|

Newsletter for Employers December 2023 |

|

|

The staff of the Michigan Unemployment Insurance Agency’s Tax and Employer Services Division sends its warmest wishes to all of Michigan’s employers for a safe Holiday season and a Happy New Year.

It was our pleasure to be of service to you this past year and we hope to strengthen that collaboration in 2024. We are looking forward to many exciting changes in the coming year, including:

-

Employer Help Center. This reorganization of employer resources and information with a user-focused design will serve as a centralized hub to efficiently manage the most common unemployment tax and claim issues.

-

Redesigned correspondence. We are reimagining key forms and correspondence to employers by leveraging user-friendly design principles and plain language.

-

Translation services. UIA will offer more multilingual resources to enhance employer and claimant access to the agency's services.

We’re very excited about the transformation of the UIA into a national model for fast, fair, and fraud-free service. We hope you are, too.

|

|

As always, if you want to suggest an article or topic for the Employer Advisor newsletter or just want to tell us how much you enjoy reading it, please send a message to UIA-EmployerAdvisor@Michigan.gov. You can view past newsletters on the Employer Homepage at Michigan.gov/UIA. |

|

|

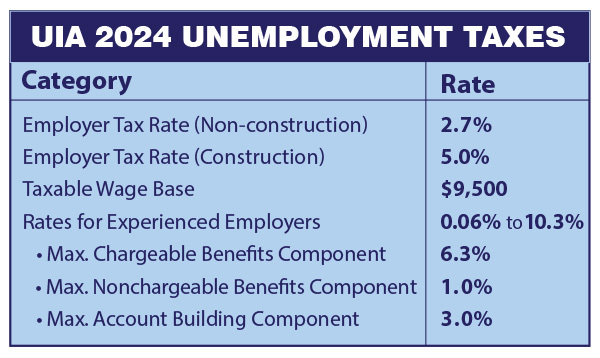

The Michigan Unemployment Insurance Agency (UIA) will mail on Dec. 28, 2023, the Tax Rate Notice for the 2024 calendar year to all Michigan contributing employers.

The Taxable Wage Base for 2024 will remain at $9,500, the same as it was this year. Contributing employers covered under the Michigan Employment Security (MES) Act must pay unemployment insurance taxes on their employees' wages. The taxable wage base is the amount of an employee's wages that is taxed by the UIA each calendar year and is payable by the employer.

For the taxable wage base to change, the UIA Trust Fund must contain at least $2.5 billion for two consecutive quarters. Currently, the Trust Fund is at $2.3 billion.

The deadline for an employer to protest its tax rate is Jan. 29, 2024.

Five other important things to keep in mind

-

Missing reports. File any missing report(s) to avoid a Non-Reporting Penalty (NRP) on your tax rate. Please file the missing report(s) within 30 days from the mailing date of the Tax Rate.

- The 3 percent NRP will be removed if the missing report(s) is filed within

30 days of the rate notice.

- A 2 percent NRP is assessed if the missing report(s) is filed after 30 days but within 1 year of the rate notice.

- A 3 percent NRP will be assessed on missing report(s) filed after 1 year of the rate notice.

- The Potential Tax Rate Increase Due to Missing Report(s) forms were mailed in September.

- If no longer in business, complete a Notice of Change form to close your employer account. The form is available in MIWAM.

-

Changes to the apportionment plan. Apportionment allows unemployment insurance tax payments to be spread out over a full year without penalty or interest. Employers with 100 or fewer employees can participate in the program. That’s up from the previous threshold of 25 or fewer employees.

-

New employers with posted Estimated Report. Filing a quarterly tax report is a must. Please review your account to ensure there are no estimated or missing reports.

- If you need assistance to file the report, call the Office of Employer Ombudsman at 1-855-484-2636.

- If you registered in error, then you must file a Notice of Change form to close your account.

-

Seasonal employers. A quarterly tax report still must be filed even if an employer is not operating due to lack of seasonal work. If there are no wages to report, then a zero-wage report must be filed.

-

Avoid closure of Employer Account Number. This is important for new employers. The payroll date you have admitted to reaching liability threshold to become an employer is verified when your initial tax report is filed. The employer account is closed if the payroll date does not match the report. Filing a zero-wage report is not an option.

- If your liability falls in the subject quarter or planning to start operation in the future, then complete the Action Needed for Employer Status form, sent by the UIA, for your status to be updated.

- If the business registered in error, then complete a Notice of Change.

- If an officer of a corporation is active in the daily operation of a business, then his or her wages are taxable, and you are required to file a report.

|

|

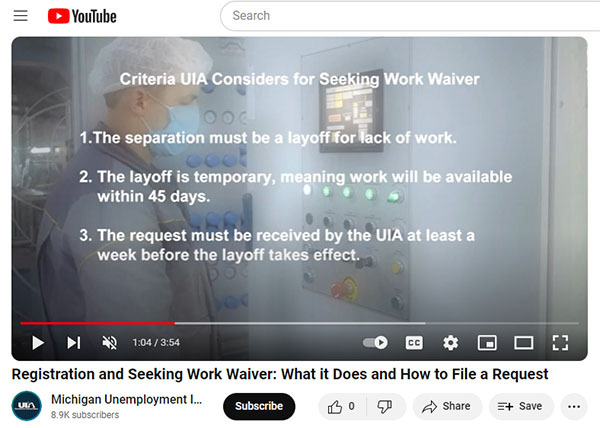

Click on the video above to learn about the Registration and Seeking Work Waiver.

|

|

|

Did you know employers can request a waiver from the Michigan Unemployment Insurance Agency so they don’t lose skilled, trained workers during a short-term layoff?

It’s called the Registration and Seeking Work waiver.

The waiver is a win-win for workers and employers. If granted, workers can collect unemployment benefits during a short-term layoff and they are not required to seek work. For employers, their workforce is available to return to work when they are once again needed.

Watch the video above for more information. If the program is right for your business, you can easily make the request through your Michigan Web Account Manager (MiWAM) account.

|

|

|

|