|

Sarah Rafajko, State National Flood Insurance Program Coordinator

I recently attended a conference at the Federal Emergency Management Agency (FEMA) Region 5, Chicago office and the conference theme was “Urban Flooding.” Urban flooding can be defined as rain falling on impervious surfaces in more densely populated areas, with storm drains unable to contain the flow. As a former local floodplain administrator, I saw urban flooding in my community caused by the increasingly intense rainfall events in recent years. In floodplain management, we are primarily focused on areas within the mapped floodplain but have seen flooding happen in urban areas that depend on storm drains outside the mapped floodplain.

Upon seeing this in my community, even though the floodplain zoning ordinance didn’t regulate those areas, I made it clear to property owners and tenants that property insurance would not cover damages from flooding. I put out a press release and social media posts that property owners and tenants who live on streets frequently plagued by urban flash flooding should consider flood insurance. A local news station interviewed me, and I spoke about flooding outside the mapped floodplain, why it was happening and the recommended steps for affected owners and tenants.

What was aired from that interview was that storm drains were undersized. Flood insurance was never mentioned. In this community, flood insurance was not a popular topic because those who suffered annual groundwater inundation and some of those pumping out basements year-round had their flood insurance claims denied because groundwater flooding doesn’t meet the definition of a flood. For a claim to be paid out for flood insurance, overland flooding must affect two or more structures or two or more acres. These criteria are typically met in the case of urban flooding, so owners and tenants should be aware that flood insurance coverage is available to them.

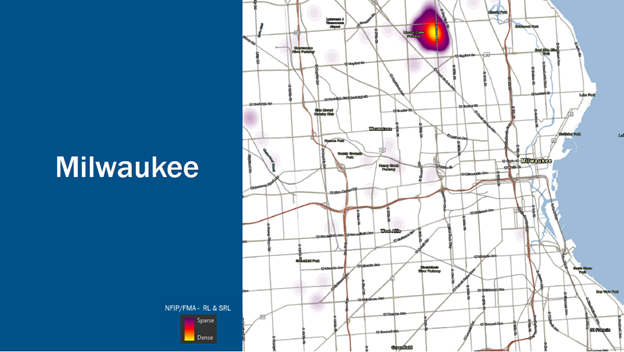

A powerful image depicting the issue of urban flooding was shown at that FEMA floodplain conference. Flood damages are determined based on data pulled from National Flood Insurance Program (NFIP) claims and properties identified as Repetitive Loss (RL) or Severe Repetitive Loss (SRL). Figure 1 is from Milwaukee, showing NFIP claims data for RL and SRL properties. Pretty sparse, right? The graphic shows only one isolated, major area of concern, suggesting that flooding isn’t a significant issue in Milwaukee. One of the points mentioned in the conference was that flood insurance coverage is often low in urbanized areas like downtown Milwaukee, so the RL and SRL claims may not accurately represent urban flood damages and losses.

Figure 1. NFIP/FMA – Repetitive Loss and Severe Repetitive Loss Properties, “Where Are We Flooding?” Presentation by FEMA R6, Charlie Cook & Jeremy Hughes

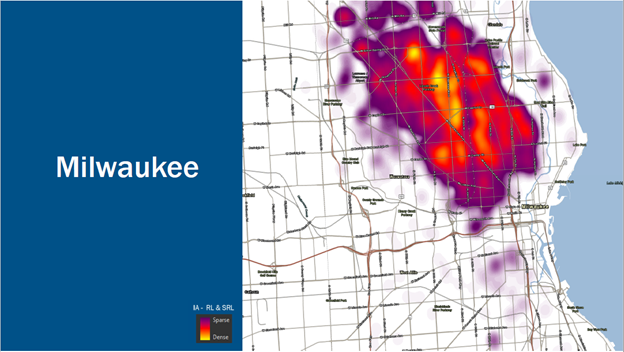

FEMA criteria define High Flood-Risk Properties as those that have two or more NFIP flood losses or two or more Individual Assistance inspections for flood losses. Individual Assistance claims are federal payout claims that FEMA offers to flood victims when there is a federally declared disaster. NFIP RL and SRL data is shared with communities, but the Individual Assistance inspection data is not. When RL and SRL claims are compared to Individual Assistance claims for the same area, we see a clearer picture of flood loss/damage. This same area in Milwaukee, a regional urban flooding hotspot, became the nation's fourth most significant urban flood loss/damage area. Figure 2 shows the Individual Assistance claims that meet the RL and SRL criteria. It’s a much different picture.

Figure 2. NFIP/FMA – Repetitive Loss and Severe Repetitive Loss Properties, “Where Are We Flooding?” Presentation by FEMA R6, Charlie Cook & Jeremy Hughes

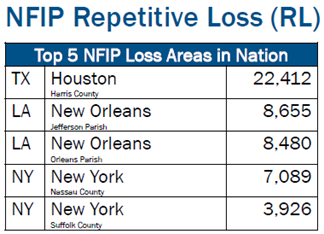

Figure 3a. NFIP Flood losses Top 5, "Where Are We Flooding?" Presentation by FEMA R6, Charlie Cook & Jeremy Hughes

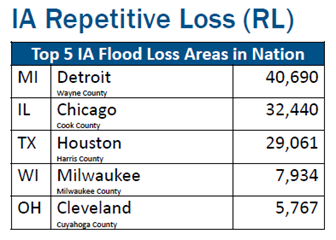

Figure 3b. NFIP/IA Flood losses Top 5, "Where Are We Flooding?" Presentation by FEMA R6, Charlie Cook & Jeremy Hughes

The Top 5 listings in Figure 3 show that Milwaukee is not in the top five for NFIP claims, but once you look at the Individual Assistance claims, we see that Milwaukee is now considered fourth in the nation for flood losses and that four of the five cities in that listing are all located in the Midwest. That’s a massive shift, and the information could be beneficial for future planning and outreach.

As mentioned earlier, urban flooding happens outside the mapped floodplain. Looking at the two heatmaps in Figures 1 and 2, you would expect that there would be some identified floodplains where the flooding hot spots are identified. Let’s look at the Flood Insurance Rate Map. The entire floodplain here is isolated to the stream channel. This means that none of these homes would be required to carry flood insurance and are not subject to floodplain development regulations.

Figure 4. Milwaukee area, FEMA Flood Insurance Rate Maps / Photo Credit: FEMA National Flood Hazard Layer, msc.fema.gov

If property owners in your community are in a similar situation, they may be overlooked when it comes to flood risk communications. We recommend that you include property owners and renters subject to urban flooding but not located in the mapped floodplain in your flood risk and insurance outreach and education efforts. Most individuals are unaware that property and renter’s insurance policies do not protect them from overland flooding. Additionally, individual assistance from FEMA is only available if a federal disaster declaration is made. Often, smaller disasters fall short of hitting the threshold that would make federal Individual Assistance available. In those cases, those without proper insurance may be left with significant damages and no financial means to recover.

I received federal Individual Assistance after a hurricane while living in Florida. I was unaware that flood insurance was available to renters at the time. The federal Individual Assistance helped immensely but significantly fell short of what a flood insurance contents policy would have covered. It did not make me whole after the disaster. The payout amount from a federal disaster is insufficient for an individual to recover to the pre-flood condition. However, a flood insurance policy can get you there.

Since these properties are not in the mapped floodplain, they could be repeatedly damaged by a flood and rebuilt to the same building standards each time, and they could not be structurally protected from flooding. As floodplain managers, we have no regulatory authority over these areas, but these graphics highlight that wherever it rains, it can flood. Suppose there are areas outside of the mapped floodplain within your community that experience regular urban flooding. In that case, we recommend including those areas in future development planning and stormwater and green infrastructure projects.

Data is available if you are interested in evaluating urban flooding claims in your community. To obtain Individual Assistance claims data, you must request it from FEMA and complete an Information Sharing Access Agreement. Contact Sarah Jensen at Sarah.Jensen@fema.dhs.gov to start the process.

|

{kind=link}