As the winter holidays approach, please bear in mind that ORS does not change calendar dates when a pay period falls on a holiday or weekend.

Employees may be paid ahead of the holiday or weekend date, but for your report header, you must use the holiday or weekend date as reflected on your payroll calendar.

If you pay employees on a day other than your pay period end date, adjust your record end date accordingly, while keeping the same report end date.

For example: If your pay period end date falls on January 1, 20xx, but you pay your employees on December 30, 20xx, your report header will have a pay period end date of January 1, 20xx, while records within the report will have an end date of December 30, 20xx.

This is especially important for IRS limits associated with DC/PHF contributions on a DTL4 record. Be advised that records will flag because they do not match your payroll calendar, and if the record posts the employee may receive inaccurate service credit.

Please refer to section 7.00.01 of the Reporting Instruction Manual (RIM).

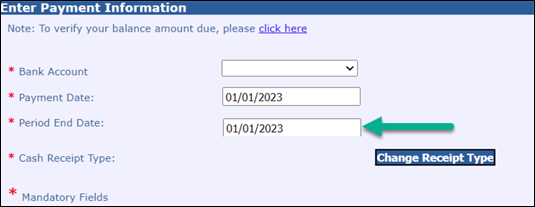

On Jan. 1, 2023, dates from 2022 will no longer be available on the Period End Date drop-down menu on your Enter Payment Information screen.

After Jan. 1, when you’re making a payment, you will see only 2023 dates. If you need to make a payment for a 2022 report, please select the earliest date available on your drop-down menu.

In the November 2022 employer newsletter, it was announced that the 147c(2) MPSERS One Time Deposit payments and invoices would be postponed.

This postponement will continue in December. MDE and ORS will continue to provide additional information to districts on accounting and timing of these funds as it becomes available. Please note: 147c(1) UAAL Rate Stabilization dollars will still be included in districts’ State School Aid payments and invoiced at ORS as normal.

|

Effective Jan. 1, 2023, the interest rate charged on late payments will be 18.78%.

The rate of interest charged on any late contribution payment is determined by the actuarial rate of return from the prior year’s investments, less 2%; however, the rate cannot be less than 6%. The most recent calculated actuarial rate of return was 20.78%.

Delinquent payments of any amount are a serious matter. ORS Employer Reporting closely monitors reporting units in shortfall. Reporting units that repeatedly miss payments or make incomplete payments are at risk for increasing penalties. Check the statement balance due each pay cycle, then make payments in full and on time to avoid a daily (including weekends and holidays) assessment of interest on the delinquent balance.

For the legal requirements regarding late fees and interest, see Public Act 300 of 1980, specifically MCL 38.1342(7).

The Reporting Instruction Manual (RIM), section 8.02.02: Late payment fees and interest charges offers further information on this topic. If you have more questions, contact us at ORS_Web_Reporting@michigan.gov.

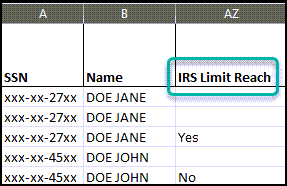

The Internal Revenue Service (IRS) determines limits to how much employees can contribute to a plan each calendar year. You can find limits for 2023 here.

ORS calculates up to the yearly IRS contribution limit using the employee contributions reported to ORS only. Once the IRS limit has been hit, column AZ on the download detail will indicate “YES”. ORS will only charge for the 4% mandatory employer DC contribution rate after the IRS limit has been hit.

|

If your reporting unit offers a deferred compensation plan outside the State of Michigan 401(k) and 457 Plans, your employee and reporting unit are responsible for monitoring the IRS limits made collectively to all 457 plans you offer.

You may save work for your reporting unit by monitoring amounts contributed to plans you offer. Any amount the employer withheld over the IRS limit needs to be refunded to the employee.

Small Steps campaign mailers were sent earlier this month. Eligible participant savings rates will be increased by 1% each year until they are saving 15% of their wages. Participants can opt out if they do not want their rate to be increased.

|

|