|

A Newsletter for Employers April 2023 |

|

![Webinar on Resources for Hiring Returning Citizens [Video still Image]](https://content.govdelivery.com/attachments/fancy_images/MILEO/2023/04/7473834/video-capture-resources-4-hiring-returning-citizens_original.jpg)

The Michigan Unemployment Insurance Agency has a fantastic free opportunity for employers who need legal representation for an issue with our agency. The Advocacy Program has been providing services for employers and workers since 1991 and last year helped more than 800 employers. See the story below about how to take part in this important service UIA provides for qualified employers.

While we’re talking about services UIA provides to employers, the UIA’s Barbara Stephens participated in an Employment and Training webinar in March focused on workers returning to the workforce. As part of the Resources for Returning Workers presentation, Stephens discussed the Work Opportunity Tax Credit (WOTC), which is a federal program administered by UIA and provides up to $9,600 in tax credits if a business hires workers from targeted groups, such as military veterans. Our WOTC webpage has resources, a video and program information about the program. Keep these two helpful hints in mind if your company decides to participate:

- Have all the necessary paperwork in hand when applying, including documentation from the employee.

- Apply for the program and upload all documents through your MiWAM account. Electronic and complete applications will be processed much more quickly than incomplete, paper applications.

In case you missed the webinar, you can watch it online.

|

|

|

Finally, a reminder that the window is closing to apply for the UIA program that allows a business to distribute its first quarter unemployment insurance tax obligation over four quarters. To participate, select the Apportionment option in your MiWAM account before first quarter reports are due April 25. Learn more about the program on our website and in this letter sent to all employers who have fewer than 100 workers. |

|

The UIA is announcing the return of its UI Outreach initiative through the Office of Employer Ombudsman (OEO). This unemployment insurance program will provide an understanding of the UIA, hands-on assistance in navigating the Michigan Web Account Manager (MiWAM) portal and other helpful information.

Beginning in May, you can schedule Employer Seminars, which offer an opportunity to engage with expert speakers, learn more about current regulatory changes, and provide valuable insight on protecting your business.

OEO is a team of dedicated business professionals and skilled communicators who can coordinate and produce educational resources on important unemployment insurance topics of interest. Whether it is a specialized issue or a general overview, we are committed to delivering exceptional service and achieving customer satisfaction in every phase of assistance.

To schedule an Employer Seminar, e-mail UIA-EmployerAdvisor@Michigan.gov.

|

|

|

|

If a business has employees who work in more than one state, a set of tests are used to determine in which state the employee could qualify for jobless benefits if terminated through no fault of their own.

The tests are applied in this order:

-

Majority of Services. In what state did the employee perform most of

their services?

-

Base of Operation. Does the employee perform some services in the state

in which the business has a base of operation?

-

Place of Direction and Control. Did the employee perform services in the state from which they receive direction and control?

-

Employee's Residence. Did the employee perform services in the state in which they live?

-

Services Not Performed in Any State. If answers to the questions do not apply, the employer may either:

- Elect to file with any state in which the employee performed some service and report all wages earned to that state.

- Report the employee’s earnings to each state in which the employee performs services.

Relocating to Michigan

Wages from another state should only be reported if the employee worked in a different state before relocating to Michigan and all wages earned going forward are from services performed in Michigan.

If the employer chooses to report wages to Michigan, the wages earned in the other state before relocating can be reported on the business’ quarterly tax report under the Out-of-State Wages tab. No out-of-state wages should be reported in any quarters after the worker came to Michigan.

For example, if an employee worked in Montana and in May 2022 relocated to Michigan. On the June 30, 2022, quarterly tax report, the year-to-date wages from January to May 2022 that were earned in Montana are reported on the Out-of-State Wages tab. Wages from May to June 2022 earned in Michigan are reported on the Combined Report tab. The wages earned in Montana are only reported once and are not reported in later quarters.

Working in Multiple States

If the employee works in multiple states, the localization of services test will determine where the wages should be reported.

Here’s one example: An employee works approximately the same amount of time in Indiana, Ohio and Michigan. The base of operation is in Michigan, the employee lives in Indiana, and direction and control of work comes from the employer in Ohio. This is considered Michigan employment since some services are performed in Michigan where the base of operation is located. All wages should be reported to Michigan on the Combined Report tab. No wages are reported under the Out-of-State Wages tab.

Let’s look at another example: An employee performs services in Michigan and Indiana. The employee lives in Indiana and direction and control come from Ohio. This is Indiana employment since the services are performed in more than one state and some services are performed in Indiana where the employee lives. All wages should be reported to Indiana.

If the employer chooses to report wages to all states where the employee works, then the wages earned in other states cannot be reported to Michigan. Only the wages earned in Michigan are reported to Michigan under the Combined Report tab. No wages are reported on the Out-of-State Wages tab.

|

|

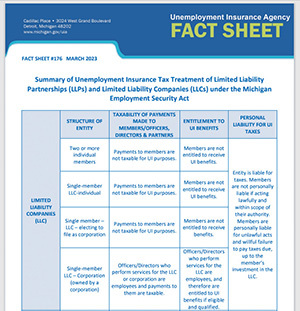

Have you ever wondered how unemployment insurance taxes are treated in Michigan for limited liability corporations (LLC) or limited liability partnerships (LLP)?

UIA now offers a new fact sheet to assist employers in sorting out any confusion when filing a quarterly Wage/Tax Report relating to payments made to LLC or LLP members.

Members who perform services for the LLC, including partners for the LLP, are not considered employees. Payments received by the members of an LLC or partners of an LLP for services performed – including members electing to file federal taxes as a corporation – are not taxable wages for Michigan unemployment tax purposes. The payments are not reportable on a quarterly report and those members, if separated, are not eligible for UI benefits.

However, if an officer or director of a corporation performs services, then the wages must be included on the quarterly report, and they are eligible for jobless benefits.

|

|

|

The UIA offers a free program that provides employers legal representation at a hearing before an administrative law judge if they disagree with a determination or redetermination from the UIA. The Advocacy Program offers information, consultation, and representation services.

Agency staff determine eligibility for the program and approved employers can choose an advocate from a statewide network of qualified independent consultants to help them prepare for their hearings before the Michigan Office of Administrative Hearings and Rules (MOAHR). Advocates are independent contractors, not UIA employees. The advocates are not required to be attorneys, but some are, and all have knowledge of the hearing process and Michigan’s unemployment insurance laws.

Advocates will consult with employers regarding the merit and preparation of their cases. If the advocate believes the case has no merit, he or she will, before the scheduled hearing, provide the employer with a written explanation of why they believe this to be the case. Otherwise, the advocate will provide representation for the employer for their hearing, except for cases specifically excluded. When making your selection, be sure the advocate is available for your scheduled hearing date and time and is willing to appear for you either in person or on the phone.

If you are interested in advocacy assistance, contact the Advocacy Program after you have received a Notice of Hearing. You must secure assistance no later than two business days before the scheduled hearing date. Failure to secure an advocate in a timely manner is not sufficient reason to reschedule a hearing.

UIA has developed a helpful video that explains the program benefits and how it works. After watching the video, visit the Employer Advocacy Program webpage for more details. You can contact the Advocacy Program by calling 1-800-638-3994.

|

|

|

|

|

|