|

Dear Colleague,

In today's edition we focus on key global policy priorities for fighting climate change, a new SDR allocation, social unrest, the economic recoveries of Germany, Egypt and Uganda, the resilience of private balance sheets in Europe, and much more. On that note, let's dive right in.

INTERNATIONAL CONFERENCE ON CLIMATE

At the G20 meetings in Italy, Managing Director Kristalina Georgieva laid out three key global policy priorities to tackle climate change and outlined how the IMF is putting climate at the heart of its work.

The three priorities include:

-

Making market signals work for the new climate economy, not against it. As politically challenging as this may be, the world needs to rid itself from all forms of fossil fuel subsidies. Defined broadly to include undercharging for supply and environmental and health costs, they are equivalent to more than 5 trillion dollars annually—and we will soon publish an updated research on the exact composition of these subsidies. By 2030, we need an average global price of $75 per ton of CO2, way up from today’s $3 per ton and up from the 23 percent current emissions coverage.

-

Green investments. Radically decarbonizing our economies will require a substantial scaling-up of investment over the next two decades. The shift to renewables, new electricity networks, energy efficiency, low carbon mobility—offer a huge investment opportunity. And it’s a huge opportunity for growth and jobs. Research by IMF staff shows how deficit-financed green supply policies could raise global GDP by about 2 percent this decade and create millions of new jobs.

-

A “just transition”—within and across countries, ensuring the shift to a low-carbon economy is fair and benefits all. Within countries we must recognize that decarbonization would impact vulnerable households, as well as businesses and workers currently deployed in sectors with high emissions. Fair compensation measures will be required. For example, revenues from carbon pricing schemes can fund cash transfers, social safety nets, worker retraining, and relocation schemes. And place-based policies can help develop new low-carbon industries and jobs through green investments.

Read the full speech here.

📣 In case you missed it, check out a recent blog by Oya Celasun, Florence Jaumotte, and Antonio Spilimbergo about what COVID-19 can teach us about mitigating climate change.

NEW US$650 BILLION SDR ALLOCATION

The IMF Executive Board agreed on a proposal for a new general SDR allocation equivalent to US$650 billion – the largest allocation in the IMF’s history – to address the long-term global needs for reserves during the worst crisis since the Great Depression.

Wondering what an SDR is? Click here.

“I will now present the new SDR allocation proposal to the IMF’s Board of Governors for their consideration and approval. If approved, we expect the SDR allocation to be completed by the end of August,” said MD Georgieva.

“This is a shot in the arm for the world. The SDR allocation will boost the liquidity and reserves of all our member countries, build confidence, and foster the resilience and stability of the global economy. In 2009, an SDR allocation contributed significantly to recovery from the global financial crisis and I am confident that this new allocation will have a similar benefit now. The SDR allocation will help every IMF member country – particularly vulnerable countries – and strengthen their response to the COVID19 crisis.”

Read the full statement here.

COULD RENEWED SOCIAL UNREST HINDER THE RECOVERY?

In a new blog by Metodij Hadzi-Vaskov, Samuel Pienknagura, and Luca Ricci, they write that protests driven by the pandemic’s economic fallout are on the rise, with potentially long-lasting economic consequences.

According to the latest Global Peace Index, the number of riots, general strikes and anti-government demonstrations around the world have increased by a staggering 244 percent in the last decade. Lockdowns and fears of contagion forced a temporary lull. But in virtually every region of the world, demonstrators are making a comeback. Causes range from frustration over governments’ handling of the crisis to mounting inequality and corruption—factors that tend to heighten existing tensions and disparities, and have led to social unrest in the aftermath of previous pandemics.

Using the Reported Social Unrest Index (RSUI)—an index developed by IMF staff based on press coverage—we find that the short to medium-term economic costs of social unrest can in fact be quite large, especially in emerging markets and developing economies (we do not study the potential long-term impacts).

Read the full blog here.

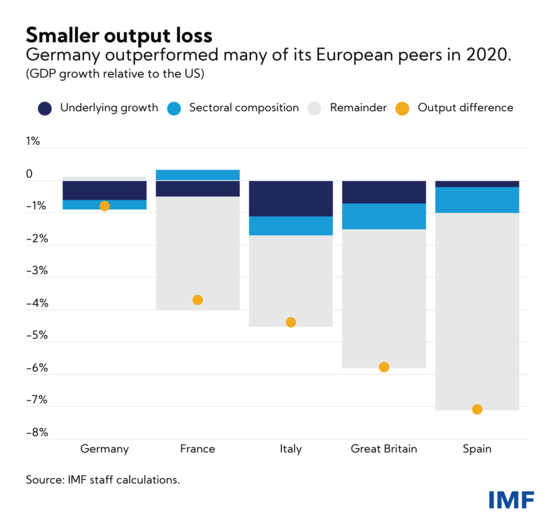

BEYOND THE PANDEMIC: GERMANY'S ECONOMIC RECOVERY PLAN

In a new IMF Country Focus by Carlos Caceres, Mai Chi Dao, and Aiko Mineshima, they showcase five charts that illustrate the effects of the pandemic on Germany and the policies necessary to support a sustained recovery while building better for the future.

A robust recovery is expected in the second half of 2021 as the mass vaccination effort gathers steam, though large uncertainties remain. Germany’s economy contracted by just under 5 percent in 2020, outperforming most European peers. New waves of infections and associated lockdowns during late-2020 to early 2021 hampered the rebound from the first wave. But forward-looking indicators suggest further growth in exports and a brightening outlook for the services sector, in line with re-opening plans and anticipated pent-up demand. For the year as a whole, growth of about 3.6 percent is expected. The recovery path, however, is beset with risks, particularly regarding the progress of the pandemic and supply shortages in key industries.

Interested in learning more? Click here to see all five charts.

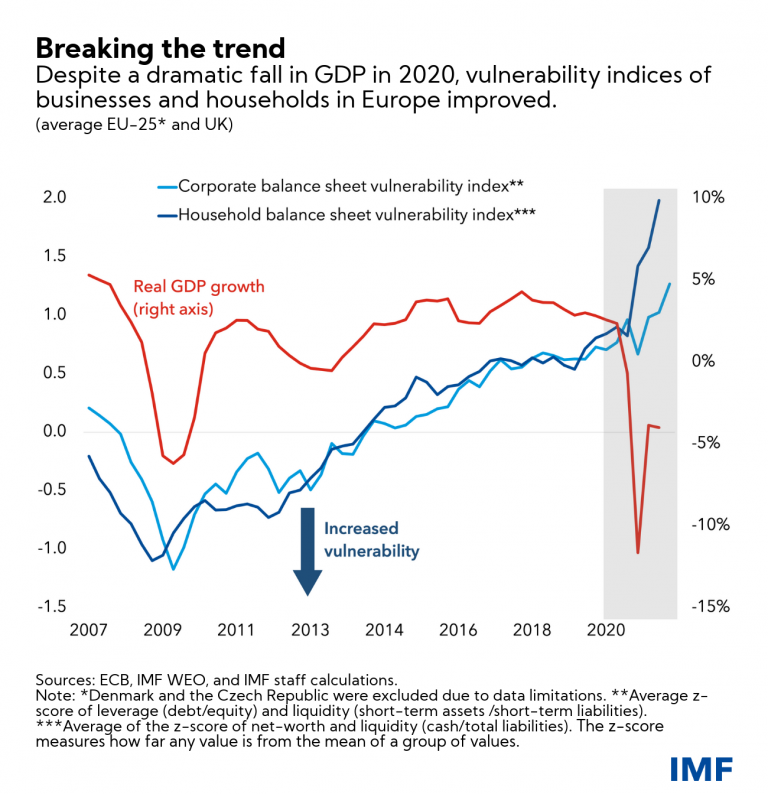

THE RESILIENCE OF PRIVATE BALANCE SHEETS IN EUROPE DURING COVID-19

In a new blog by Estelle Xue Liu, Karim Foda, and Sebastian Weber, they write that one of the positive surprises about last year’s recession is how little damage it inflicted on average household and corporate balance sheets in Europe.

In the past, deep recessions were followed by protracted weakness as they left households and businesses with significantly higher debt and lower income and capital. So far this has not been the case with the COVID-19 crisis, largely thanks to the extraordinary policy response by governments and central banks.

As the recovery takes hold, however, policy makers will need to maintain support for the hardest hit segments of the economy and remain alert for signs of economic damage yet to emerge. Not all private balance sheets were equally resilient.

In new IMF staff research, we observe the resilience of private sector balance sheets. For example, using a simple balance sheet vulnerability index, which combines measures of leverage (or indebtedness) and liquidity, we can see that despite the collapse in GDP in European Union countries and the United Kingdom in 2020, business and household balance sheets in Europe were little affected on average.

Interested in learning more? Read the full blog here.

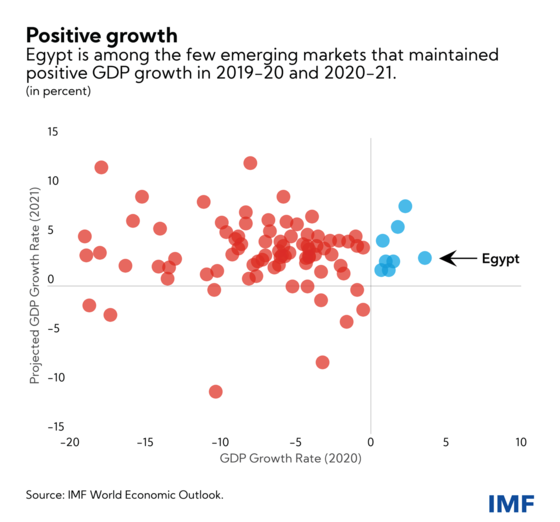

EGYPT: OVERCOMING THE COVID SHOCK AND MAINTAINING GROWTH

Egypt was one of the few emerging market countries that experienced a positive growth rate in 2020. As a result of the government’s swift and prudent policy response, coupled with IMF support, the Egyptian economy showed resilience in the face of the pandemic.

IMF Country Focus spoke to the IMF team for Egypt about the government’s response to the pandemic, the IMF’s role in supporting Egypt, and the challenges and priorities moving forward.

How did the COVID-19 pandemic impact Egypt?

Suchanan Tambunlertchai: Like most emerging markets, the COVID-19 pandemic has been an enormous shock for the Egyptian economy. The fallout was immediately felt through a sudden stop in tourism—which, at the onset of the crisis, accounted for around 12 percent of GDP, 10 percent of employment, and 4 percent of GDP in foreign currency earnings. Precautionary measures to contain the spread of the virus, including partial lockdowns and restrictions on capacity in public spaces, resulted in a temporary decline in domestic activity, while the government’s budget was stretched as the economic slowdown reduced tax revenues.

Egypt also experienced significant capital outflows of more than $15 billion during March-April 2020 as investors pulled out of emerging markets in a flight to safety. Nonetheless, Egypt was one of the few emerging market countries that experienced a positive growth rate in 2020, thanks to the government’s timely response, the short period of lockdown and Egypt’s relatively diversified economy.

What are the top challenges and priorities for Egypt moving forward?

Celine Allard: Over the past 12 months, the authorities’ commitment to prudent policies and their strong performance under the IMF program have helped mitigate the health and social impact of the pandemic while safeguarding economic stability, debt sustainability, and investor confidence. Growth is expected to rebound strongly in FY2021/22 to 5.2 percent, but the outlook is still clouded by uncertainty related to the pandemic, including regarding the full recovery of tourism.

Interested in learning more about Egypt's economic recovery? Click here.

NEW PODCAST: ORAL WILLIAMS ON HOW TECHNICAL ASSISTANCE TRANSLATES INTO BETTER LIVES

Capacity development is one of the IMF's best-kept secrets. Strong institutions are key to a country's long-term development, and a third of the IMF's operating budget goes toward helping governments build the institutional capacity they need to fulfill their development goals. Oral Williams heads the IMF Regional Capacity Development Center for Anglophone West Africa and is coauthor with economists Ralph Chami and Elorm Darkey of a study that shows a direct relationship between technical assistance and the improvement in tax revenues. In this podcast, Williams says providing technical assistance and training to governments means better living standards for more people.

🎙️ Listen to the podcast here. And if you're in a hurry, skim the transcript (PDF).

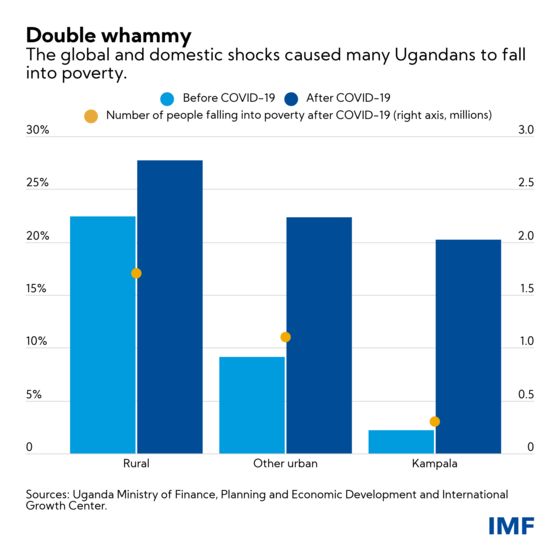

SUPPORTING UGANDA'S RECOVERY FROM THE CRISIS

The IMF has approved a three-year financing arrangement for Uganda under the Extended Credit Facility (ECF), which will generate more inclusive, sustainable growth. This will be achieved through better spending composition and stronger governance.

In a conversation with IMF Country Focus, the IMF Mission Chief for Uganda Amine Mati and Resident Representative Izabela Karpowicz explain that the funding will help Uganda recover from the COVID-19 pandemic and boost income in the medium term.

Uganda, along with much of sub-Saharan Africa, has faced extraordinary challenges since the pandemic hit. Can you explain why IMF financing is necessary now?

Before the pandemic, Uganda’s economy grew, on average, by about 6 percent. However, even then, per capita income growth had started to slow because of high population growth. The global and domestic shocks hit Uganda hard, halving its real GDP growth to only 3 percent in fiscal year 2019/20, and opening sizeable fiscal and external financing gaps.

An earlier disbursement in May 2020, alongside other donor funds, helped support the government’s efforts to mitigate the impact of the pandemic. But they were not sufficient to prevent an increase in poverty, in particular in urban areas. (See chart below.) It is estimated that poverty increased by 7.5 percent nationally by early 2021.

Interested in the full interview? Click here.

F&D: AFRICA'S UNEQUAL PANDEMIC

In sub-Saharan Africa, the gender inequities of the COVID-19 pandemic follow different paths but almost always end up the same: women have suffered disproportionate economic harm from the crisis.

In a new article for F&D, the IMF's Chie Aoyagi dives into why women have fared worse during COVID than men as the rural‑urban divide deepens and income falls across sub-Saharan Africa.

Rural or urban. Educated or uneducated. Formally employed or self-employed. The nuances of how women have fared worse than men in the crisis are becoming clearer with the availability of more high-frequency data. A targeted set of women-centered policies can blunt the negative impact of the crisis and improve prospects for the next generation.

New IMF staff research shows that self-employment among most women could mask the economic impact of the crisis on them. The divide between women in urban and rural settings also makes a difference. Women in cities may be more prone to lose their jobs, whereas women in rural areas are more likely to be self-employed and face greater challenges to keeping their children in school.

Interested in learning more? Read the full piece here.

IMF AROUND THE WORLD

The IMF Executive Board this week concluded Article IV economic assessment consultations with Germany and Timor-Leste. IMF staff completed a virtual mission for the third review of the Extended Credit Facility to São Tomé and Príncipe.

RESPONDING TO THE CRISIS: To date, 86 countries have received more than $110 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note. We would love to hear from you.

Sincerely,

|