|

|

- What to Do Before a Flood, website in English and Spanish

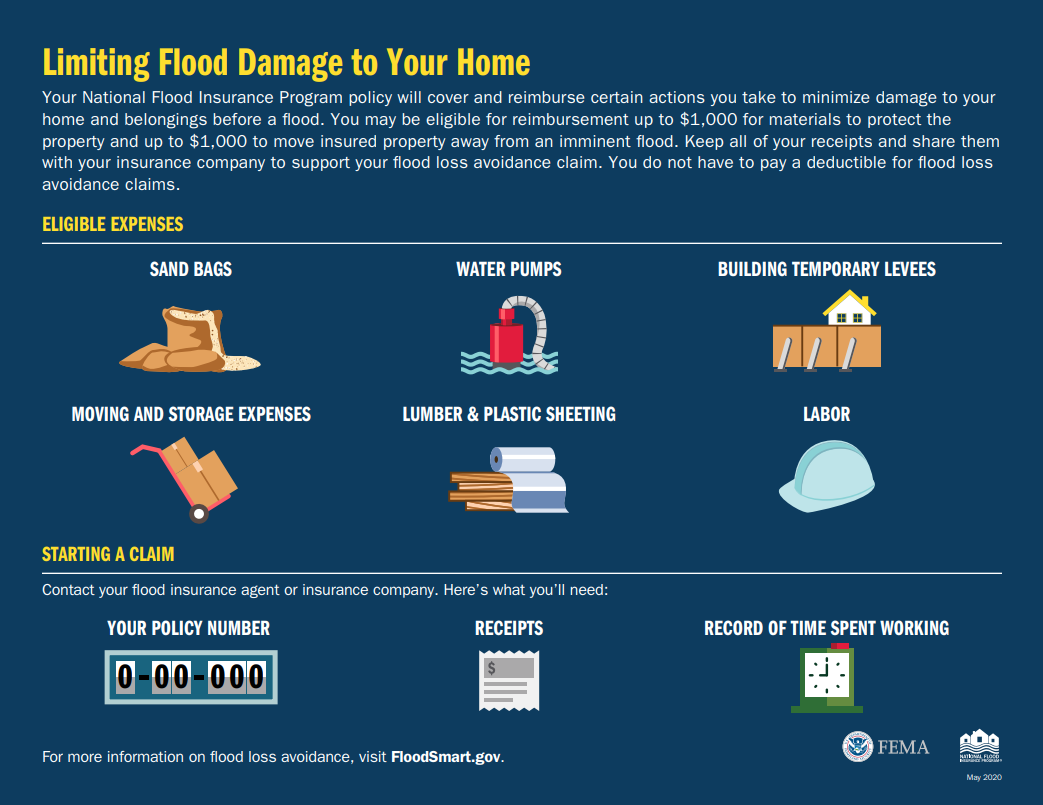

- Flood Loss Avoidance, fact sheet in English and Spanish

- Flood Loss Avoidance, infographic in English and Spanish

- Flood Loss Avoidance, video in English and Spanish

- Securing Documents In Preparation for a Flood, video in English and Spanish

- General flood safety social media from Ready.gov, tool kit in English and Spanish

-

Is it too late to purchase flood insurance? It could be. Generally there is a 30-day waiting period for policies to go into effect and there is a flood in progress exclusion. Check with your insurance agent though, because there are a few exceptions including no waiting period if you purchase flood insurance while making, increasing, extending, or renewing your mortgage loan and a 1-day waiting period if a home or business is newly designated to be in the high-risk flood area and you purchase flood insurance within the 13-month period following a map update. Click here for more information in English and Spanish.

-

What if my NFIP policy just expired? If your NFIP flood insurance policy (including a Group Flood Insurance Policy) just expired, contact your insurance company immediately to renew your policy (or for recently expired GFIP-holders, purchase a Standard Flood Insurance Policy). Claims for losses that occur in a 30-day grace period will be honored, provided that the full renewal premium is paid within 30 days of the policy expiration date. Lapsed policies (expired policies after the grace period) may cause you to lose any discounted rates you have been receiving and you may be subject to a new 30-day waiting period for coverage to go into effect.

|

- Help Your Clients Prepare for Flooding, website

- Understanding Flood Loss Avoidance for Agents, fact sheet

- Flood Insurance Agent Field guide

- Flood Insurance Manual

- Risk Rating 2.0: Equity in Action website

- NFIP Marketing Resource Library with hundreds of assets including social media posts, videos, fact sheets, templated letters to potential customers and other products for you to communicate the value of flood insurance

- Permits for development, including repairs and rebuilding, are required in the Special Flood Hazard Area (Zones A and V). Some communities may choose to waive a permit fee, but you can't waive the permit. Click here for more information.

- Damage of any source (wind, water, fire, debris impact and more) to structures in the Special Flood Hazard Area must be assessed for substantial damage and substantial improvement. Communities can use FEMA's free Substantial Damage Estimator 3.0 Tool to help with the assessments. Click here to view short YouTube videos on substantial damage and using the tool.

- Substantially damaged structures are the most-damaged structures that are also at the most risk of future flood damage. Local floodplain and permitting offices will determine what, if any, rebuilding requirements must be met to bring these structures into compliance with locally adopted ordinances, orders and codes, including the potential need to elevate the structure to or above the community's design flood elevation. View Answers to Questions About Substantially Improved/Substantially Damaged Buildings for more information.

- Determining that a structure is substantially damaged and must meet current, local regulations can help provide access to mitigation dollars, and it helps break the cycle of repeat flood damage. View Increased Cost of Compliance for more information, and consider applying for FEMA Hazard Mitigation Assistance Grants.

- DRRA Section 1206 FEMA Public Assistance Reimbursement: After a federal disaster is declared with the FEMA Public Assistance, permanent work designation for your county or parish, you may be able to seek reimbursement for the work and costs associated with administering and enforcing your floodplain management and building code regulations for the 180 days after declaration date. Reimbursement is subject to a cost share and could include overtime for your permitting staff; straight and overtime for temporary hires; work and costs associated with substantial damage inspections, including the use of a contractor or mutual aid; and more. Click here to view the policy and here to watch a 20-minute video explaining the policy. Begin discussions between departments, including floodplain, building code, emergency management, budget and finance and more to help posture your community to be able to submit for this reimbursement.

|

|

|