|

Dear Colleague,

In today's edition we focus on an assessment of the US economy, the need to act for Africa, the outlook on inflation, inclusive innovation, debt relief for Sudan, and much more. On that note, let's dive right in.

US ECONOMIC RECOVERY

Unprecedented fiscal and monetary support, combined with the receding COVID-19 case numbers, should provide a substantial boost to US economic activity in the coming months, IMF staff concluded in their preliminary findings of an assessment of the US economy.

Strong recovery: US economic growth in 2021 is expected to be around 7 percent, the fastest pace in a generation, with modest risks to the upside. This strong economic performance should continue into 2022, with growth of around 5 percent. These forecasts, however, are based upon an assumption that the American Jobs Plan and American Families Plan will be legislated during the course of 2021 with a size and composition that is similar to that proposed by the administration.

The concluding statement also highlighted the likely transitory nature of inflation in the US. While core inflation (which excludes more volatile food and energy prices) is expected to increase to nearly 4 percent by the end of the year but back down to 2.5 percent by the end of 2022.

The impact of spending measures: The economic impact of the American Jobs Plan (AJP) and American Families Plan (AFP) was a large focus of the IMF’s annual review. The plans envision substantial multi-year investments in infrastructure, research and development, education, childcare, and in-home care. Overall, IMF staff estimate that the AJP and AFP will add a cumulative 5.3 percent to US GDP during 2022-24, as spending ramps up over the next few years. This estimate takes into account how different types of government spending have different fiscal multipliers.

Read the concluding statement here. A new IMF Country Focus article focuses on the effect of new potential US stimulus. Watch a press conference with IMF Managing Director Kristalina Georgieva and Nigel Chalk, the IMF's mission chief to the United States.

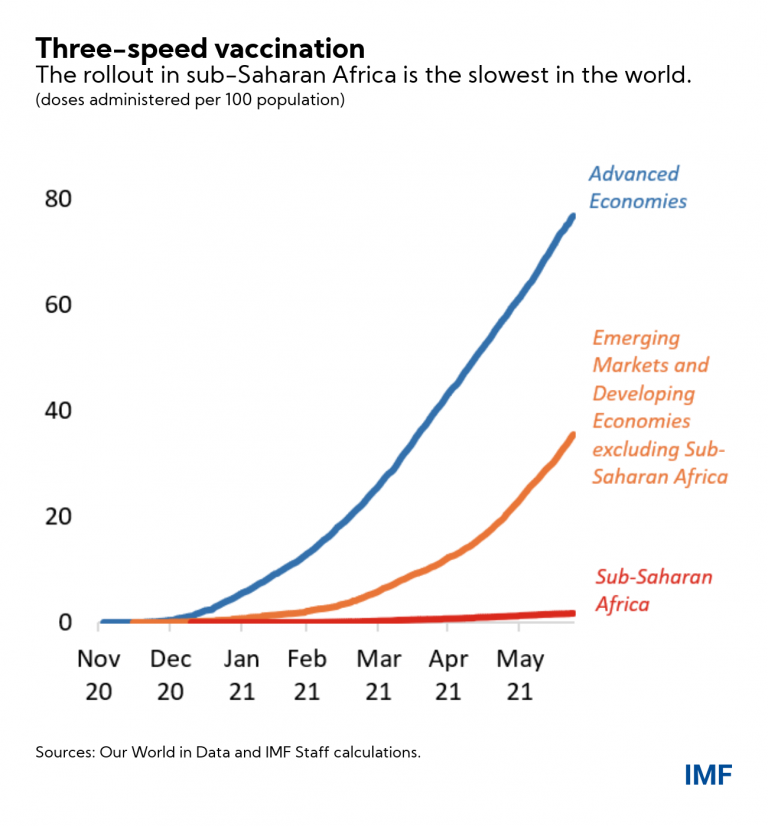

THE NEED TO ACT NOW IN SUB-SAHARAN AFRICA

Sub-Saharan Africa is in the grips of a third wave of COVID-19 infections that threatens to be even more brutal than the two that came before. This is yet more evidence of a dangerous divergence in the global economy. One track for countries with good access to vaccines, where strong recoveries are taking hold. And another for those countries that are still waiting and at risk of falling further behind.

The only way for the region to break free from this vicious pandemic cycle is to swiftly implement a widespread vaccination program, IMF Managing Director Kristalina Georgieva and IMF African Department Director Abebe Aemro Selassie write in a recent blog.

A global public good: Without significant, upfront, international assistance—and without an effective region-wide vaccination effort—the near-term future of sub-Saharan Africa will be one of repeated waves of infection, which will exact an ever-increasing toll on the lives and livelihoods of the region’s most vulnerable, while also paralyzing investment, productivity, and growth. In short, without help the region risks being left further and further behind.

And the longer the pandemic is left to ravage Africa, the more likely it is that ever more dangerous variants of the disease will emerge. Vaccination is not simply an issue of local lives and livelihoods. It is also a global public good. For every country—everywhere—the most durable vaccine effort is one that covers everyone, in every country.

Read the full blog here.

WHERE DO WE GO FROM HERE?

IMF Chief Economist Gita Gopinath once again stressed how important a more equitable vaccine distribution is for a sustained global recovery from the pandemic.

"No. 1 is to recognize that wee need all countries to get to at least 40 percent vaccination rates by the end of this year and 60 percent by the middle of next year," she said in an event with World Bank Chief Economist Carmen Reinhart and European Bank for Reconstruction and Development (EBRD) Chief Economist Beata Javorcik. The discussion took place during the EBRD Annual Meeting and Business Forum.

How do we get there? In the near term, the issue isn't the ability of countries to sign contracts to procure vaccines, it's getting pre-existing supply to countries in need. To reach the 40 percent target by the end of this year, countries that bought surplus vaccines will need to share about 250 million doses by September and an additional 750 million doses by the end of the year. Total surplus among these countries adds up to about 2 billion doses. "This should be very doable," Gopinath said.

What's going to happen to inflation? Supply and demand mismatches, a high number of unfilled jobs yet many still claiming unemployment benefits, a lingering health threat--these are all creating unique conditions during the recovery and feeding inflation.

"There is reason to believe that by next year, these numbers will come back down to more normal levels. But I think the million dollar question is what happens to inflation expectations," Gopinath said, noting that the inflation picture varies by country.

If the transitory shocks of supply and demand mismatches, labor issues and market issues persist, that could influence inflation expectations. "That might then enter into contract negotiations on wages and then on prices, and that's when we enter into a more difficult space," she said.

To hear more on inflation, debt, the role of the state, and other topics, watch the full event here.

📺 Tune in today: IMF Managing Director Kristalina Georgieva will participate in a 9 a.m. ET panel reflecting on the 30th anniversary of the EBRD and what's to come in the next 30 years. Click here to watch the event.

F&D: INCLUSIVE INNOVATOR

In our latest issue, F&D's Peter J. Walker profiles Yale’s Rohini Pande, whose work focuses on how better institutions can make life fairer.

Pande, 49 years old, is “one of the most influential development economists of her generation,” according to the American Economic Association, and has made groundbreaking contributions to political economy, international development, gender economics, anti-corruption, and efforts to combat climate change.

“Running through her work is an insistence not simply to ask what will work to improve the lives of the poor, but why it works, and what this teaches us about how institutions should be structured and how we should view the world,” says Charity Troyer Moore, Yale’s director for South Asia economics research.

In 2019, Pande was named the Henry J. Heinz II Professor of Economics at Yale University and director of the Economic Growth Center. She spent the previous 13 years as a senior professor at the Harvard Kennedy School. There she co-founded Evidence for Policy Design, which works with developing economy governments to address policy problems. Pande won the 2018 Carolyn Shaw Bell Award for furthering the status of women in economics.

Interested in learning more? Read the full profile here.

DEBT RELIEF FOR SUDAN

Sudan became the 38th country to receive debt relief under the enhanced Heavily Indebted Poor Countries (HIPC) Initiative. Reaching the so-called decision point in which Sudan was deemed eligible for the initiative will allow the country's external public debt to be irrevocably reduced—through HIPC debt relief and other debt relief initiatives anchored to the HIPC initiative—by more than $50 billion in net present value terms. If it reaches the HIPC Completion Point in about three years’ time, this represents over 90 percent of Sudan’s total external debt.

The decision by the executive boards of the IMF and World Bank means that Sudan has committed to a strong economic reform agenda and further eliminating poverty.

Read the joint statement from IMF Managing Director Kristalina Georgieva and World Bank President David Malpass, a press release on the decision, and a FAQ on Sudan.

IMF AROUND THE WORLD

The IMF Executive Board this past week completed the second review of Jordan’s program supported by the Extended Fund Facility (EFF), which included a request to increase access to address the impact of the pandemic. The Board also approved a disbursement of $11.6 Million for St. Vincent and the Grenadines to address the fallout from a significant volcanic eruption. The Board approved a 36-month, $1 billion arrangement under the Extended Credit Facility (ECF) for Uganda. The Board approved a 39-month arrangement under the Extended Credit Facility (ECF) for Sudan.

The Executive Board this past week also concluded Article IV consultations with the Dominican Republic, Guinea, Hungary and Mauritius.

RESPONDING TO THE CRISIS: To date, 85 countries have received more than $113 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note. We would love to hear from you.

Sincerely,

|