Arlington County’s Virginia Insurance Counseling and Assistance Program

(VICAP) provides free, unbiased, one-on-one insurance counseling to Arlington County Medicare Beneficiaries, their families, friends and caregivers.

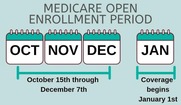

Open Enrollment is Here!

Medicare's Annual Open Enrollment Period began October 15th and ends December 7th. During this time, Medicare beneficiaries can assess or change their Medicare health or drug coverage for 2026. A beneficiary can join, switch, or drop a Medicare Advantage plan or a Medicare drug plan, or switch to Original Medicare during this annual Open Enrollment Period. The changes you make during Open Enrollment are effective January 1 of the next year.

Complete the Intake form below and contact Arlington County VICAP for an appointment.

VICAP Intake Form English

VICAP Intake Form Spanish

|

Negotiated Prices Take Effect for

Ten Drugs in 2026

The Inflation Reduction Act (IRA) of 2022 created the opportunity for Medicare to negotiate prices for the most expensive drugs the program covers. The first set of negotiated drug prices will take effect in 2026 and is estimated to save $1.5 billion in annual out-of-pocket costs for Medicare beneficiaries, while also saving the Medicare program $6 billion per year. Drugs selected for negotiation must be brand-name drugs that don’t have competition and must be among those that drive the most Medicare spending. The negotiated prices are a minimum of 38% off the 2023 list price. All eligible Medicare beneficiaries will have access to these prices, and new drugs will be added to the negotiated list each year.

For 2026 the ten drugs are: Eliquis, Entresto, Farxiga, Jardiance, Stelara, Enbrel, Imbruvica, Januvia, NovoLog, and Xarelto. Click here to learn more.

|

National Diabetes Month

November brings awareness to diabetes and the impact it has on the lives of many. While diabetes is manageable, it can still be serious at any age, especially for older adults who are likely to face more unique complications such as hypoglycemia, heart disease, and kidney failure. Nearly half of all people with type 2 diabetes are aged 65 or older. To learn more about signs and symptoms of diabetes in older adults, click here.

Medicare Part B covers an annual diabetes screening, including a fasting blood glucose test and/or a post-glucose challenge test, if you have certain risk factors. Part B also covers the following diabetic supplies:

- Glucose monitors

- Blood glucose test strips

- Lancet devices and lancets

- Glucose control solutions

Medicare Part D may cover insulin and related medical supplies used to inject insulin (syringes, gauze, and alcohol swabs) if you have a prescription from your doctor. As of January 2023, Part D-covered insulin copays are capped at $35 per month, with no deductible. You should contact your Part D plan for information about its exact costs and coverage rules for insulin. To learn more about diabetes related coverage visit medicare.gov.

The Centers for Disease Control and Prevention (CDC) also offers great tips on effective ways to manage diabetes.

|

Doctor Charged with Telemedicine Scheme

Virginia SMP | October 8, 2025

Dr. Tommie Robinson has been charged and has agreed to plead guilty in connection with a $6 million telemedicine fraud scheme. Charging documents say he worked with telemedicine companies to sign medical documentation, including doctors’ orders, for medically unnecessary durable medical equipment and genetic testing. He never had any contact with the beneficiaries and had no medical relationship with them. Read a Department of Justice press release.

|

Dear VICAP Team,

Are Medicare Advantage Plans less expensive than Original Medicare?

Dear Medicare Beneficiary,

Choosing between Medicare Advantage and Original Medicare isn’t a one-size-fits-all decision—it really comes down to your personal health situation. The expenses associated with Medicare Advantage (MA) plans can vary significantly from those of Original Medicare, and MA plans often include additional guidelines you’ll need to follow. Below is a breakdown of costs in MA and Original Medicare.

Premiums:

Medicare Par B premium: No matter which coverage you choose—Medicare Advantage or Original Medicare—you will be responsible for the Part B premium. If you have limited income and resources, you may be able to get help from your state to pay your premiums and other costs. Click here to learn more.

Plan Premiums: Medicare Advantage Plans may charge an additional premium. If you are enrolled in Original Medicare, you will typically need to pay an additional premium for a Part D plan to cover prescription medications. You can also purchase a Medicare Supplement (Medigap) policy, which comes with its own premium. However, if you have other coverage that coordinates with Medicare—such as retiree health benefits, VA healthcare, or Medicaid—you might not require a Part D or Medigap plan.

Deductible: A deductible is the amount that you must pay for health care services before your insurance starts to cover care. Medicare Advantage plans may include deductibles that vary by plan. Original Medicare has separate deductibles for Part A and Part B, which may be partially or fully covered by Medigap or other insurance.

Copayment / Coinsurance: Copayments and coinsurance are your share of the cost for covered services. Medicare Advantage (MA) plans typically charge a fixed copayment (copay) that varies by plan. With Original Medicare, you usually pay 20% (a coinsurance) of the approved amount for outpatient care. Some MA copays may be higher or lower than Original Medicare’s coinsurance, though certain services must match or be lower. Medigap or other insurance may help cover these costs.

Maximum out-of-pocket (MOOP) limit: Medicare Advantage (MA) plans include an annual cap on out-of-pocket costs, which limits how much you’ll spend on copays, coinsurance, and deductibles. Original Medicare, on the other hand, does not have a maximum out-of-pocket limit.

Other Rules & Restrictions

Out-of-Network Care: Medicare Advantage (MA) plans have varying rules for out-of-network care, including separate out-of-pocket limits. Some don’t cover it at all, while others may charge more. If you go out-of-network, you could pay the full cost. Original Medicare lets you see any provider that accepts Medicare. Also, providers can leave MA networks anytime, but switching plans is only allowed during designated enrollment periods to avoid penalties.

Supplemental Benefits: Some Medicare Advantage plans include extra perks like dental, vision, and hearing care, which can help reduce out-of-pocket costs. However, it's wise to review these benefits closely—coverage may be limited or harder to use than expected, such as dental plans covering only basic cleanings or gym memberships restricted to select locations.

Ultimately, which option is more cost-effective depends on your unique medical needs, lifestyle, and coverage preferences. Click here to view the differences between Medicare Advantage and Original Medicare.

Interested in joining our team? Click here to complete an online volunteer application or contact the Arlington County VICAP team by phone or email:

703-228-1725

MedicareHelp@arlingtonva.us

This project was supported, in part by grant number 90SAPG0064, from the U.S. Administration for Community Living (ACL), Department of Health and Human Services (HHS). Points of view or opinions do not, therefore, necessarily represent official ACL policy

|