|

The application permit for Flood Mitigation Assistance and Building Resilient Infrastructure and Communities grant programs opens on September 20, 2022 and closes on November 18, 2022. Interested communities must have sub-applications submitted through the FEMA Go system by the deadline. Interested communities are encouraged to work through the County and State Offices of Emergency Management.

Details regarding these programs can be found on the FEMA website or through the following grants.gov links:

Back to top.

If Federal funds are utilized for the rehabilitation or construction of structures, new policy related to the reinstatement of Presidential Executive Order 13560 will apply if it is funded with FEMA and Stafford Act disaster funds (e.g. HMGP, FMA, HMA, CDBG-DR funds). It is also expected that the Department of Housing and Urban Development rulemaking will also follow this policy which is describe in FEMA Policy 104-22-003 Partial Implementation of the Federal Flood Risk Management Standard for Public Assistance (Interim). This policy is applicable to walled and roofed buildings (including manufactured homes and gas or liquid storage tanks. It requires that the Local Design Flood Elevation for critical actions be set at the best available FEMA Base Flood Elevation plus three feet or the 0.2% annual chance/500-year flood, which also must be adjusted for wave action in tidal areas or the Local Design Flood Elevation if it is more stringent. Non-critical actions would have to meet a minimum of the best available Base Flood Elevation plus two feet or the Local Design Flood Elevation if it is more stringent. Please note that the Local Design Flood Elevation is reflective of the State minimum floodplain standards under the Flood Hazard Area Control Act, the Uniform Construction Code minimum freeboard requirements as described by ASCE 24-14, and any more stringent floodplain requirements in a local flood damage prevention ordinance.

Back to top.

Image of an engineered flood vent.

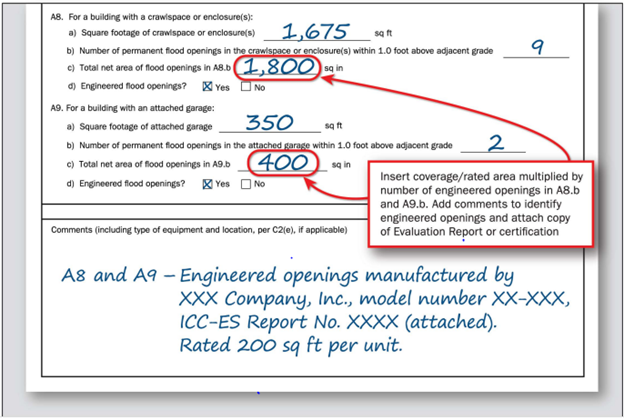

Unlike non-engineered flood openings, which must have a ratio of 1 square inch of opening for every 1 square foot of enclosed foundation space, engineered openings are documented using a coverage/rated area rather than a direct measurement of the engineered opening size. This means that it is possible that the opening size to enclosure area may be less than the 1 square inch to 1 square foot ratio.

When engineered openings are used, the coverage/rated area rather than the opening measurements must be documented by a surveyor on the Elevation Certificate and either the product’s Evaluation report or the design professional’s documentation must be included and referenced on the Certificate. The surveyor must also measure the square footage of the vented enclosure.

Section 9 of Technical Bulletin 1, Requirements for Flood Openings in Foundation Walls and Walls of Enclosures Below Elevated Buildings in Special Flood Hazard Areas (2020), provides detailed guidance on how these openings should be documented in an Elevation Certificate and what information must be in an Evaluation report or in the design professional’s documentation. The figure below, from Technical Bulletin 1, also shows how this information must be documented in the elevation certificate.

Technical Bulletin 1, Requirements for Flood Openings in Foundation Walls and Walls of Enclosures Below Elevated Buildings in Special Flood Hazard Areas (2020)

In addition to updated guidance on engineered openings, other updates to Technical Bulletin 1 include:

- Clarification on unusual configurations such as sloping sites, multiple enclosed areas, large enclosed areas and sites with shallow flooding.

- Guidance on above-grade enclosed areas and two-level enclosures.

- Expanded discussion on completing the National Flood Insurance Program Elevation Certificate, including information on non-engineered openings.

Back to top.

Example of dry floodproofing

Mixed use buildings with more than 5 residential units above the Local Design Flood Elevation and non-residential uses below this elevation require very specific floodplain permitting to ensure the safety of all users of the building and the protection of property. Technical Bulletin 3 , Requirements for the Design and Certification of Dry Floodproofed Non-Residential and Mixed-Use Buildings Located in Special Flood Hazard Areas which was published in 2021 requires that building residents have a non-dry-floodproofed exist from the structure that is separate from any dry-floodproofed non-residential space. Additionally, all residential uses such as laundry, mail, and recreation rooms related to residential uses and any utilities servicing residential areas must also be above the Local Design Flood Elevation.

Other updates to Technical Bulletin 3 include:

- Discussion of the factors and planning considerations that influence the decision-making process when determining the feasibility of dry floodproofing a building.

- Step by step discussion regarding dry floodproofing design requirements.

- An example seepage calculation illustrating how to determine if the structure can be considered as “substantially impermeable.”

- Instructions for completing the National Flood Insurance Program Floodproofing Certificate.

Mixed-use buildings also may have underground parking garages. In 2021, Technical Bulletin 6 , Requirements for Dry Floodproofed Below-Grade Parking Areas Under Non-Residential and Mixed-Use Buildings Located in Special Flood Hazard Areas was also updated to include the following:

- Identification of issues specific to dry floodproofing below-grade parking areas.

- References to Technical Bulletin 3 for extensive guidance on design requirements.

- Updated discussion on design considerations such as protecting points of entry, managing internal flow of seepage, and equalization of flood loads vertically in multi-level below grade parking areas.

Information regarding elevator shafts and foundation openings can also be found in Technical Bulletin 4 Elevator Installation for Buildings Located in Special Flood Hazard Areas in Accordance with the National Flood Insurance Program (June 2019).

Back to top.

The National Flood Insurance Program floodplain management regulations in 44 CFR 60.3 require that the design and construction of manufactured home and recreational vehicle foundations must meet the same A zone and V zone requirements as other structures. A previous exception in 44 CFR 60.3c(12) for placement in an existing manufactured home park, which allowed a 36 inch elevation is superseded under State law by the Flood Hazard Area Control Act (N.J.A.C. 7:13 – “FHACA”), which regulates these homes as habitable structures and requires that the lowest floor for a single family dwelling or duplex “is set at least one foot above the flood hazard area design flood elevation and no lower than the elevation required under the Uniform Construction Code, N.J.A.C. 5:23”.

The definition of a “habitable structure” in FHACA, is defined as:

“a building that is intended for regular human occupation and/or residence. Examples of a habitable building include a single-family home, duplex, multi-residence building, or critical building; a commercial building such as a retail store, restaurant, office building, or gymnasium; an accessory structure that is regularly occupied, such as a garage, barn, or workshop; mobile and manufactured homes, and trailers intended for human residence, which are set on a foundation and/or connected to utilities, such as in a mobile home park (not including campers and recreational vehicles); and any other building that is regularly occupied, such as a house of worship, community center, or meeting hall, or animal shelter that includes regular human access and occupation. Examples of a non-habitable building include a bus stop shelter, utility building, storage shed, self-storage unit, construction trailer, or an individual shelter for animals such as a doghouse or outdoor kennel.”

Back to top.

Both manufactured homes and recreational vehicles can obtain National Flood Insurance Program Insurance. The NFIP Standard Insurance Manual (the “Insurance Manual”) defines a manufactured home as a “structure built on a permanent chassis, transported to a site in one or more sections, and affixed to a permanent foundation.” It also defines a “travel trailer” as “without wheels, built on a chassis and affixed to a permanent foundation” and states that they are “eligible for flood coverage where regulated under the community’s floodplain management and building ordinances or laws.”

However, to be eligible, the Insurance Manual also requires that for manufactured homes and recreational vehicles must:

- "Be affixed to a permanent foundation that may be a poured masonry slab,

foundation walls, piers, or blocks, so that the wheels and axles of the mobile

home do not support its weight; and

-

Be anchored to a permanent foundation to resist flotation, collapse, or lateral

movement:

- By providing over-the-top or frame ties to ground anchors;

- In accordance with manufacturer’s specifications; or

- In compliance with the community’s floodplain management requirements.”

For manufactured/mobile homes continuously insured since September 30, 1982, the Insurance Manual allows renewals under the previously existing requirements if they meet the following conditions:

- "Are affixed to a permanent foundation in compliance with the foundation and

anchoring requirements at the time of placement; and

- Are adequately anchored, which means the foundation support system must

secure the manufactured or mobile home into the ground sufficiently to resist

flotation, collapse, and lateral movement caused by flood forces, including wind

forces in coastal areas.”

Because all development in a floodplain must be overseen by a Floodplain Administrator, it is imperative that Floodplain Administrators ensure that any new and substantially improved new or substantially improved manufactured homes or recreational vehicles are given permits for the placement and inspection of foundations. Additionally, Floodplain Administrators must ensure that any recreational vehicles in the floodplain which are not on permanent foundations be moved at least twice a year to comply with prohibition against placement for more than 180 consecutive days in the floodplain, be registered and licensed, and be “road-ready”. Ideally, the Floodplain Administrator would observe the movement of these vehicles and might also recommend winter relocation to an area outside the floodplain. It is also recommended that any unsecured mobile home be removed in advance of predicted flooding to prevent damage to other structures and downstream obstructions that worsen flooding outside of the regulated floodplain. If a recreational vehicle is unlicensed, unregistered, or otherwise not “road-ready” and is located in a floodplain on a non-existent or non-compliant foundation, the Floodplain Administrator may require that they be built on compliant foundations or may regulate these vehicles as “unsecured materials” under the Model Code Coordinated Ordinance as appropriate.

Because these homes are often purchased with Federal Housing Association or other Federal funds, it is very important to understand the economic factors related to manufactured homes and recreational vehicles and homeowner finances after a flood.

- The maximum Federal Housing Association loan for a manufactured home is $69,678 and for a manufactured home with land it is $92,904. The mortgage term is 20 years for the home and 15 years for the land. The maximum payout under the NFIP Standard Insurance Policy is $250,000 for a manufactured home and a qualifying recreational vehicle provided that the insured structure is at least 16 feet wide and is larger than 600 square feet. Applicants for insurance are required to list the make, year of manufacture, model number, and serial number of the home which establishes the initial replacement cost prior to any depreciation.

- Depending upon the amount of insurance carried by the homeowner, the home’s depreciation and the home’s pre-damage condition, that $250,000 maximum claim amount could be adjusted downward. In establishing a claim amount , an adjuster can consider replacement cost, the home’s actual cash value, or a use a process which considers a special loss settlement. This process considers the cost to set up a replacement home on the existing foundation and the cost of any additions but it may not consider the cost to comply with construction codes unless the home is substantially damaged and can qualify for Increased Cost of Compliance funds.

- Manufactured homes and recreational vehicles are considered personal property in New Jersey rather than real estate. Interest rates for borrowing are generally higher than for conventional real estate loans. These homes can be repossessed under N.J.A.C. 2A:18 et. seq. with notice given to the Division of Motor Vehicles and any lienholders with security interested recorded with the Division of Motor Vehicles. If insurance is insufficient to cover the cost of repair or replacement, homeowners may declare bankruptcy rather than continue paying their loan.

Mitigation options after a flood event are generally home relocation or foundation elevation. (Buyouts are only possible if the owner owns both the home and the land where the home is placed. Floodproofing is an option only for non-residential manufactured homes provided that a licensed NJ Professional Engineer or NJ Licensed Architect certifies the design.) This means that it is even more important to ensure that these homes are properly elevated and anchored at NFIP insurance policy application and in advance of any flood event. Because these homes are often placed in manufactured home parks or campgrounds where the owner pays a ground lease to the landowner, any loss of income to the landowner could be pursued through post-disaster recovery programs and buyouts may be possible if the flood impacted areas are no longer rented to tenants with permanently placed manufactured homes and recreational vehicles.

Back to top.

An earlier version of the New Jersey Model Code Coordinated Ordinance required that all new and substantially improved manufactured homes placed in flood zones have foundations built in accordance with Section 322 of the International Residential Code. The new version requires that new manufactured homes have foundations built in accordance with the Department of Housing and Urban Development Regulations 24 CFR 3285.302. The Uniform Construction Code does not issue permits or inspect foundation design for installations of new manufactured homes because the HUD regulations supersede State law. However, the Uniform Construction Code issues permits and inspects foundations for existing manufactured homes undergoing substantial improvements. More information on the background for this decision is found here in the January 7, 2019 rule proposal links.

While HUD regulates the installation of manufactured homes, it defers to engineer or architect installation designs when these homes (including certain non-self-propelled recreational vehicles under the regulation’s definition) are not designed by the manufacturer to withstand flood impacts and are located in a flood zone.

24 CFR 3285 .302 Flood hazard areas.

In flood hazard areas, foundations, anchorings, and support systems must be capable of resisting loads associated with design flood and wind events or combined wind and flood events, and homes must be installed on foundation supports that are designed and anchored to prevent floatation, collapse, or lateral movement of the structure. Manufacturer's installation instructions must indicate whether:

(a) The foundation specifications have been designed for flood-resistant considerations, and, if so, the conditions of applicability for velocities, depths, or wave action; or

(b) The foundation specifications are not designed to address flood loads.

The manufacturer’s foundation design, specifications, and stated conditions of applicability for velocities, depths, or wave action should meet or exceed the conditions present at the proposed foundation location so that the home is reasonably safe from flooding. If the manufacturer does not specify the home for use at the conditions found at the site, the alternate design requirements of 3285.301(c) and (d) would apply. These are as follows:

(c) All foundation details, plans, and test data must be designed and certified by a registered professional engineer or registered architect and must not take the home out of compliance with the Manufactured Home Construction Safety Standards. (See 3285.2, Manufacturer Installation Instructions).

(d) Alternative foundation systems or designs are permitted in accordance with either of the following:

(1) Systems or designs must be manufactured and installed in accordance with their listings by a nationally recognized testing agency, based on a nationally recognized testing protocol; or

(2) System designs must be prepared by a professional engineer or a registered architect or tested and certified by a professional engineer or registered architect in accordance with acceptable engineering practice and must be manufactured and installed so as not to take the home out of compliance with the Manufactured Home Construction and Safety Standards (part 3280 of this chapter).

In recognition of this regulatory change and to better address foundations in flood zones for these homes, the Model Code Coordinated Ordinance now requires the following language in Section 501.3 for foundations:

“501.3 Foundations. All new, relocated, and replacement manufactured homes, including substantial improvement of existing manufactured homes, shall be placed on foundations as specified by the manufacturer only if the manufacturer’s installation instructions specify that the home has been designed for flood-resistant considerations and provides the conditions of applicability for velocities, depths, or wave action as required by 24 CFR Part 3285-302. The Floodplain Administrator is authorized to determine whether the design meets or exceeds the performance necessary based upon the proposed site location conditions as a precondition of issuing a flood damage prevention permit. If the Floodplain Administrator determines that the home’s performance standards will not withstand the flood loads in the proposed location, the applicant must propose a design certified by a New Jersey licensed design professional and in accordance with 24 CFR 3285.301 (c) and (d) which conforms with ASCE 24, the accepted standard of engineering practice for flood resistant design and construction.”

In addition, unlicensed/unregistered recreational vehicles which are not “road-ready” and are kept onsite more than 180 days in a regulated flood zone must also be placed on foundations that meet the local design flood elevation. 24 CFR 3285 is applicable to all recreational vehicles except for self-propelled recreational vehicles because it defines a “manufactured home” as being “one or two sections, which in the travelling mode are 8 feet or more in width or 40 body feet or more in length, or which when erected on site is 320 or more square feet, and which is built on a permanent chassis and designed to be used as a dwelling with or without a permanent foundation when connected to utilities”. The applicable square footage is based on the structure’s exterior dimensions when constructed on site and also include “all expandable rooms, cabinets, and other projections containing interior space”. To reflect the applicability of the HUD regulations to certain recreational vehicles, Section 601.3, has also been revised as follows:

“601.3 Permanent Placement. Recreational vehicles that are not fully licensed and ready for highway use, or that are to be placed on a site for more than 180 consecutive days, shall meet the requirements of Section 801.2 for habitable buildings and Section 501.3.”

Floodplain Administrators should also be aware that 24 CFR 3285.102 affirms the permit applicant’s and the installer’s responsibility to determine whether the proposed manufactured home site lies partly or wholly within a Special Flood Hazard Area. It also requires that before an installation method is agreed upon, the map and supporting studies should be utilized to determine the flood hazard zone and base flood elevation of the site. This section also references parts of 44 CFR 59 and 60 as well as 24 CFR 3285.903 which specifically mentions an “LAHJ”, which is a Local Authority Having Jurisdiction. A LAHJ is defined as “The state, city, county, city and county, municipality, utility, or organization that has local responsibilities and requirements that must be complied with during the installation of a manufactured home” and would include permitting performed by an NFIP participating community.

Back to top.

Rising Together New Jersey is asking people to share their flood stories to better prepare people to rise together in the future. See the flyer below and visit their website for more information and how to share your story.

Back to top.

|