to pay the surging claims, and began to borrow from the federal government starting in May 2020.

While many states had to borrow from the federal government to support UI claims, New York is one of only seven states or territories with UI funds that continue to be in debt to the federal government, and the size of the outstanding loan balance—$8.1 billion—is second only to California. In May 2022, New York State paid $1.2 billion of its federal loan, but New York’s UI debt has remained stubbornly high despite steady employment gains and State tax rates that have already increased to maximum permissible levels. If New York’s outstanding balance is not fully repaid by November 10, 2022, interest costs will mount, as will the federal portion of employers’ 2022 tax bills. Absent any significant federal or State action, employer costs will continue to grow, potentially impeding the State’s employment recovery amid growing economic uncertainty.

The Federal Loan

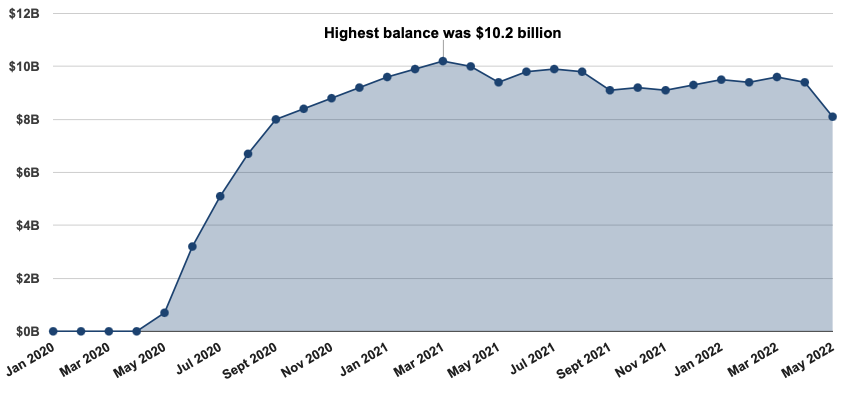

Pandemic-related unemployment claims surged during the COVID-19 economic shutdown and reached unprecedented levels; as a result, New York has drawn advances from the federal Unemployment Trust Fund (UTF) since May 2020 when its UI fund initially ran out of funds for paying benefits. The loan balance reached as high as $10.2 billion in March 2021, declined and then plateaued to an average $9.3 billion from September 2021 through April 2022. After a series of large repayments, the balance dropped to $8.1 billion by May 31, 2022, as shown in Figure 1.1

FIGURE 1: New York’s Monthly UTF Loan Balance During the

COVID-19 Pandemic

Interest due on New York’s advance has been limited to date because of federal pandemic legislation waiving such payments. The Families First Coronavirus Response Act first waived interest accrued on loans through December 2020. This date was extended by the Consolidated Appropriations Act/Continued Assistance Act and the American Rescue Plan (ARP) Act and the waiver ultimately lasted through September 6, 2021. Interest due from New York for the remainder of federal fiscal year (FFY) 2021 (which ran through September 30, 2021) totaled $13.5 million.2 Payment of this interest was largely deferred, with only $3.4 million paid.3 As of May 31, New York has accrued $113.4 million in interest due in FFY 2022 and will also pay an additional $3.4 million for interest accrued during 2021, for a total of $116.8 million in interest for FFY 2022.

Balance Remains High Despite Recovery and Increased UI Tax Collections

New York’s ability to repay the federal loan is directly tied to the strength of its economic recovery and the tax rates levied on employers. State UI tax rates vary based on employers’ payroll, UI benefits paid to former employees and the size of the State UI fund balance. Collections of UI taxes are deposited to the State’s fund for the payment of benefits. Although unemployment decreased dramatically in 2021, total benefit payments remained greater than total UI tax collections, contributing to the persistently high balance in New York’s outstanding loan.

Fewer Unemployed Individuals, Claims and Benefits Paid

Over the last year, improved employment in New York State has resulted in fewer unemployed individuals, UI claims and accompanying benefit payments. Since April 2020, New York State has added over 1.5 million jobs, recovering over 77 percent of jobs lost.4 After reaching a high of 16.5 percent in May 2020, the State unemployment rate has declined steadily to 4.5 percent in April 2022.5 UI claims in New York have decreased significantly in tandem with falling unemployment. In the first quarter of 2020, unemployed individuals totaled 403,000 and $829.4 million in regular UI benefits were paid. These numbers increased dramatically in the next quarter to 1.4 million unemployed individuals (a 248 percent rise) and $6.5 billion in benefit payments (682 percent). These high levels fell significantly by the end of 2020 and throughout 2021. In the first quarter of 2021, there were 850,000 unemployed individuals, decreasing to 505,000 in the fourth quarter, with commensurate benefits paid declining from $1.54 billion to $643 million. Moreover, first payments declined from more than 1.5 million in the second quarter of 2020 to 88,437 by the fourth quarter of 2021.6

Greater UI Tax Collections

State UI tax rates increased in 2021 from the prior year; combined with employment growth, these increases have bolstered tax collections by more than 54 percent from $2.1 billion in 2020 to $3.2 billion in 2021. These revenues are used to fund benefit payments and pay down outstanding balances.7

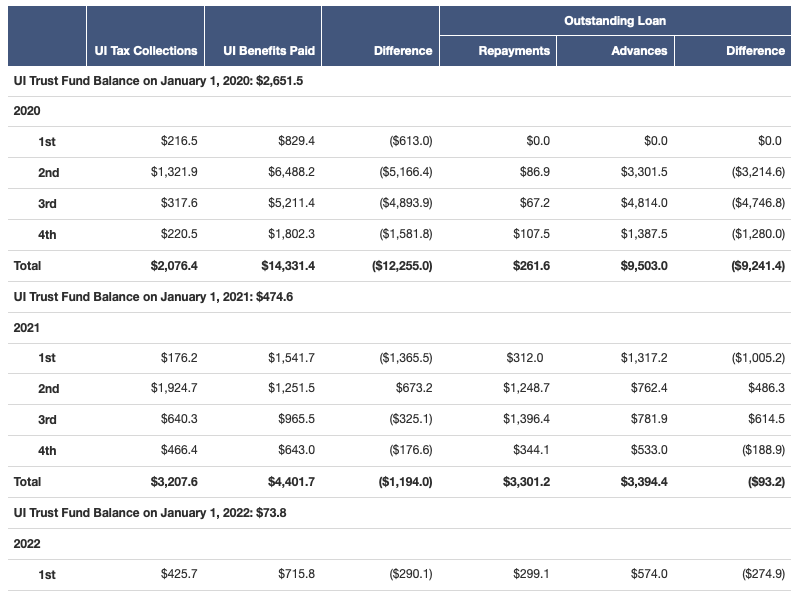

As shown in Figure 2, even though regular UI benefit payments decreased by almost $10 billion in 2021 and tax collections increased by more than $1.1 billion, total benefit payments remained greater than total tax collections, at $4.4 billion compared to $3.2 billion. As a result, New York’s UI fund continues to draw loans from the federal UTF. In 2021, the size of these loans decreased by almost two-thirds and repayments increased more than tenfold compared to 2020.8 Nevertheless, repayments have not yet been sufficient to significantly address the high level of borrowing required in 2020 and the State UI fund continues to draw advances in 2022.

New York’s large repayments in May 2022, however, indicate greater movement towards paying down its current advance. If the overall trend of decreasing UI benefit payments continues, or such payments remain at recent levels, and UI tax collections continue to increase (even with typical quarterly variation), New York will be able to continue taking fewer advances and making larger repayments.

FIGURE 2: New York’s UI Experience During the COVID-19 Pandemic

(in millions)

Source: U.S. Department of Labor, Employment and Training Administration

Responses by Other States

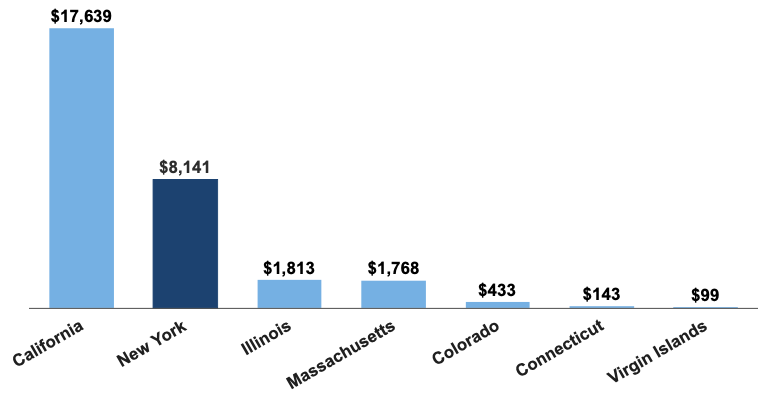

On January 1, 2021, 18 states and territories had outstanding loans with the federal UTF; as of May 31, 2022, there were seven states and territories with outstanding advances.9 On that date, loans drawn by California and New York summed to almost $25.8 billion, representing nearly 86 percent of the total balance in the United States; Illinois and Massachusetts held balances of about $1.8 billion each. (See Figure 3.)

FIGURE 3: States’ Outstanding Balances with the Federal UTF

(in millions)

Source: U.S. Department of Treasury

States have addressed their outstanding advances with the federal UTF by using surplus funding, issuing bonds, and modifying tax rates. In addition, the National Conference of State Legislatures notes that 20 states have used ARP Act State Fiscal Recovery Funds to repay these loans and/or replenish state UI funds.10 States that have taken such actions since September 2021 include Nevada, Ohio, Maryland, Texas and Minnesota.11

Going Forward

New York State has not applied any of its allocation of federal pandemic fiscal relief funds to its advance with the federal UTF, and the Enacted Budget for State Fiscal Year 2022-23 did not include use of federal or State funds for this purpose.

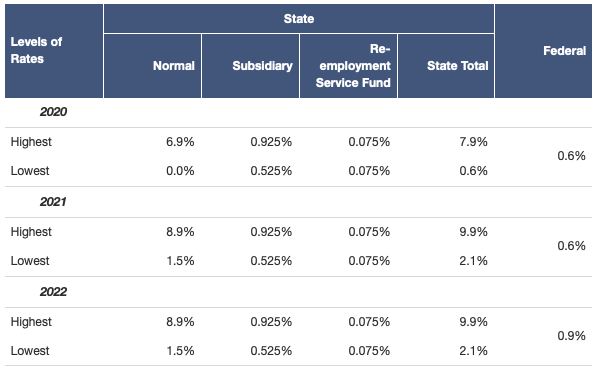

In 2022, State UI tax rates have remained at the highest levels allowed under law for the range of tax rates applied to employers, depending on their experience in the State’s unemployment insurance system. If New York does not repay its outstanding advance by November 10, 2022, the federal UI tax rate will increase by 0.3 percent to 0.9 percent for 2022. (See Figure 4.) This would represent an additional annual federal tax payment of $21 per employee; compared to 2020, the new rate would represent an increase in total tax payments of 30.5 percent for employers required to pay the highest UI tax rates and of 182.3 percent for those who currently pay the lowest rates. If New York continues to hold an outstanding balance on January 1, 2023, employers’ federal tax rate will go up to 1.2 percent, representing an additional cost of $42 per employee over current levels. This additional cost will increase by $21 per year for each employee as long as New York retains an outstanding balance on November 10 in the relevant tax year.12

FIGURE 4: Unemployment Insurance Tax Rates in New York

Endnotes

|