|

You received this email as a PERS employer reporting or financial contact. Please contact your PERS account representative or PERS Actuarial Services if you need assistance. Review your GovDelivery subscriptions here.

Senate Bill 1049: Work After Retirement contributions may cause a potential unrecorded liability as of June 30, 2020

This information is only relevant to PERS-participating employers that hire PERS retirees to "Work After Retirement."

From Senate Bill 1049 (2019).

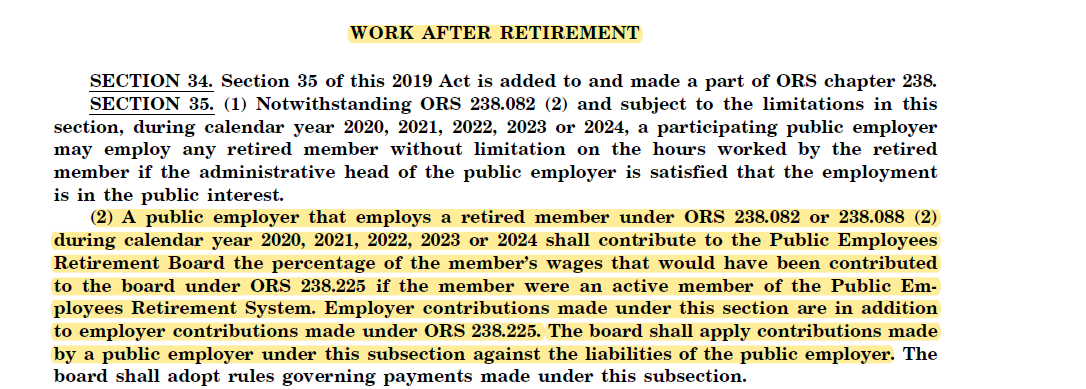

Effective January 1, 2020, the Work After Retirement section of Senate Bill 1049 relaxes most existing restrictions on retirees working after retirement. This allows most retirees to work unlimited hours for a PERS-participating employer, while continuing to receive their retirement benefits (without accruing any new benefits), in calendar years 2020-2024.

The bill also requires employers to pay employer contributions on PERS retirees’ salaries as if they were active members, excluding IAP (6%) contributions.

Potential unrecorded liability: You may want to contact your municipal audit firm

PERS will not be able to invoice employers for Work After Retirement contributions until fall 2020 because of the timeline to launch brand new system functionality. Therefore, your first invoice may include several months of contributions accrued prior to fall 2020.

- Employers who are required to report unrecorded liabilities as of June 30, 2020, should be able to estimate the amount of contributions owed to PERS for retirees employed between January 1, 2020, and June 30, 2020, regardless of whether PERS has invoiced the employer yet.

- Your estimated liability may be calculated by taking the rate components applicable for active members (not including IAP), and multiplying that by your retiree wages paid between January 1, 2020, and June 30, 2020.

- Depending on the basis of accounting you use for financial purposes, you may need to report the amount of estimated employer contributions owed on retired employees' salaries on your fiscal year-end financial statements as a liability.

- You may want to consider contacting your municipal audit firm if you have any questions about correctly reporting a liability for contributions that are owed to PERS but have not yet been invoiced as of the end of the fiscal year.

Learn more: For more information about SB 1049, visit our SB 1049 webpage for employers.

|