|

|

DED Stakeholders,

August’s economic data continues to provide us with mixed signals, however, the Fed may have given us an indicator as to which signals are more important.

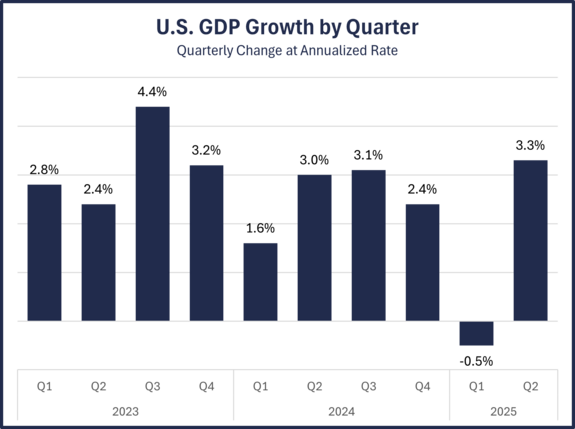

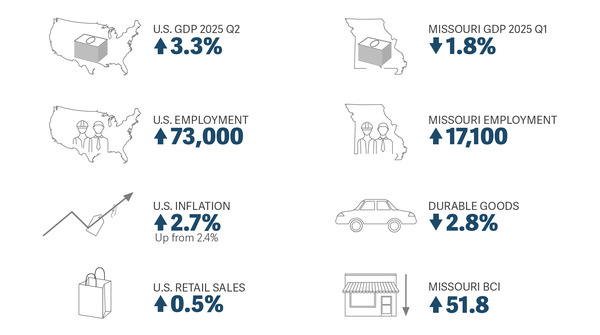

Last month we covered the initial GDP release for the second quarter and the U.S. employment data for July. As a recap, GDP rebounded strongly (at an annualized 3.0% rate) after an import-induced decline in Q1. Revised GDP numbers released last week show that the second quarter’s growth was even better than originally announced (3.3%). However, U.S. employment told another story. Revised data shows that businesses have pulled back considerably on hiring with May, June, and July combining for just 106,000 jobs. Prior to May, the average growth per month was over 122,000.

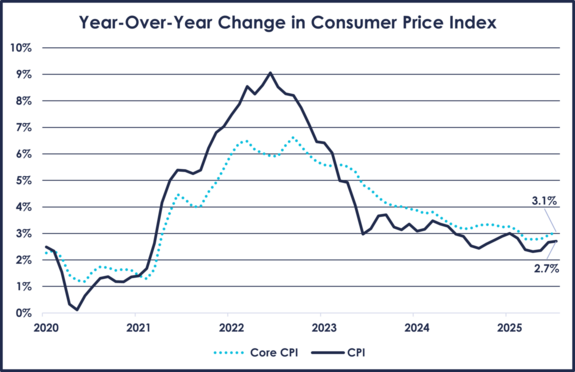

July’s headline inflation number held steady at 2.7%, while core inflation (which removes food and energy prices due to their volatility) rose to 3.1%. This gets us back to those mixed signals. On one hand, there is concern (based largely on the employment data) that the economy might be slowing down. At the same time, inflation remains well above the Fed’s target rate of 2% and has risen in recent months. We often associate rising inflation with an economy that is running “too hot,” so seeing it rise as the economy is showing signs of slowing puts the Fed in a difficult spot. Should they hold interest rates at their elevated level to keep inflation in check (at the risk of slowing the economy further)? Or cut rates to boost the economy while risking higher inflation? Fed Chair Jerome Powell gave us a good indicator that the Fed was more concerned about the slowing economy and was leaning towards rate cuts.

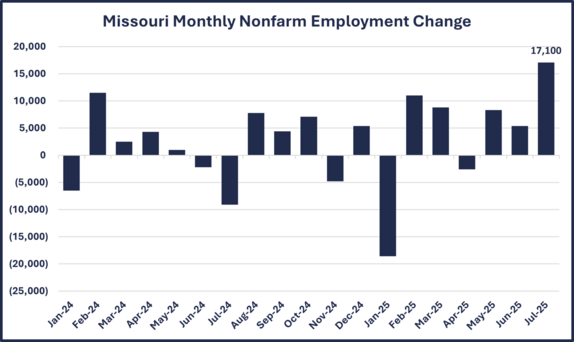

Turning to Missouri, July’s employment numbers were good, adding 17,100, however, it might be best to wait until August’s data release (which would include any revisions to that 17,100 figure) before we celebrate. Much of the growth in July was in the local government sector, which includes public education. Understandably, these numbers can be difficult to assess during the summer as districts start hiring for the new school year.

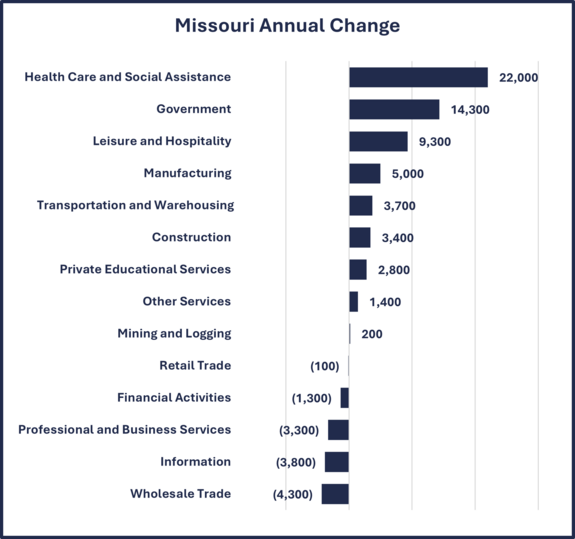

Looking at a longer-term trend, Missouri is posting solid employment growth year-over-year with 49,300 jobs added for the year ending in July, which ranks 10th nationally.

September promises to be a telling month. All eyes will be on Friday’s U.S. employment release for August to see if the recent slowdown in hiring was a blip or the start of a new trend. On the 11th, we will have the latest data on inflation, which will undoubtedly factor in when the Federal Open Market Committee considers interest rate cuts when they meet in the middle of the month. Again, Chair Powell has signaled a cut.

All said, uncertainty continues to cloud the economy. However, it seems at least a bit clearer now that slowing growth is the primary concern.

Sincerely,

Jeff Pinkerton

Director of Economic Research

Sources: Bureau of Economic Analysis, Bureau of Labor Statistics, Census Bureau, Creighton University

|

|

Inflation

Inflation stayed at 2.7% in July compared to last year, a bit lower than expected, with prices up 0.2% from June. Core inflation, which leaves out food and energy, ticked up to 3.1% and rose 0.3% from last month. Big consumer categories like shelter, energy, and groceries mostly leveled off or dipped, but prices for furniture, used cars, and some services kept climbing.

The producer-price index (PPI) rose 0.9% from last month and 3.3% over the last year. As a reminder, CPI tracks prices from the consumer’s perspective, while PPI reflects costs from the producer’s side. The biggest impact on the PPI increase were higher raw agricultural products prices. Both goods (+0.7%) and services (+1.1%) rose in July, with manufacturing equipment up 0.4% and related services jumping 4.5%.

Source: Bureau of Labor Statistics

Retail Sales

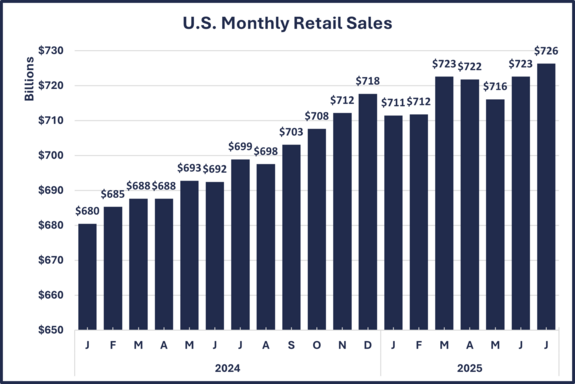

Retail sales rose 0.5% in July, just shy of expectations, marking the second straight month of growth. Excluding autos and gas, sales were up 0.2%. After back-to-back declines in April and May, consumer spending has picked up this summer, with June’s increase revised higher to 0.9% from the initial 0.6%.

Even after factoring in July’s 0.2% rise in consumer prices, retail sales were still up 0.3% in real terms. Home furnishings jumped 1.4%, though this category has also faced stronger inflation recently. E-commerce sales rose 0.8% (coinciding with Amazon’s Prime Day). Spending at restaurants and bars fell 0.4%, suggesting some consumers are pulling back on certain discretionary purchases.

Source: Census Bureau

Business Conditions Index

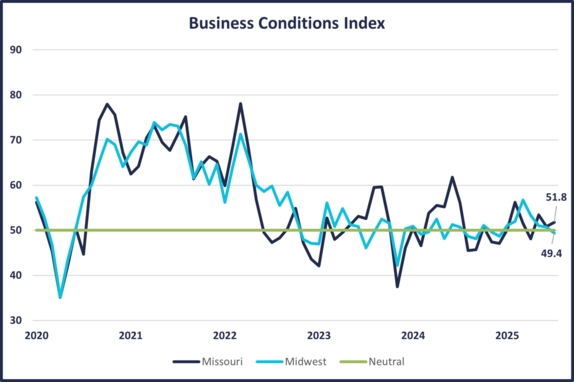

Missouri’s Business Conditions Index (BCI) rose to 51.8 in July, the second highest confidence reading for the region. Aside from a slight dip in June, Missouri has stayed above the growth-neutral threshold (50.0) in six of the past seven months. Meanwhile, the Midwest region fell below growth neutral confidence to 49.4 in July.

The disparity between Missouri businesses and their Midwestern peers appears most evident in the Inventories component. Missouri climbed to 54.4 (+8.4 points) while the Midwest posted a more modest 49.1 (+2.2). However, both Missouri and the region saw sharp declines in New Orders, with confidence dropping 6.8 points and 6.9 points, respectively. Businesses also flagged trade policy shifts as a potential source of inflationary pressure.

Still, only 6.7% of supply managers reported shifting purchases from international to domestic suppliers in response to tariffs.

Source: Creighton University

Employment

Missouri nonfarm employment grew by 17,100 in July. This is a strong number. You would need to go back to January 2023 to find a month where more jobs were added to Missouri’s economy.

However, we must remember this initial jobs number release is preliminary and subject to revision. It would be wise to take a “wait and see” approach to this number. As we discussed a few weeks ago, the national employment numbers for July were mostly flat and previous months were heavily revised downward.

As more surveys are collected, it is possible that Missouri’s data could be revised and reflect the national trend.

Sources: Missouri Economic Research and Information Center, Bureau of Labor Statistics

|

|

|

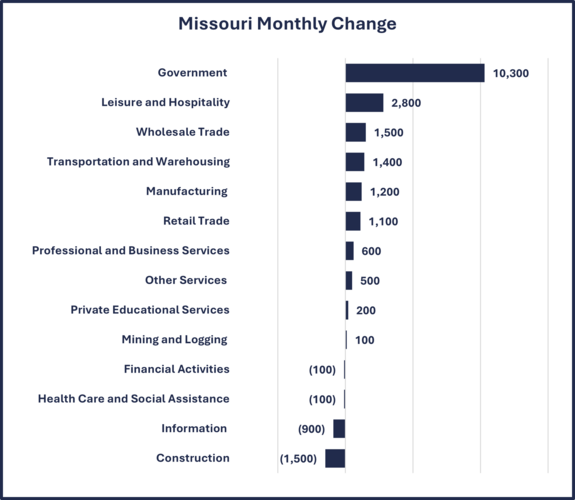

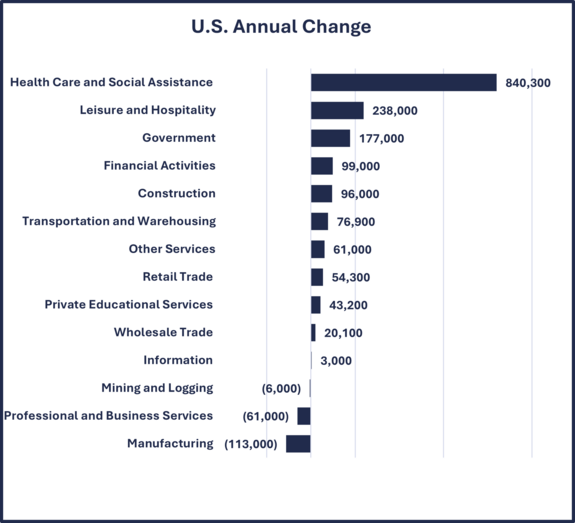

Government was the fastest growing sector, adding 10,300 jobs (10,000 of those were in local government). For the year ending in July, Missouri has added 49,300 jobs. Missouri’s unemployment rate ticked up to 4.1%, just below the national rate of 4.2%.

Sources: Missouri Economic Research and Information Center, Bureau of Labor Statistics

|

|

|

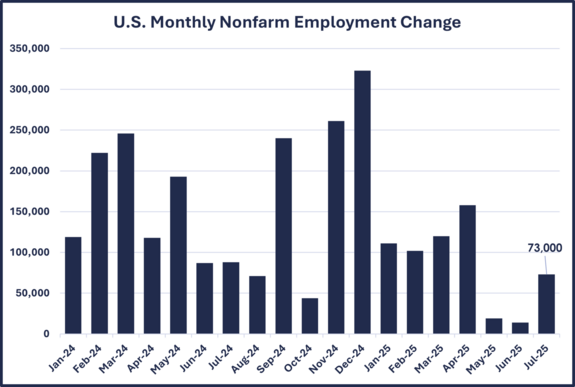

Employment grew by just 73,000 in July - but more importantly, job growth from the previous two months was revised heavily downward (by a combined 258,000).

The U.S. unemployment rate has been steady this year (4.2% in July) despite the slower employment growth. This is due to a leveling off in the U.S. labor force. If the labor force and employment continue tracking at roughly the same pace, the unemployment rate will not change much.

This new and revised data somewhat changes the narrative that U.S. employers were mostly undaunted by outside issues like international trade, immigration, and federal employment cutbacks.

Source: Bureau of Labor Statistics

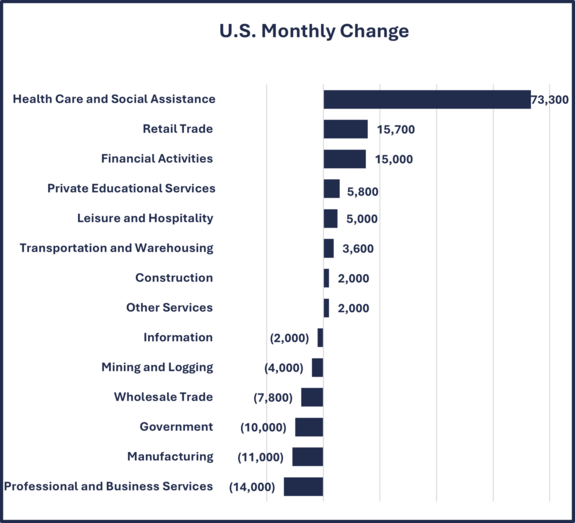

The health care industry continues to be the main driver for employment growth, adding 73,300 jobs in July. We saw declines in professional-business services (-14,000), manufacturing (-11,000), and government (-10,000).

Source: Bureau of Labor Statistics

|

|

U.S. GDP Growth

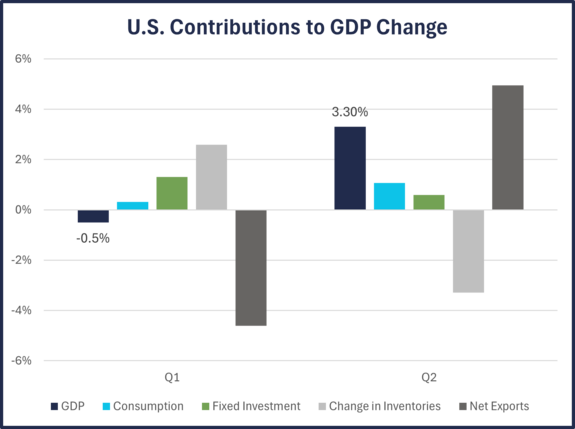

The U.S. economy grew at an annualized rate of 3.3% in the second quarter. This was an expected rebound from Q1, when the economy contracted by 0.5%. The cause for this quarter’s sharp rise is the same cause for the previous quarter’s decline: international trade. In the first quarter, businesses actively stocked up on imports to get ahead of tariffs.

Imports, since they are produced in another country, are counted as a negative in the GDP calculation. With their warehouses full and some tariffs in effect, businesses imported fewer goods in Q2, which resulted in a strong increase in “net exports.” Other details within the data are telling. One, consumption grew at a decent 1.1% rate, telling us that the U.S. consumer is still active.

Fixed investment came in at a modest 0.6% annual rate (which was an upward revision from the original 0.1%). This likely reflects the current uncertain environment as businesses are hesitant to take on major projects.

Overall, this quarter’s number was good, but not a surprise.

Missouri’s GDP figure for Q2 will be released later this month.

Source: Bureau of Economic Analysis

|

|

|

|

|