|

OUTREACH TO AFR NON-FILERS

State Comptroller DiNapoli speaks to local officials at the 2025 New York State Association of Counties Legislative Conference.

As we highlighted in the last issue of LGSA News, the number of local governments that are delinquent in filing their statutorily required Annual Financial Reports with our office has been rising. In response, we are reaching out directly to many non-filers to alert them to the problem and to offer our help. However, this effort will only be successful if we have up-to-date contact information. Please ensure that your municipal clerk regularly verifies your municipality’s contact information in our Contact Management System.

If you need help filing, below are some resources you can start using now:

Or simply call us. Staff at the OSC Regional Office near you can discuss filing options, answer your questions and, where appropriate, offer guidance. Staff at our Central Office can help with system access, filing options and filing questions.

We hope to hear from you soon!

|

|

IMPACT OF THE INFLATION REDUCTION ACT

Comptroller DiNapoli recently released a report detailing New York’s financial impact from the Inflation Reduction Act (IRA). The IRA of 2022 has been a source of approximately $2 billion in grants to New York’s farms, businesses, municipalities and state government. New York’s municipal governments and school districts have been awarded at least $365.8 million in grants for efforts to reduce greenhouse gas emissions, invest in climate resilience and address air pollution. Specific projects funded include reconnecting communities separated by highways, electrification of homes, cultivating urban forestry and purchase of electric school buses. In addition, “direct pay” provisions in the act allow municipalities and nonprofits that do not pay taxes to take advantage of tax credits for efficiency, renewable energy generation and other investments.

|

|

AVOIDING THE FISCAL CLIFF

Comptroller DiNapoli recently released a report that found New York’s local governments received significant funding from federal stimulus programs to help manage the challenges associated with the COVID-19 pandemic. However, in addition to this temporary funding source ending, state aid has stagnated, and sales and property tax revenues continue to moderate. While the recent high inflationary period has diminished, costs continue to rise. Going forward, local governments must carefully manage this new reality or potentially risk coming close to the edge of a “fiscal cliff.”

|

|

An Audit Is Scheduled – What Happens Next?

To demystify the process for what happens after receiving notification that the Division of Local Government and School Accounting will be performing an audit, we have prepared a brochure, Understanding the Audit Process. This brochure explains the audit process from start to finish and offers insights into what to expect when auditors are on site to conduct the audit.

After the audit is completed and the draft audit report is provided to officials, Responding to an OSC Audit Report: Audit Responses and Corrective Action Plans should be consulted. This brochure explains the difference between the audit response and the corrective action plan and provides useful tips for what to include in each document. A draft template is offered to assist with writing the corrective action plan.

|

|

NON-CALENDAR FISCAL YEAR END MUNICIPALITIES IN A FISCAL STRESS DESIGNATION

The following nine municipalities with a non-calendar fiscal year end were designated in a fiscal stress category as shown below after being assessed in our Fiscal Stress Monitoring System. The results are based on the municipalities’ 2024 Annual Financial Reports and were released to the public in April 2025.

In addition, 20 percent of local governments that would have been included in this release were delinquent in filing the statutorily required Annual Financial Report and as a result did not receive a score. To view the full listing of entities that were not filed in time for this release, click here.

|

|

UPCOMING CHANGES TO MUNICIPAL WEBSITES

New York recently enacted legislation that affects county, city, town and village official websites. A significant change is that these websites must use a “.gov” domain name to help the public identify these sites as the official, trusted website belonging to a local government. In addition, local governments will be required to regularly update their official websites with certain information, including, but not limited to the following:

- Their most recently filed annual financial report;

- Information about how website visitors’ personal information is collected and used; and

- Access to the municipality’s codes, local laws and resolutions.

These requirements apply to local governments with a population of at least 1,500 (as shown by the latest decennial federal census), beginning December 21, 2025. Local governments under this population threshold will need to comply to the extent practicable.

The State Committee on Open Government has issued a memorandum which provides more information on the new requirements. To learn more about obtaining a “.gov” domain name, see get.gov.

|

|

|

|

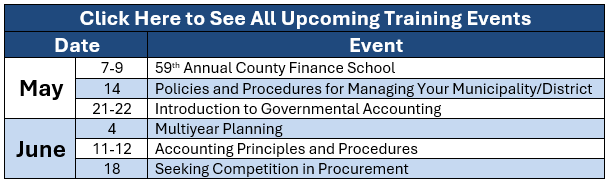

Upcoming Training Events from

The Academy for New York’s Local Officials

|

|

|

|

|