Water Talk Newsletter - Winter 2017

December 27, 2017

By Ceil Strauss,

MNDNR, State Floodplain Manager

You are the local zoning authority and you get an angry call

from a resident. “My bank is telling me

I’m in the floodplain and I have to buy flood insurance. That’s crazy! I’ve never been in the floodplain

before.”

What do you tell them?

It depends . . .

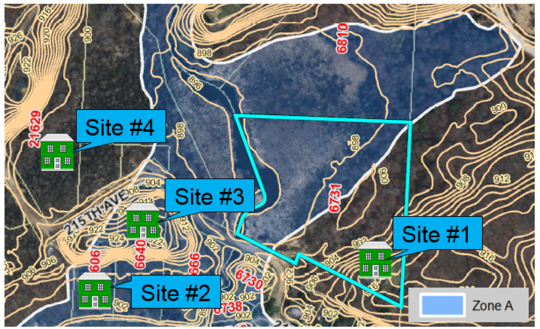

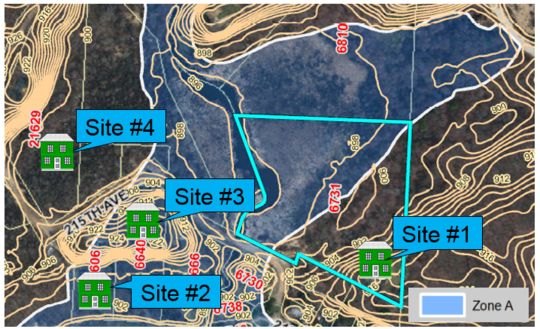

What would your answer be for the four scenarios shown below?

Source: MnDNR; background adapted from Anoka County Floodplain Mapper

See answer at bottom of this newsletter.

By Dan Petrik,

MNDNR, Land Use Specialist – Shoreland and River Related Programs

Adopting or amending an ordinance can be a major planning project

requiring research, public engagement, multiple revisions, and public hearings.

Additionally, adopting or amending a shoreland ordinance also requires DNR involvement

to review and approve the ordinance, which adds another step that must be

incorporated into the project. As the number of stakeholders increases, so does

the potential complexity, conflict, and time needed to successfully adopt an

ordinance.

|

The DNR has launched a new shoreland ordinance review and

approval process that is designed around local government public engagement processes

and uses a project management approach to better communicate roles,

responsibilities, and timing for a smoother adoption process.

Local governments have been required to protect shoreland

resources through development standards established in state rules through

shoreland ordinances since the early-1970s. As the state agency responsible for

administering the shoreland program, the DNR’s resources, roles and expectations

for reviewing and approving local ordinances have varied over time and

geographic area. This lack of

consistency has created some problems for local governments and the DNR including:

-

Misalignment of DNR’s review and approval

schedule with local government adoption processes, leading to insufficient time

for DNR to review ordinances, which has caused delay and frustration for local

governments.

- Often incomplete/insufficient proposed ordinance

submittals and documentation from local governments for DNR to determine

compliance with rules

- Occasional, incomplete follow through by DNR

and/or local governments resulting in adoption of noncompliant shoreland

ordinances.

The new process provides clarity on DNR and local government

roles, expectations, and timing, with the goal of providing local governments

with conditional approval on proposed ordinances and amendments in time for

public hearings. We believe that this process will help reduce delays and

potential conflicts in getting shoreland ordinances and amendments adopted. Key

highlights include:

- Early engagement with the DNR, establishing a

goal of a 30 day review period for DNR conditional approval.

-

A step-by-step process aligned with local

government ordinance amendment procedures and public processes, with clear

roles and tasks in each step so there are no surprises.

-

One email address to use for submitting all

ordinance documents to the DNR.

-

Completion of a checklist by local government

that provides a “citation crosswalk” between provisions being changed in the

local ordinance relative to the DNR model shoreland ordinance to encourage

conforming language and streamline communications during DNR review.

-

Clarity on when deviation from the shoreland

rules requires offsetting higher standards and expectations of how these

deviations from key protection provisions are evaluated by the DNR.

Please visit our webpage

to learn more about this new process. If you have specific questions or want to

discuss a new ordinance or amendment, please contact your area hydrologist. If

you are considering amendments to your shoreland ordinance or developing a new

ordinance, please consider using the shoreland

model ordinance; doing so will speed up review and approval.

By Ceil Strauss,

MNDNR, State Floodplain Manager

The Summer 2017 Water

Talk issue included a

brief article on the June 23, 2017 Supreme Court ruling on Murr et al. v.

Wisconsin et al., noting the court ruled in favor of the State of Wisconsin

on a regulatory takings case.

The Murr et al. v. Wisconsin et al. case involved landowners

on the St. Croix River in St. Croix County, Wisconsin. The petitioners own two adjacent lots – that

are each less than one acre - adjacent to the Lower St. Croix River within an

area protected under federal, state, and local law. Those regulations prevent

use or sale of adjacent lots under common ownership unless they have a least one

acre of land suitable for development. The landowners wanted to sell one of the

lots in 2006 and use the proceeds for improvements to the remaining lot.

The landowners applied for a variance, and the St. Croix

County Board of Adjustment denied the request. The landowners filed suit and

the case worked its way up to the U.S. Supreme Court, resulting in the June 23,

2017 ruling.

Does this Decision

Affect Minnesota?

Minnesota has similar laws to those in Wisconsin requiring

the combination of contiguous nonconforming (or substandard) lots under common

ownership that the court found were not

regulatory takings. As

is noted in the Murr

et al. v. Wisconsin et al. ruling, 1973

Wisconsin statutes authorized the Wisconsin Department of Natural Resources to

promulgate rules limiting development

in order to

“guarantee the protection

of the wild, scenic

and recreational qualities

of the river

for present and future

generations.” Wis. Stat. §30.27(l) (1973). Minnesota has several programs

authorized by the state legislature with similar goals to protect the state’s lakes

and rivers for present and future generations, including: Shoreland

Management Program, Floodplain

Management Program, Wild

and Scenic Rivers Program, Lower

St. Croix Riverway Program and the Mississippi

River Corridor Critical Area Program.

How Has Wisconsin

Reacted?

|

In response to the

Supreme Court ruling, the State of Wisconsin’s legislature passed 2017 Wisconsin

Act 67:

-

limiting the authority of local governments to

regulate development on substandard lots and to require the merging of lots;

- requiring political subdivisions to issue a

conditional use permit under certain circumstances;

-

giving standards for granting certain zoning

variances;

- amending local ordinance authorities related to

repair, rebuilding, and maintenance of certain nonconforming structures; and

- Limiting restrictions regarding the right to display

the flag of the United States.

The Wisconsin Act amends enabling statutes for counties

(Chapter 59), towns (Chapter 60), and cities (Chapter 62).

This follows 2015 Wisconsin Act

55 – the state’s 2015-2017 biennial budget - which included language amending

the Wisconsin Shoreland Management regulations to prohibit higher local

standards. Wisconsin staff prepared a summary of those changes in an October

1, 2015 memo on 2015 Wisconsin Act 55 and Shoreland Zoning.

|

By Matt Bauman,

MNDNR Floodplain and Shoreland Planner

If you aren’t already enforcing it, freeboard beyond the

statewide minimum is an easy higher standard to enforce and can save a

community a few headaches. Even if you’re in a community that may not typically

embrace higher standards, a good economic argument can be made for safe and

sustainable floodplain regulations, since your residents and businesses will

have less impacts during flood events and can save money on flood

insurance. We’ll dig into a few reasons for why and how you should be enforcing

a higher freeboard.

Ease of

Administration

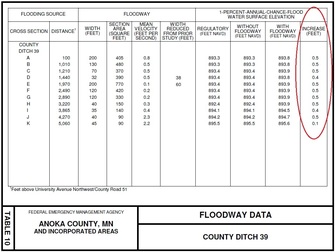

If you don’t know what stage increase is, or don’t know how

to find it, you may have unknowingly been permitting floodplain violations.

Minnesota Rules (6120.5700, subp. 5) define flood protection elevations as:

“…a point not

less than one foot above the water surface profile associated with the regional

flood plus any increases in flood stages attributable to encroachments

on the floodplain…” (emphasis added).

In

a nutshell, stage increase accommodates for permitted filling in flood fringe

areas. Finding this stage increase involves digging into your Flood Insurance

Study (FIS), which is not familiar to many administrators. When the average

Minnesota community processes so few floodplain permits each year, it’s easy to

understand how stage increase can be overlooked. Even if you understand how to

find this information, are you confident that your successor will? If stage

increase ever gets overlooked, and the structure gets flooded down the line,

the community is setting themselves up for potential liability.

|

An easy safeguard to ensure you don’t get burned (or

flooded!) by forgetting or miscalculating stage increases is to amend your definition

for “Regulatory Flood Protection Elevation” by removing the one foot of

freeboard plus any stage increase language, and administer a two foot freeboard

instead. In Minnesota, stage increases are half a foot or less*, so adding

a foot of freeboard, for a total of two feet, will always be higher than the

minimum one to 1.5 feet of freeboard plus stage increase.

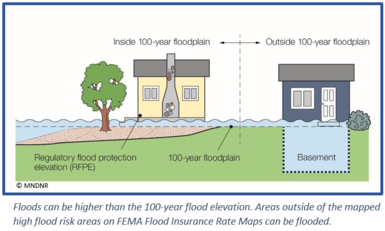

Protection from Large Events

Flood levels often exceed the 100-year flood elevation, as has

been seen all around the state with increasing frequency. In fact, the Minnesota

State Climatology office has assembled a

list of 15 “Mega-Rain Events” - where the six inches of rain covered at

least 1,000 square miles and the core exceeded eight inches - and seven of those occurred in the last 15 years!

|

Many floodplain maps were created long ago, using no

supporting data or outdated modeling techniques. Others predate

developments that have altered local hydrology and increased the level of runoff. In

addition, older maps often are based on studies using outdated precipitation data

such as the 1960 Technical Paper 40 (TP-40). New studies use NOAA’s 2013 Atlas

14 data, which reflects an additional 50 years of records and more extensive

rain gage network, and shows 20 to 30 percent higher 100-year, 24 hour

precipitation amounts in most of Minnesota.

To tackle these realities, many communities have elected to

carry out updated modeling based on Atlas 14 precipitation data or future development. These updated models can provide technical backbone

to support the enforcement of higher standards.

Economic Sense

When floods cause damages to homes and businesses, or impact

basic community services like water and power, there are costs for: flood

response, replacement of damaged buildings and contents, and temporary or long-term

loss of business or employment.

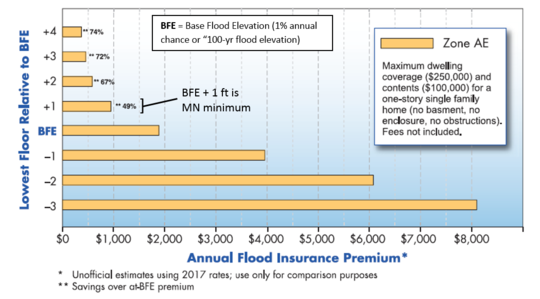

In addition to reducing impacts during a flood, building higher with

additional freeboard or updated modeling can lead to significant savings on

flood insurance for homeowners and businesses. See the FEMA sourced graphic

below showing how flood insurance costs drop dramatically as the lowest floor

gets to two or more feet above the Base Flood Elevation (the one percent

annual chance flood, or the “100-year flood”).

For More Information on Higher Standards

Communities interested in exploring higher standards are

encouraged to contact DNR floodplain staff.

* Minnesota Rules 6120.5700, subp. 4, A. allows a stage

increase of up to 0.5 feet if that does not “increase flood damage potential,”

which has been interpreted as any impact on existing structures. Note that

stage increases are higher on the North Dakota border since the combination of

Minnesota and North Dakota laws result in up to a 0.75 foot stage increase.

By Ceil Strauss,

MNDNR, State Floodplain Manager

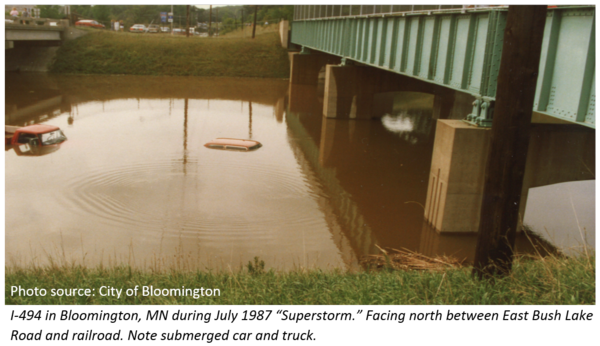

While on a telephone call with a reporter recently, I mentioned the July 1987 Twin Cities "Superstorm," and asked the reporter if she'd been in the Twin Cities at that time. She paused, and replied "I wasn't born yet in 1987." That prompted me to realize it's been 30 years! Many of our local officials and other professionals working with floodplain management are either too young to know about the "superstorm," or were not in the area at that time.

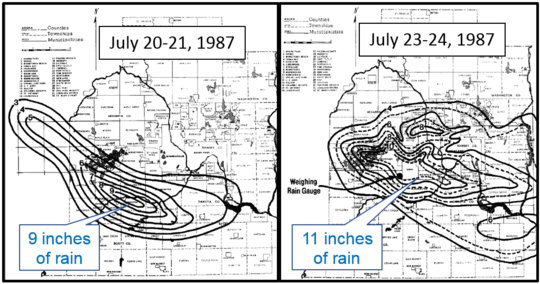

First the July 20-21, 1987 storm hit southern Hennepin and northern Dakota and Scott Counties, with more than 140 square miles getting over 6 inches of rain. The greatest amount reported was over 9 inches at Canterbury Downs in Shakopee.

Then, only a day later, an even bigger storm hit. That storm was centered just to the north, overlapping with much of the same area. The July 23-24, 1987 storm hit over 93 square miles with more than 10 inches of rain and over 574 square miles with more than 6 inches of rain. The map below shows the location of a weighing rain gage that measured 11.32 inches. Some areas had over 16 inches of rain between the two storms.

Two major storms were back to back in the western Twin Cities July 20-21, 1987 and July 23-24, 1987. Source: MNDNR Climatology Office.

Impacts of "Superstorm"

The Twin Cities "Superstorm" impacted

major transportation arteries, affecting many businesses and homeowners.

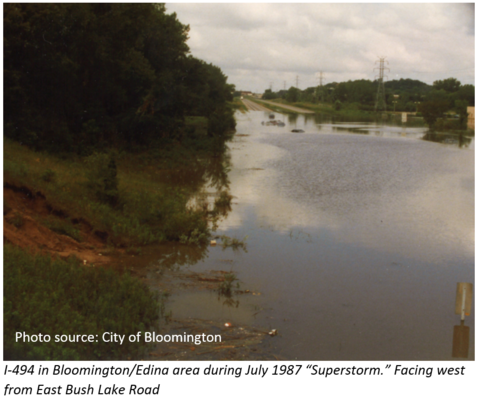

It's hard for those who were not in the area at the time to understand the magnitude of this flood. Portions of I-494 in

the Bloomington and Edina area - not very far from the current Mall of America complex - were closed due to flooding for

nearly a week.

|

At

the time of the MNDNR State Climatology Office storm prepared their summary in July 1987, over

7,000 homes had reported water damage at a cost of over $25 million.

Just over $1.2 million was paid in flood insurance claims.

Resulted in Action

The "Superstorm" triggered a discussion at both the state and local levels about the need to reduce the impacts - and accompanying costs - of future floods.

- 1987 - The Flood

Damage Reduction Grant Assistance Program was created by the Minnesota

Legislature in 1987 to provide technical and financial assistance to local

government units for reducing the damaging effects of floods. The state

provides grants to local units of government for up to 50 percent of the total

cost of a project. The state of Minnesota has provided over provided over $500

Million in cost share grants since 1988.

- 1988 – Cities of Bloomington and Apple Valley adopted Stormwater

Utilities. Note: Nearly 200 Minnesota

municipalities now have stormwater utilities, but the first was adopted by the

City of Roseville in 1984. The utilities typically provide funds for

maintenance of stormwater systems, but many municipalities target at least a

portion of the funds for projects to reduce flood damage potential.

Moody's recently published the report "Environmental Risks -- Evaluating the impact of

climate change on US state and local issuers."

An

announcement on Moody's website notes that the effects of climate change, including

climbing global temperatures, and rising sea levels, are forecast to have an increasing

negative impact on credit ratings. The announcement states, “Moody's analysts

weigh the impact of climate risks with states and municipalities' preparedness

and planning for these changes when we are analyzing credit ratings. Analysts

for municipal issuers with higher exposure to climate risks will also focus on

current and future mitigation steps and how these steps will impact the

issuer's overall profile when assigning ratings.”

The report is available to

Moody’s subscribers.

By Ceil Strauss,

MNDNR, State Floodplain Manager

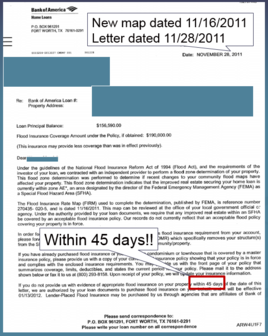

As new FEMA Flood Insurance Rate Maps become effective, many

landowners are receiving letters from their lenders telling them they must

purchase flood insurance. If they do not purchase flood insurance within 45

days, the lender will “force place” flood insurance that is typically much more

expensive.

Local officials can first help citizens verify whether the

mandatory flood insurance requirement really applies. (See the “Zoning

Challenge - How Can I Be in the Floodplain?” article in this Water Talk issue.)

If a structure IS "in" the Special Flood Hazard Area (or the

high flood risk area) on the new map, they MAY be eligible for the greatly

discounted “Newly Mapped Rates.” However, it recently came to the

attention of Minnesota’s Floodplain Program staff that there are scenarios we

thought would be eligible for “Newly Mapped Rates,” but realized they are not when you look at the details for for "Newly Mapped Rates" eligibility.

There are three main possible scenarios for properties in mapped floodplain

on new maps:

|

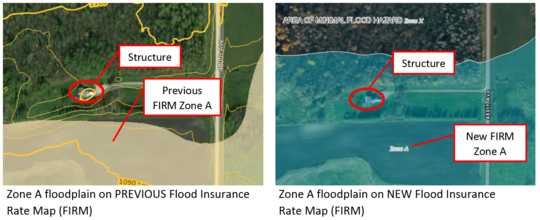

(1)

Eligible for “Newly Mapped Rates”

If there was

a previous Flood Insurance Rate Map (FIRM), and a new FIRM becomes effective, properties

previously in Zones B, C, X, D, AR, or A99 that have been newly mapped into a

Special Flood Hazard Area (SFHA) are eligible for the discounted “Newly Mapped

Rates.” So properties newly mapped in Zone A or Zone AE can essentially pay the

same rates as properties in low and medium risk areas for the first year IF

they purchase the policy within the first year the new map is effective. The rates

will go up annually, but at a percent relative to the much lower initial “Newly

Mapped Rate.”

See example below of a structure that was "out" on the previous FIRM, but "in" on the new FIRM.

|

Example of property that would be eligible for the "Newly Mapped Rate"

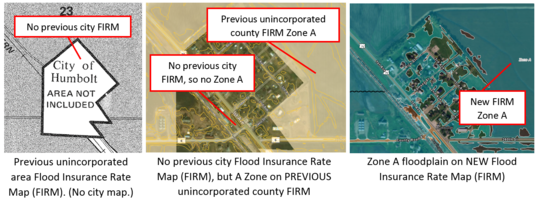

(2) Newly Mapped, but First Flood Insurance Rate Map

If the new map is the first FEMA Flood Insurance Rate Map, the newly mapped

property is not eligible for the “Newly Mapped Rate.” This includes cities that

had never had a floodplain map, and communities that have only had the older

Flood Hazard Boundary Maps. Properties in the newly identified high flood risk

areas would be considered “pre-FIRM,” or pre – Flood Insurance Rate Map (FIRM).

Pre-FIRM structures can use either the

subsidized “pre-FIRM” flood insurance rates, or the rates based on actual

elevations, whichever is cheaper. In order to determine the elevation based

rates, the agent must have a FEMA elevation certificate completed by a licensed

surveyor or professional engineer.

Example of newly mapped areas within old boundary of a city with no previous Flood Insurance Rate Map (FIRM)

(3)

Old Maps Actually Showed Higher Risk

They were

in the high flood risk area on the old maps, but didn’t know it. If the previous map was from the 1970s,

1980s, or 1990s, they were often difficult to interpret. The old paper maps had

few streets for reference, didn’t have an aerial background, and could be at a

scale of one inch = 2,000 feet. With the newer digital maps, it’s much easier

to see whether structures are in the high flood risk area.

The applicable rates depend on whether the

building was built before or after the first Flood Insurance Rate Map. All

properties can be rated based on actual elevations (using the FEMA Elevation

Certificate), and pre-FIRM buildings can also be rated using the “pre-FIRM”

rates.

The National Flood Insurance Program (NFIP) was originally set to expire September 30, 2017, but was extended to December 8, 2017.

Before expiring on December 8th, there was a short extension to December 22, 2017, and just before that deadline there was another extension to January 19, 2018 .

See links to the latest updates and more information about NFIP reform and other topics of

interest to floodplain managers at the Association

of State Floodplain Managers (ASFPM) site.

Adapted from Article by Steve Samuelson, State of Kansas Floodplain Manager

|

There are television shows about tiny houses and the idea is growing in

popularity. Here in Minnesota, we most commonly see them in the form of

vacation homes and guest quarters. There have been a number of questions raised

about the applicable provisions in floodplain and shoreland areas. Ignoring any

other building codes or zoning issues and just considering floodplain and

shoreland regulations, here are some things to consider.

|

|

|

A tiny house is still a house. No matter if the square footage is 300

feet or 3,000 feet, or whether it’s a converted shed or new construction. If it

is habitable in any way, it IS a residential structure.

Every set of floodplain regulations has very clear requirements that the

lowest floor be elevated to or above the regulatory flood protection elevation

and must be anchored to prevent flotation, collapse or lateral movement. It has

to be attached to a permanent foundation.

The argument has come back that the tiny house was delivered on back of

a truck, so it is just temporary. Temporary living quarters are only allowed

for structures that qualify as a recreational vehicle. Coincidentally, many tiny

houses are built on trailers. To be treated as a recreational vehicle, the

structure must be fully licensed and ready for highway use, and meet the

definition found in most floodplain management ordinances:

- Is the tiny house built on a single chassis, 400

square feet or less when measured at the largest horizontal projections,

-

Is it designed to be self-propelled or permanently

able to be towed by a light duty truck, and

-

Is it designed primarily not for use as a permanent

dwelling, but as a temporary living quarters for recreational, camping, travel

or seasonal use?

Any tiny house that can meet that definition could be considered to be a

“recreational vehicle” and allowed to meet the recreational vehicle

requirements for floodplain management.

There has also been some confusion about tiny houses being

called “accessory structures” because they were placed on a property that

already had a larger primary structure. There’ve been cases of someone who

purchased a shed from a lumberyard, had it delivered and then moved into it and

turned it in to a house. To be very clear about this, when people will be

living and sleeping in the structure, then it IS a residence and shouldn’t be

considered a shed or accessory structure.

In Minnesota, even if the tiny structure meets the floodplain standards outlined

above, it is still subject to shoreland standards, if located in a shoreland

district. If so, it must comply with lot area and width requirements and water

and bluff setback requirements. The shoreland rules allow secondary dwelling

units, or “guest cottages” as long as they are on lots that meet the minimum lot

size standards for duplexes. Guest cottages are a type of “tiny house” and are

defined as a structure that is 700 square feet or less and no higher than 15

feet in height. Setbacks and lot size provisions for residential structures

would vary based on the classification of the water body, and should be

verified in the local ordinance.

The tiny house must meet all of the same requirements of any

other larger house. A house is a house and the size does not matter.

Editor's note: The original article was in the October 2017 issue of Kansas Floodplain Tips, and reprinted in the Association of State Floodplain Managers News & Views

|