|

A Newsletter for Employers December 2024 |

|

|

Suggest an article or topic for a future edition of the Employer Advisor newsletter, or just want to tell us how much you enjoy reading it, please send a message to

UIA-EmployerAdvisor

@Michigan.gov.

|

|

This is our final edition of the Michigan Employer Advisor for 2024. We thank you for taking the time to read this newsletter each month and hopefully share it among your colleagues. Our goal is to answer your questions about unemployment insurance in Michigan. If you missed any editions, our Employer Advisor archive goes back two years. You can find a link to the archive on the Employer Homepage at Michigan.gov.

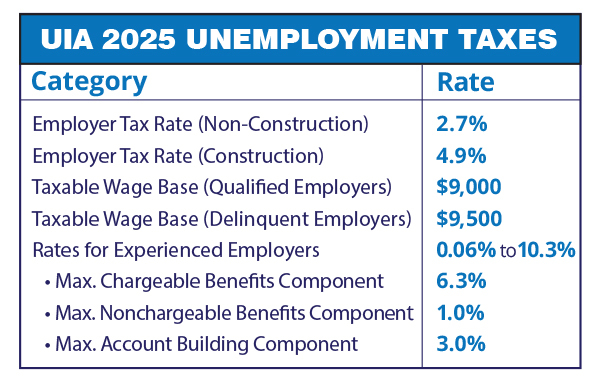

We’re excited to pass along good news for employer across the state: In 2025, the taxable wage base will fall to $9,000 per employee from the current $9,500. Keep in mind, though, employers must be in compliance to qualify for the reduction. Read more below for everything you need to know about the change.

Finally, a reminder that fourth quarter wage and tax reports are due January 25. Filing correct and complete reports is key to whether you qualify for a lowered taxable wage base in 2025.

Happy Holidays and see you again after the New Year!

|

|

|

The taxable wage base will be reduced in 2025 from $9,500 per employee to $9,000 for qualifying contributing employers.

The reduction is triggered if the unemployment insurance Trust Fund balance exceeds $2.5 billion on June 30 and the following calendar quarter.

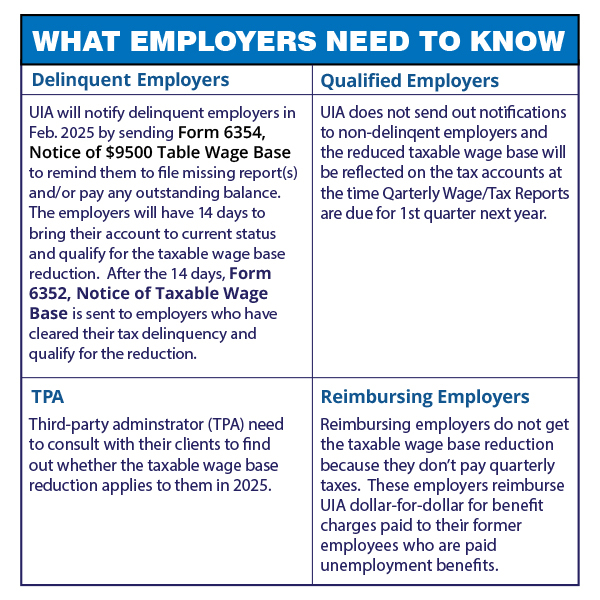

To qualify for the taxable wage base reduction, an employer must be in good standing, which means all the quarterly tax reports are submitted and has no missing reports or estimated reports. Also, an employer cannot be delinquent. An employer is considered delinquent if they have an unpaid balance of $25 or more in tax, penalty or interest.

In February, delinquent employers will be sent Form 6354 Notice of $9500 Taxable Wage Base to remind them to file any missing report and/or pay an outstanding balance. Delinquent employers have 14 days to fix outstanding issues with their account to qualify for the reduction.

|

|

- Read UIA’s news release announcing the lower taxable wage base.

|

|

|

The Michigan Unemployment Insurance Agency (UIA) will mail on Dec. 30, 2024, the Tax Rate Notice for the 2025 calendar year to all Michigan contributing employers.

The deadline for an employer to protest their tax rate is Jan. 29, 2025.

Important things to keep in mind:

1. Missing reports. File any missing report(s) to avoid a Non-Reporting Penalty (NRP) on your tax rate. Please file the missing report(s) within 30 days from the mailing date of the tax rate.

- The 3 percent NRP will be removed if the missing report(s) is filed within 30 days of the rate notice.

- A 2 percent NRP is assessed if the missing report(s) is filed after 30 days but within 1 year of the rate notice.

- A 3 percent NRP will be assessed on missing report(s) filed after 1 year of the rate notice.

- The Potential Tax Rate Increase Due to Missing Report(s) forms were mailed in September.

- If no longer in business, complete a Notice of Change form to close your employer account. The form is available in the Michigan Web Account Manager (MIWAM).

2. Apportionment plan. Apportionment allows unemployment insurance tax payments to be spread out over a full year without penalty or interest. Employers with 100 or fewer employees can participate in the program. Michigan.gov/UIA has more information about the program.

3. New employers with posted Estimated Report. Filing a quarterly tax report is a must. Please review your account to ensure there are no estimated or missing reports.

- If you need assistance to file the report, call the Office of Employer Ombudsman at 1-855-484-2636 and select Option 4.

- If you registered in error, then you must file a Notice of Change form to close your account.

4. Seasonal employers. A quarterly tax report still must be filed even if an employer is not operating due to lack of seasonal work. If there are no wages to report, then a zero-wage report must be filed.

5. Avoid closure of Employer Account Number. This is important for new employers.

The payroll date you have admitted to reaching liability threshold to become an employer is verified when your initial tax report is filed. The employer account is closed if the payroll date does not match the report. Filing a zero-wage report is not an option.

- If your liability falls in the subject quarter or planning to start operation in the future, then complete the Action Needed for Employer Status form, sent by the UIA, for your status to be updated.

- If the business registered in error, then complete a Notice of Change.

- If an officer of a corporation is active in the daily operation of a business, then his or her wages are taxable, and you are required to file a report.

|

|

Definition of a Qualified Employer

- Employers with no missing or estimated reports and a total balance due is less than $25.

- Employers with approved apportionment that are paying each quarter plus the apportioned payment as required.

- Employers that become liable in the TWB reduction year (newly liable and successor employers).

Definition of a Delinquent Employer

- Employers with missing or estimated reports.

- Total balance due is equal to or greater than $25 in contributions, penalties, and/or interest.

- Employers with approved apportionment are only considered delinquent if they don't meet their scheduled apportionment payments.

- Domestic employers that have a balance due from prior years.

|

|

This past year has been filled with learning and progress for UIA, and the project team is hard at work on the MiUI system rollout.

We are in the Build phase of the project, which is when the initial system is being developed. More information to come as work progresses. Concluding 2024 and celebrating the beginning of 2025, we wish you a safe and happy holiday season!

|

|

|

|

|