Use the contribution rate table with the effective date of Oct. 1, 2020 for DTL2 records with a report end date on or after 10/01/2020.

You’ll find the contribution rate tables for FY 2020-21 (published in March 2020) on the Employer Information website under Reporting Resources, Contribution Rates. Be sure to use the correct table, depending on the type of reporting unit:

For a description of each of the elements of the contribution rates, please see Employer Contribution Rates: Terms, Definitions and Descriptions, found on the Contribution Rates page as well.

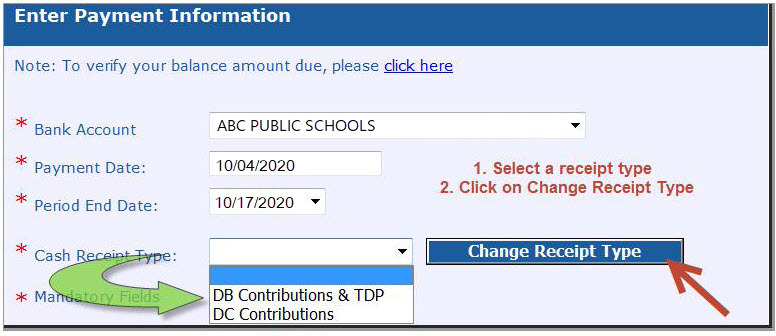

Payment processors: please pay attention to the “cash receipt type” (DB Contributions & TDP or DC Contributions) when making payments.

Correction requests increased in 2019 and 2020, leading to a change in the ORS policy to allow a once-per-year waiver of fees for accidental errors. Beginning in October, fee and interest reversals will no longer be granted for payments that are paid using the incorrect Cash Receipt Type (DC payments made to DB or vice versa). Please make sure the UAAL rate stabilization payment is paid under your DB Contributions & TDP statement.

|

See Reporting Instruction Manual (RIM) section 8.03.01.02: Make a Payment for further clarification.

It is the reporting unit’s responsibility to make sure that payments are made timely and correctly. It is the responsibility of the Office of Retirement Services to administer Public Act 300 of 1980 (38.1342), assigning and collecting fees for contributions not paid according to the schedule, and in the manner determined by ORS.

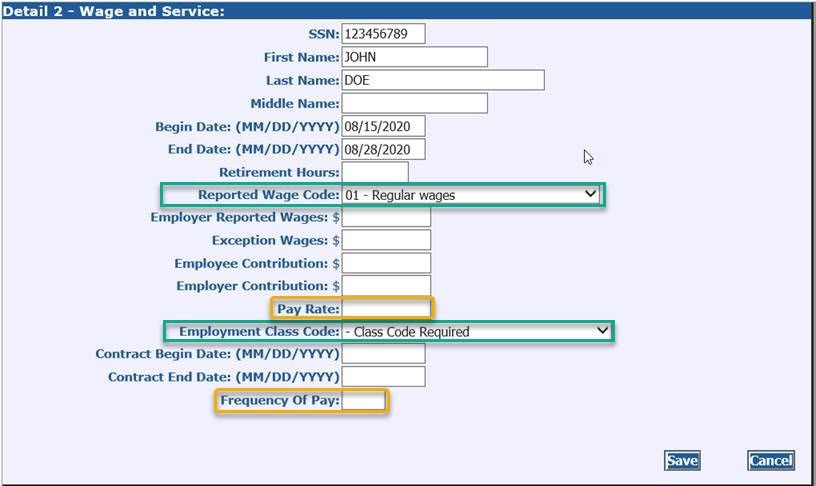

Using the correct information on the DTL2 record is important when reporting your employees because this information can make a big difference when the employee retires. To avoid adjustments in the future, be sure you are using the correct employment class and wage code. Refer to RIM sections 7.12.00: Using Employment Class Codes 13.01: Detail 2 Employment Class Codes and Definitions and 13.03: Detail 2 Wage Codes for information about these codes.

The pay rate and the pay frequency must also be correct on the DTL2 record. When reporting regular wages, the pay frequency must be the number of pays that the employee will be paid for their normal salary (ex. 20, 24, 26, 27, etc). The pay rate field should have either the hourly rate or the annual salary amount based on the employee’s contract.

According to Executive Order 2020-65 (COVID-19) and Executive Order 2020-142 (COVID-19) (June 30, 2020), the following provision is currently scheduled to extend through September 30, 2020:

Mandatory closure of schools relating to COVID-19 shall not affect an employer contribution, employee contribution, or the accrual of service credit under the Public School Employees Retirement Act of 1979, 1980 PA 300, as amended, MCL 38.1301 to 38.1467.

When employees are working a partial schedule at the same position due to COVID-19, please report full contracted wages and hours through September 30, 2020, as specified in EO 2020-142. Please watch for further communications from the state of Michigan regarding any change of this date.

For employees who are unable to perform their regular duties due to COVID-19 and are repurposed to alternate duties, please do not report more than their contracted hours and wages. Please follow these examples:

Full-time employee:

| Wages |

Hours |

|

| $200 |

16 |

Repurposed to clerical (1800-Sub Clerical) |

| $800 |

64 |

Regular position of Aide (1630-Aide) |

| $1,000 |

80 |

Total regular wages and hours under contract or agreement |

Part-time employee:

| Wages |

Hours |

|

| $100 |

8 |

Repurposed to clerical (1800-Sub Clerical) |

| $400 |

32 |

Regular position of Aide (1630-Aide) |

| $500 |

40 |

Total regular wages and hours under contract or agreement |

For any situations other than repurposing, or if you have any questions, please email ORS_Web_Reporting@michigan.gov. Please include as much detail as possible.

Employees who take a leave of absence from work due to Covid-19

Separately, if an employee needs to take time off work due to COVID-19 as stipulated under the U.S. Department of Labor guidelines, Families First Coronavirus Response Act: Employee Paid Leave Rights, we have consulted with the Attorney General’s office and determined that the wages paid for the Expanded FMLA offered April 2, 2020 through December 31, 2020 as a part of the Families First Coronavirus Response Act (FFCRA) are reportable compensation. As a result, these wages and hours should be reported on both a DTL2 and DTL4 record (report it like sick leave). Please report 100% of the hours the employee would have earned if they had been working.

Employees receiving hazard pay

While Executive Order 2020-65 is in effect, extra pay for school employees who are actively working is reportable for both wages and hours. This can be on an hourly basis or as a stipend. It is understood that this is above and beyond the regular pay that all employees are receiving whether they work or not. Going forward, please report these wages using the Supplemental Employment 9510, 9520, or 9530 class codes.

|

|