Pepco’s distribution rates should be reduced—not increased—from current levels, OPC testimony says

BALTIMORE – Pepco’s proposed 23 percent rate increase should be rejected, and Pepco’s current distribution rates should be reduced, according to Office of People’s Counsel expert testimony filed with the Public Service Commission last week. The decrease would come from eliminating unwarranted spending proposals and a costly change in tax treatment, coupled with reductions in Pepco’s approved level of profit to better reflect market conditions and the low risks of utility investments.

“It is extremely rare for our office in a rate case to oppose any increase to rates,” said Maryland People’s Counsel David S. Lapp. “The evidence typically supports moderate increases due to rising costs and necessary investments, but our review of the facts and the law here demonstrates that Pepco’s requested increase should be fully denied and its profit levels reduced, such that customer rates are reduced from current levels.”

OPC’s experts concluded that Pepco had not presented evidence—as it is required to do—to support its additional revenue needs and, with lower regulated profit levels, that Pepco’s current distribution rates should be reduced by $7.5 million. (More information on Pepco’s request for higher rates is available in OPC’s Consumer Guide to Pepco’s Proposed Rate Increase.)

OPC’s submission included testimony from five expert witnesses. Highlights of the experts’ conclusions include:

- Pepco’s proposed return on equity—essentially its allowed profits—is excessive and does not reflect actual market conditions. (Pepco requests a 10.5 percent return on equity—an increase from its current authorized return of 9.5 percent.) Pepco should instead receive a 7.7 percent return on equity. Pepco’s true market cost of equity may be significantly below 7.7 percent, but that level is a first step toward gradually reducing Pepco’s authorized returns closer to its actual cost of raising equity capital. Contrary to expected arguments from Pepco, lower returns have never been demonstrated to impede utility access to capital.

- Pepco proposes costs for system enhancements beyond those needed to improve system-wide reliability. Pepco already ranks high in terms of reliability nationally and the data supports maintaining—or even reducing—recent spending levels to reduce financial burdens for ratepayers on capital investments that are not cost-effective. As OPC has previously found, those investments are yielding diminishing returns and not improving long-term resilience.

- Like multi-year rate plans, Pepco’s proposed “fully forecasted test year” proposal shifts to customers the risks of inaccurate utility forecasting and overstated forecasts, which means customers pay for utility spending that is higher than necessary. Using forecasts to determine rates also incentivizes utilities to propose more ambitious capital investment plans that overstate their spending needs. Rates should be set under standard methods that allocate risks to the utility which—unlike customers—controls those risks.

- Pepco should not be allowed to increase its rate base (on which it collects profits) by $51.5 million based on a requested tax ruling from the Internal Revenue Service that has not been approved. The IRS guidance Pepco cites is for another company and expressly forbids other parties from relying on that guidance. Pepco’s own request to the IRS may be rejected, and, at minimum, it is premature for customers to pay for it.

-

Pepco’s so-called “Net Economic Benefits Analysis” and its associated testimony is irrelevant to the case, unreliable, and appears to be an attempt to generate additional goodwill for the company’s large spending proposal. Such economic impact studies are not typically considered in evaluating utility proposals to increase rates.

-

Pepco should continue to use seasonal rates in which it charges customers less in the winter months. Although the Commission stated a preference for moving away from seasonal rates in Pepco’s last case, using the same rates for the whole year disproportionately shifts costs from the summer to winter months and reduces the economic benefits of electrifying home heating, which would not be consistent with achieving Maryland’s climate and emissions-reduction goals.

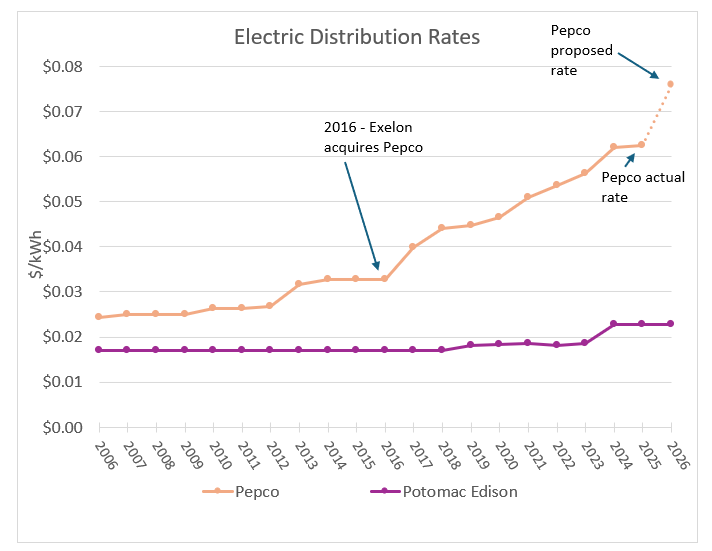

Pepco’s current proposed rate increase follows years of large rate increases for Pepco customers following its acquisition in 2016 by Illinois-based Exelon Corporation. Pepco’s request, if allowed, would mean Pepco’s distribution rates will have risen nine times since 2016, more than doubling its rates (a 132 percent increase). In contrast, Pepco’s neighboring utility, Potomac Edison—the only large for-profit Maryland electric utility not Exelon-owned—has had just two rate increases in about 25 years. Potomac Edison’s rates today are less than one-third (2.3 cents/kWh) of Pepco’s proposed average rate of 7.6 cents/kWh. (See Figure below.)

“Customers are suffering from high energy bills while Pepco presses forward with an unsustainable pace of spending that is driving up rates and profits,” Lapp said. “Further, utility-regulated profit levels far exceed what the markets demand, contributing to high rates and energy bills. It’s time to rein in Pepco’s spending and excessive regulator-approved levels of utility profits.”

The Maryland Office of People’s Counsel is an independent state agency that represents Maryland’s residential consumers of electric, natural gas, telecommunications, private water and certain transportation matters before the Public Service Commission, federal regulatory agencies and the courts.

* * *

|