We’re introducing a new toolkit for your new hires! Please share it with any new employee that’s not already a MPSERS member. You may also wish to provide it to recently hired new employees. Depending on your school’s process for onboarding new employees, you can print and distribute the materials in an orientation or other meeting, or you may simply email the information to your new hires.

These materials replace the New Employee Retirement Plan rack card (R0615C), which is no longer available for order on the Employer Information website (psru).

The material consists of two handouts intended to help new hires understand the retirement plan election: the Retirement Plan Election Guide (ORS mails this to new MPSERS members after you report wages for the person) and a new handout, the Retirement Plan Decision Guide.

The Election Guide summarizes the two plans (Pension Plus 2 and the Defined Contribution plan) and offers comparison in terms of benefits and contributions and qualifying requirements.

The Decision Guide works with the Election Guide, assisting new employees to consider the factors related to this decision, such as their long-term career plans and their tolerance of risk.

Note that there is a lag between when employees are hired and when they can make their election, because ORS cannot work with a member until a DTL1 record has been posted. This may take as long as a few months (for someone hired in June or July but starting in late August) or as short as four weeks after an employee is hired. Even four weeks may be a long wait, and the new employee, busy with their job, may forget to complete their election, thus defaulting into a plan they may not want.

The goal of this new approach is to encourage new employees to make an informed election earlier. Although the legislature gives new employees 75 days to make their election, it’s easier for all involved when members make their election sooner rather than later. Members who receive this information earlier can consider it along with other “new job” issues, even if they must wait a few weeks to make their election on miAccount. Of course, the sooner a member makes the election, the fewer adjustments you’ll have to make.

Because the new materials are electronic documents, you may choose to email all new hires this information. Here’s a sample email you can copy and paste into an email.

|

Welcome! As a new employee at [school or organization name], you have a decision to make about your future! Please review the information in the links below to understand your options and consider what fits you best.

About three to five weeks after the first day you work, you’ll receive a letter from the Michigan Office of Retirement Services (ORS) with information, including an account number, you’ll need to make your election on miAccount. In the meantime, we hope you’ll review the information and consider your future. More detailed information about the two plan options is available at pickmiplan.org.

|

We hope this new approach will help us meet the goal of improving the rate of plan elections (rather than defaulting), and we continue to investigate other options to ease this process for members and reporting units.

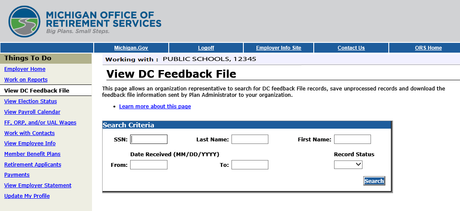

The link to the DC Feedback file is on the Employer Reporting website under the Things To Do menu. The information on the link, provided by both Voya and ORS, relays to you any recent Defined Contribution (DC) and Personal Healthcare Fund contribution changes for your DC employees. The link should be checked on a regular basis, or at least each time you process payroll. Each record on the file contains the employee’s name, their benefit structure, the last four digits of the SSN, the new contribution percentages, the date the change was received, and the report end date when the changes will be effective.

To keep the Feedback File screen up to date and easier to use, once you have updated your employee records with the deduction changes, place a check mark in the Read Record box and click the Save button. The record will drop down to the Read Feedback section of the page leaving only the unchanged records in the Unread section. These Read Records will remain on the screen only until the page is closed when they will be removed. If you need to recall any records at a later time, simply use the Search Criteria section provided on the Feedback File screen.

Tax-sheltered annuity (TSA) investments are an excellent avenue for eligible employees to defer some of their salary and contribute to an additional retirement savings to invest in their retirement future.

Depending on the specific reason for the payment into the TSA, however, the payment may or may not be included in the calculation of an employee’s final average compensation (and therefore reportable).

If the TSA payment is made for compensation that would normally be considered reportable, the TSA payment should be reported. Examples of when TSAs are reportable:

- The TSA is paid for work or services performed.

- The TSA is paid as part of their salary and wages.

- The TSA is paid for longevity or merit pay.

If the TSA payment is made for compensation that would normally be considered not reportable, the TSA payment should not be reported. Examples of when TSAs are not reportable:

- It is paid in lieu of health insurance premiums.

- It is paid in lieu of life insurance premiums.

- It is paid in lieu of other fringe benefits.

It is vital that you report all TSAs properly so employee pensions are accurately calculated. When you report TSAs incorrectly or not at all, you are probably creating future reporting adjustments that could have been avoided.

For more information on reporting TSAs, please review RIM section 4.04.02: Tax-Sheltered Annuity Investments and section 4.04.03: Employee Tax-Sheltered Annuity or Deferred Compensation Investments.

|

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Duis tempus arcu eget sem hendrerit, sed ullamcorper sem ultrices. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Interdum et malesuada fames ac ante ipsum primis in faucibus. Cras tellus nibh, condimentum ut porta tempor, facilisis in eros. Aenean rutrum tortor a ipsum porttitor, a facilisis urna suscipit. Aliquam ac purus orci. Praesent ac neque vitae diam ultricies pretium.

|

Defined Benefit account interest

Interest has been posted to all active Michigan Public School Employees Retirement System (MPSERS) member accounts on July 1, 2019. This is the first year that Pension Plus 2 members received interest on their accounts.The interest rates posted this year are as follows.

- Basic and Member Investment Plan (MIP) members: 11.11%.

- Pension Plus members: 11.84%.

- Pension Plus 2 members: 7.02%.

You may refer employees to the full list of the Defined Benefit plan interest rates dating back to July 1, 1988, available on the Members website under Contributions - Defined Benefit Plan Interest Rates.

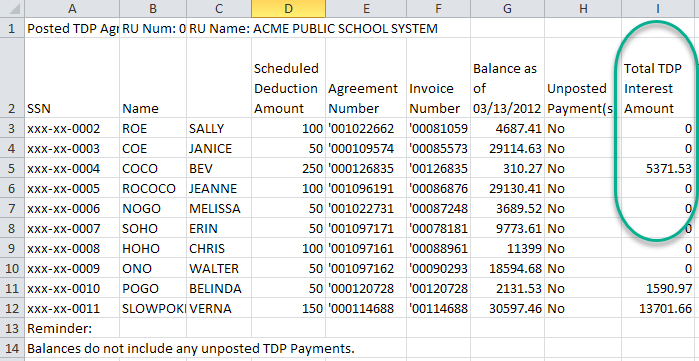

TDP Interest

Tax-Deferred Payment (TDP) agreements that were initiated on or after January 1, 2004, are subject to 8% compound interest, applied annually on July 1 to the unpaid balance. This is included in terms of the completed TDP Agreement Form (R0392C).

As the employer, it's your responsibility to update the employee’s remaining TDP balance with the TDP Interest each year after July 1. The amount appears in the Total TDP Interest Amount column of the TDP Agreement Details spreadsheet.

See RIM sections 10.06: How to Use the TDP Download Detail Link and 10.07: TDP Annual Interest in the Reporting Instruction Manual for more information.

|