|

Dear Colleague,

In today's edition we focus on Africa's uncertain recovery, a carbon price floor proposal, facts about food prices, emerging markets in flux, Thailand's economic challenges, and much more. On that note, let's dive right in.

THE ROAD AHEAD FOR AFRICA

Africa is now facing the world's fastest growth rate for new COVID-19 cases, with an exponential trajectory even more alarming than the second wave in January. Based on current trends, this wave will likely surpass previous peaks within the next week. IMF Managing Director Kristalina Georgieva sounded the alarm this week on a worrying trend, which could further delay the region's recovery.

The IMF projects the global economy will grow 6 percent this year, but only half that--3.2 percent--in Africa. In remarks to the African Development Bank's annual meeting, she outlined three policy priorities for getting growth back on track in Africa.

-

End the pandemic everywhere. IMF staff recently proposed a $50 billion plan that could vaccinate 60 percent of the world's population by mid-2022. It would be the best public investment of our lives—and it would be a game changer for Africa.

-

Help Africa deal with a growing debt burden. Public debt in sub-Saharan Africa jumped by more than 6 percentage points to 58 percent of GDP in 2020, the highest level in almost two decades. The G20 Debt Service Suspension Initiative has provided much-need breathing space. Now is the time to make the Common Framework for debt resolution fully operational.

-

Mobilize the international community. IMF membership has supported efforts to scale up financing. That includes a new allocation of Special Drawing Rights (SDRs) of 650 billion. Once approved, it will directly and immediately make about $33 billion available to African members. In addition, we are working towards magnifying the impact of the new allocation—by encouraging voluntary channeling of some of the SDRs and/or budget loans to reach a total global ambition of $100 billion for the poorest and most vulnerable countries.

Read the full remarks here.

A CARBON PRICE FLOOR PROPOSAL

The amount of carbon dioxide and other greenhouse gases being released into the atmosphere must be cut anywhere between a quarter and a half over the next decade if we want to restrict global warming to below 2°C. The fastest and most practical way to achieve this is by creating an international carbon price floor arrangement, the IMF's Vitor Gaspar and Ian Parry write in a recent blog.

A new paper from IMF staff, still under discussion with the IMF Board and membership, proposes the creation of an international carbon price floor arrangement that complements the Paris Agreement and is launched by the largest emitters, anchored on a minimum carbon price, and designed pragmatically.

An illustrative example shows that reinforcing Paris Agreement pledges with a three-tier price floor among just six participants (Canada, China, European Union, India, United Kingdom, United States) with prices of $75, $50, and $25 for advanced, high, and low-income emerging markets, respectively and in addition to current policies, could help achieve a 23 percent reduction in global emissions below baseline by 2030. This is enough to bring emissions in line with keeping global warming below 2°C.

Read the full blog.

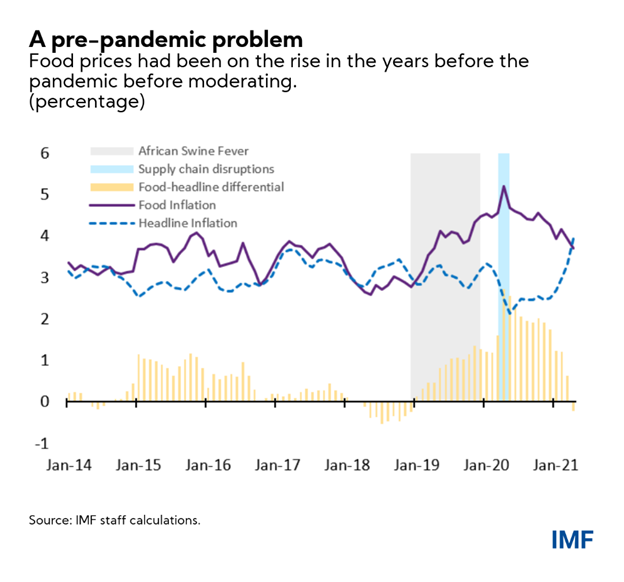

FOUR FACTS ABOUT RISING FOOD PRICES

Rising world food prices for producers are making headlines and causing concerns among the public. The most recent data show a moderation in consumer food price inflation, globally, but that could change in the coming months, the IMF's Christian Bogmans, Andrea Pescatori, and Ervin Prifti write in a new blog.

Four facts:

- Food price inflation started increasing before the pandemic.

- Early lockdown measures and supply chain disruptions induced a spike in consumer food prices.

- Shipping and transport costs are rising and will eventually increase consumer food inflation.

- Global food producer prices have rallied to multi-year highs.

What's the outlook? Based on the four facts presented, it is plausible that consumer food price inflation will pick up again in the remainder of 2021 and 2022. Indeed, the recent sharp increase in international food prices has already slowly started to feed into domestic consumer prices in some regions as retailers, unable to absorb the rising costs, are passing on the increases to consumers. More is likely to come, however, since international food prices are expected to increase by about 25 percent in 2021 from 2020 and stabilizing in 2021.

The impact will vary by country but if producers pass through pass-through 20 percent (13 percent in the first and 7 percent in the second year) of their increased prices it would cause an increase in consumer food price inflation of about 3.2 percentage points and 1.75 percentage points on average in 2021 and 2022, respectively. An additional 1 percentage point to the 2021 global consumer food inflation could be added by the higher freight rates.

Read the full blog.

🎙️ NEW PODCAST: WOOING INVESTORS TO AFRICA'S DEVELOPMENT

With public finances stretched to the limit and the pandemic making things worse by the day, new IMF research looks at innovative ways to get the private sector more involved in financing Africa's development needs. Economist Luc Eyraud led this research. In this podcast, he says while fixing the business environment is a good place to start, sometimes it is simply not enough.

Listen to the podcast here. And if you're in a hurry, skim the transcript (PDF).

F&D: EMERGING MARKETS IN FLUX

In our latest issue of F&D, the IMF's Mahmood Pradhan chats with Richard House (chief investment officer for emerging market debt at Allianz Global Investors) and David Lubin (head of emerging market economics at Citibank) on the outlook for emerging markets.

Emerging market assets have proved remarkably resilient over the past year, confounding more dire expectations at the outbreak of the COVID-19 pandemic. The very large liquidity injections from central banks in advanced economies have undoubtedly helped. But some emerging market economies have also found more policy space, including turning to unconventional monetary policies that many would have thought available only to advanced economies. This crisis will, however, leave scars. Debt burdens of emerging markets and low-income countries are rising to unprecedented levels. Will more countries need financial assistance when the tide of global liquidity turns? And will private investors be willing to share the burden?

Two veteran market players explain why the maturity of this asset class helped limit the fallout and bodes well for its resilience and return to a more normal global liquidity environment. But they do see a need for the private sector to share the burden of adjustment in some countries. They also call for the public sector, including the IMF, to help countries take advantage of the growing demand for debt issuance that complies with environmental, social, and governance standards.

Interested in learning more? Read the full interview here.

THAILAND'S ECONOMIC CHALLENGES

Thailand took decisive action to implement a package of fiscal, monetary, and financial policies to mitigate the impact of the COVID-19 pandemic. Still, the country faces an uncertain path toward recovery. According to the IMF’s latest annual assessment or Article IV consultation, Thailand’s economy is forecast to grow at 2.6 percent in 2021, and a surge in COVID‑19 infections in the country and the region since the beginning of the year highlights the uncertainty about the path of the pandemic and the importance of continued efforts to contain the spread of the virus for a strong and durable recovery.

The IMF's Stella Kaendera and Lamin Leigh break down five things to know about Thailand's economy and COVID-19 in this latest Country Focus.

IMF AROUND THE WORLD

The IMF Executive Board this week completed the first reviews of the 38-month Extended Arrangement under the Extended Fund Facility (EFF) and 38-month arrangement under Extended Credit Facility (ECF) for Kenya. The Board also completed the second and final review of Egypt’s economic reform program supported by a 12-month Stand-By Arrangement and an Article IV economic assessment. The Board concluded Article IV consultations with the Slovak Republic, Switzerland, and Serbia.

RESPONDING TO THE CRISIS: To date, 86 countries have received more than $110 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note. We would love to hear from you.

Sincerely,

|