|

Dear Colleague,

In today's edition we focus on the G7 summit this weekend and how vaccine policy is the most important economic policy moving forward, the benefits of setting a lower limit on corporate taxation, how the pandemic accelerated digitalization and automation, a look behind the metals price rally, the insurance industry and climate change, the future of emerging markets and much more. On that note, let's dive right in.

THE G7 SUMMIT AS THE FAIR SHOT SUMMIT

Vaccinate the world not in 2023, not 2024, but in 2022, so we can bring the pandemic to an end and ensure the recovery is on sound footing. Simply put, I want a [G7] summit that is the Fair Shot Summit: fair shot in the arm, fair shot at the future, said Managing Director Kristalina Georgieva this week at a Health Security Summit hosted by Ian Bremmer of the Eurasia Group.

Georgieva talked about how a two-track pandemic means a two-track recovery, and that would hold the world economy back. If we want to see progress on the economic front, it must be on the back of vaccinations. Vaccine policy is the most important economic policy. If there is strong coordination and additional financing, it is achievable to vaccinate the world to 40 percent by the end of this year, and to 60 percent by mid next year.

The $50 billion investment in this plan will generate $9 trillion in global economic returns by 2025. We hope the G7 would step forward. We hope the G20 will follow in the same spirit. We would like to see as much coordination on the allocation of vaccines as possible. We are also putting together a task force between the World Bank, the World Health Organization, the World Trade Organization and IMF, with the objective to closely monitor how production translates into contracts, how contracts translate into delivery, and to what extent we are matching the needs and the distribution.

Our analysis shows that there are one billion doses that are booked in excess of what is necessary in advanced economies. All advanced economies. Not just the G7. By the end of this year, there can be one billion excess doses redirected to the developing world, said Georgieva.

📺 Watch the discussion here and read the IMF's proposal to end the pandemic.

THE BENEFITS OF SETTING A LOWER LIMIT ON CORPORATE TAXATION

On June 5, 2021, Finance Ministers from the Group of Seven major industrialized nations committed to a global minimum corporate tax rate on multinationals of at least 15 percent. While there are a number of details yet to be hammered out in broader global discussions, this historic agreement heralds an important step forward on the road to international corporate tax reform.

It also highlights the role minimum taxes can play at the global level to help reverse nearly four decades of falling global corporate tax rates and reduce the incentives for large multinational firms to shift profits to low-tax jurisdictions to reduce their worldwide tax liability. In a new study by Aqib Aslam and Maria Coelho, they examine how different types of domestic minimum tax regimes can help countries preserve their corporate tax base and mobilize revenue.

They study the impact of minimum taxes on revenue and economic activity by combining a new country panel database with firm-level data. What they find is that introducing a minimum tax is associated with an increase in the average effective tax rate—that is, the tax rate actually paid by corporations after taking into account tax breaks—of just over 1.5 percentage points with respect to turnover and around 10 percentage points with respect to profits.

Read the full blog here for more.

GETTING BACK TO GROWTH

Producing and consuming more goods and services for the same amount of work sounds too good to be true. In fact, it’s entirely possible. Higher productivity is one of the key ingredients to higher economic growth and incomes. It’s all about how workers become more productive. For many of us, the COVID-19 pandemic has changed the way we work and spend. The question is how these changes will affect our productivity, both now and into the future.

In a new blog about by Lone Engbo Christiansen, Ashique Habib, Margaux MacDonald, and Davide Malacrino, they write that while it’s difficult to forecast long-run productivity, particularly in the current environment, there are two key channels through which the pandemic might influence productivity: accelerated digitalization and a reallocation of workers and capital (e.g. machines and digital technologies) between different firms and industries. Our recent note examines how all this works.

The pandemic accelerated the shift toward digitalization and automation, including through e-commerce and remote-work—and these trends seem unlikely to reverse.

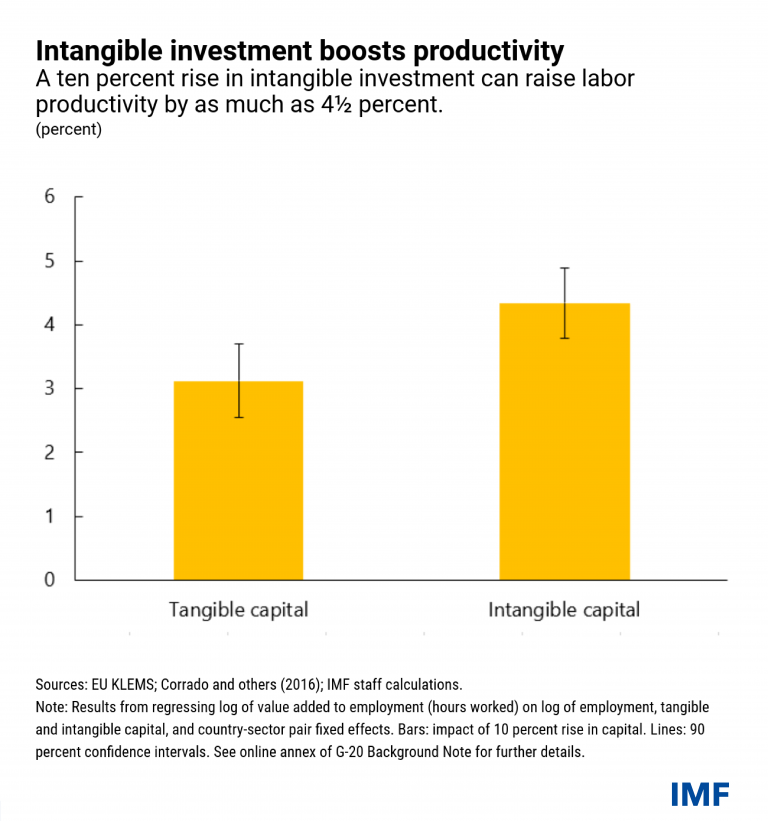

These changes are likely to impact productivity. Recent investments in digital tools—ranging from video conferencing and file sharing applications to drones and data-mining technologies—can make us more efficient at our work. As shown in the chart below, for a sample of 15 countries over 1995–2016, a ten percent rise in intangible capital investment (which is where assets like digital technologies are captured in the national statistics) is associated with about a 4½ percent rise in labor productivity—likely reflecting the role of intangible capital in improving efficiency and competencies.

In comparison, a boost in tangible capital (such as buildings and machinery) is associated with a slightly smaller rise in productivity. As COVID-19 recedes, the firms which invested in intangible assets, such as digital technologies and patents may see higher productivity as a result.

Interested in learning more? Click here to read the full blog.

BEHIND THE METALS PRICE RALLY

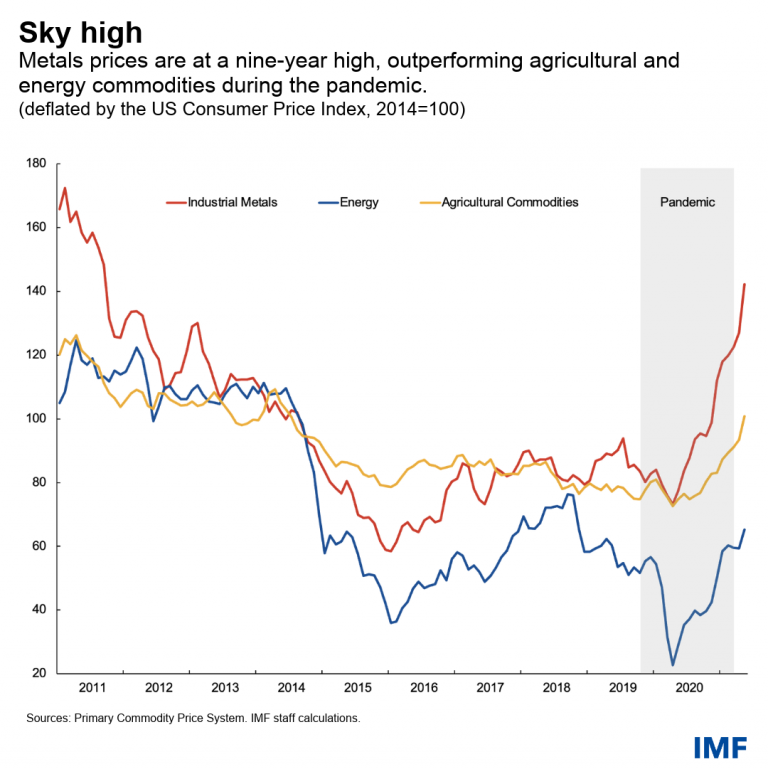

As economies reopen in various parts of the world, the price of some commodities has soared, including the prices of prominent industrial metals. The extent to which the metals price rally may lose steam depends on how multiple factors will play out.

As our latest chart of the week by Martin Stuermer and Nico Valckx shows, metals prices have increased by 72 percent relative to their pre-pandemic levels—reaching a nine-year high in May (in inflation adjusted terms). The increase has been broad-based across industrial metals—copper is up 89 percent in May (year-over-year), iron ore is up 116 percent, and nickel is up 41 percent. The prices of most agricultural and energy commodities are also tracking upward, but at a slower rate. Energy commodities (oil, coal, and natural gas), in particular, sit only a few percentage points above pre-pandemic levels.

Why have metals prices increased much more than other commodities? There are four reasons: a manufacturing-based recovery, supply-side factors, expectations for faster energy transition and infrastructure spending, and storability of metals.

Read the blog to find out more.

THE INSURANCE INDUSTRY AND CLIMATE CHANGE

Earlier this week MD Georgieva participated in the Insurance Development Forum, alongside David Malpass and Mark Carney, and focused her remarks on three aspects.

First, building resilience to climate shocks and accelerating the transition to the new climate economy. Second, identifying and managing climate-related financial risks for the insurance industry itself. And third, unlocking the potential of the insurance industry as a source of financing in this transformation.

On all these issues, the MD said that we rely on the insurance industry’s work on risk assessment, which we are integrating into our own assessments. This includes the IMF's regular country assessments, where we take the pulse of economies, as well as our financial sector assessments, the so-called FSAPs.

How we can integrate insurance sector expertise and products in building resilience is something that the IMF has embraced. We identify best practices and share them across our membership. We support countries in developing and adopting insurance products that are forward leaning. And we work hard to help countries expand insurance coverage—not just at the level of the sovereign, but also for businesses and households.

Click here to read more.

📅 Speaking of climate change, on Wednesday, June 16, at 9:00 AM ET, MD Georgieva will be part of a high-level policy panel on “Natural Disasters and Climate Change: Building Resilience Through Adaptation” as part of a Virtual Conference on Climate-Related Natural Disasters organized by our Research Department. She will be joined by Mia Mottley, Prime Minister of Barbados, and Richard Randriamandrato, Minister of Economy and Finance of Madagascar. It will be live-streamed on IMF.org. Stay tuned.

WOMEN AND WORK: HAS THE PANDEMIC UNDONE PROGRESS?

The pandemic recession has disproportionately affected women, in both developed and developing countries. In advanced economies, women have withdrawn from the labor force in greater numbers, likely hurting their career prospects as well as family incomes. In poorer countries, the costs can include a reversal of progress in halting child marriage and in boosting education for girls.

In this special panel, Carol Atkinson (Senior Advisor RockCreek and Peterson Institute for International Economics Executive Committee member) discusses with Betsey Stevenson (University of Michigan) and Abebe Selassie (IMF Africa Department) how the pandemic has affected women's progress in the workplace in developed and developing countries.

📺 Watch the discussion here.

F&D: MILES TO GO—THE FUTURE OF EMERGING MARKETS

In the cover story for our latest issue of F&D on the road ahead for emerging markets, the IMF's Rupa Duttagupta and Ceyla Pazarbasioglu write that emerging markets must balance overcoming the pandemic, returning to more normal policies, and rebuilding their economies.

As the COVID-19 pandemic enters a second year, concerns are rising about how well emerging markets will fare. So far, they have been agile in responding to the economic fallout from the pandemic with unprecedented rescue packages for their hard-hit sectors and households. After a short-lived period of financial stress in March 2020, most emerging markets were able to return to global financial markets and issue new debt to meet their financing needs. However, in a global recovery in which some countries are rebounding faster than others and uncertainty is high regarding the pandemic, there is likely to be more market volatility. This will test the ability of policymakers in emerging markets to navigate a shifting landscape, manage their policy trade-offs, and achieve a durable recovery.

Read the full cover story here, and check out this 📺 brief video discussing the future of emerging markets.

TREVOR MANUEL: PUTTING PEOPLE FIRST

When the apartheid regime ceded power following South Africa’s first democratic elections in 1994, the economy was in shambles and deeply unequal. Debt service costs as a share of GDP were crippling. Trevor Manuel—a veteran of the anti-apartheid struggle who was appointed minister of finance—made a tough call. He revamped the budgeting process and set a stringent deficit reduction target.

By 2006, the economy was growing at its fastest pace in more than two decades, and the budget deficit was close to zero—outcomes few thought possible. “Part of leadership,” Manuel said, “is that you must not be afraid to take a stand on some issues if you are on solid ground.” It’s a position that has guided him throughout his career. Blunt in his criticism of the “old order,” he put voice and representation of emerging market and developing economies squarely on the international agenda, both as chair of the World Bank’s Development Committee and as head of the Committee on IMF Governance Reform.

His advocacy for a level playing field continues, as special envoy of the African Union for Africa’s COVID-19 response, following 20 years as a Cabinet minister under the first four presidents of democratic South Africa. In a new interview with F&D’s Analisa Bala, Manuel talks about South Africa’s struggles and the resources needed to get ahead of the pandemic in Africa.

Read the interview here and listen to 🎙️ a new podcast with Manuel.

NORWAY, ELECTRIC VEHICLES AND EMISSIONS

In a new IMF Working Paper by Youssouf Camara, Bjart Holtsmark, and Florian Misch, they dive into the world of electric vehicles, tax incentives and emissions in Norway.

Specifically, this paper empirically estimates the effects of electric vehicles (EVs) on passenger car emissions to inform the design of policies that encourage EV purchases in Norway. They use exceptionally rich data on the universe of cars and households from Norway, which has a very high share of EVs, thanks to generous tax incentives and other policies. Their estimates suggest that household-level emission savings from the purchase of additional EVs are limited, resulting in high implicit abatement costs of Norway’s tax incentives relative to emission savings. However, the estimated emission savings are much larger if EVs replace the dirtiest cars. Norway’s experience may also help inform similar policies in other countries as they ramp up their own national climate mitigation strategies.

IMF CLIMATE INNOVATION CHALLENGE

At the IMF, climate change is now at the heart of our work on economic and financial stability, growth, and jobs. Policy innovation is central to helping member countries reduce emissions, build resilience, and capture the opportunities for greener growth.

How might we integrate climate change into economic analysis to promote green policies?

To help answer this question, the IMF is organizing an innovation challenge on the economic and financial stability aspects of climate change. Country authorities/agencies, civil society organizations (including think tanks), and staff from the IMF, World Bank, and international organizations are invited to submit proposals that have the potential to enhance the IMF’s capacity development, policy advice, and operational impact in areas where economic and financial policies intersect with climate change.

Click here to learn more about the process and timeline.

📅 NEXT WEEK: PROMOTING AN INCLUSIVE RECOVERY

Achieving inclusive growth—that is, strong and sustainable economic growth whose benefits are widely shared—is the key policy challenge of our day and thus a fundamental pillar of the IMF’s policy focus in the years ahead. Inequality has been rising in many countries, and large income disparities persist across regions, genders, ethnicities, and generations. The COVID-19 pandemic and economic and financial crises have further exposed these vulnerabilities, while longer-term trends, such as climate change and job-displacing technologies, if left unaddressed, pose serious challenges to inclusive growth.

On Tuesday, June 15th at 12:00 PM ET, following the G7 Leaders Summit, Managing Director Kristalina Georgieva will join Professor Barry Eichengreen from UC Berkeley and UN Under Secretary General and Special Adviser on Africa Cristina Duarte in a high-level panel on these issues—moderated by Martin Sandbu, European Economics Commentator at the Financial Times. Stay tuned here for more.

The event coincides with a new course on inclusive growth for government officials and the broader economic community, and the forthcoming book How to Achieve Inclusive Growth, which is co-edited by Professor Eichengreen and IMF staff members. Over the past several months, the IMF has stepped up its involvement on inclusive growth and published nearly 20 working papers (PDF list) on this topic.

IMF AROUND THE WORLD

The IMF Executive Board this week announced the approval of about $650 million in funding for Senegal under the stand-by arrangement and arrangement under the Standby Credit Facility for and completed the third review under the Policy Coordination Instrument. The Board completed its fifth review of the Extended Fund Facility arrangement for Angola and approved a $772 million disbursement. The Board also completed its first review of the Extended Credit Facility arrangement for Afghanistan and concluded a Financial System Stability Assessment with Hong Kong SAR.

The Board this week announced the conclusion of Article IV economic assessment consultations with Belize, the Kyrgyz Republic, Norway, and Iceland.

IMF staff this week announced that they have reached an agreement with Gabon on a new arrangement under the Extended Fund Facility.

RESPONDING TO THE CRISIS: To date, 86 countries have received more than $110 billion in financial assistance in response to the economic impact of the COVID-19 crisis. Find out more in our lending tracker, which visualizes the latest emergency financial assistance and debt relief to member countries approved by the IMF’s Executive Board.

Overall, the IMF is currently making about $250 billion, a quarter of its $1 trillion lending capacity, available to member countries.

Looking for our Q&A about the IMF's response to COVID-19? Click here. We are also continually producing a special series of notes—about 100 to date—by IMF experts to help members address the economic effects of COVID-19 on a range of topics including fiscal, legal, statistical, tax and more.

HAVE YOUR SAY

Thank you again very much for your interest in the Weekend Read. We really appreciate your time. If you have any questions, comments or feedback of any kind, please do write me a note.

And if you're on LinkedIn, subscribe to this newsletter in a more 📈 visual format.

Sincerely,

|