|

A Newsletter for Employers February 2023 |

|

Happy February! With the unfortunate forecast that Michigan’s “Woody the Woodchuck” and the classic Punxsutawney Phil (of Pennsylvania) saw their shadows, we are in for six more weeks of winter and no early spring. I hope the information in this month’s Michigan Employer Advisor will keep you warm and cozy.

In this issue, we want to provide information about reimbursing employer options, meeting important dates to avoid unnecessary fees and interest, what to do if you sell or close your business, an employer survey about hiring resources, and other important facts.

|

As always, if you want to suggest an article or topic for the Employer Advisor newsletter or just want to tell us how much you enjoy reading it, please send a message to UIA-EmployerAdvisor@Michigan.gov. You can view past newsletters on the Employer Homepage at Michigan.gov/UIA.

|

|

Governmental entities, Indian tribes and tribal units are, by law, reimbursing employers.

A 501c3 non-profit employer is considered a contributing employer by default but has the option to be classified as a reimbursing employer. An out-of-state governmental employer is only treated as a reimbursing employer if it is partnered with a Michigan governmental entity.

A reimbursing employer does not pay quarterly taxes to the Michigan Unemployment Insurance Agency (UIA). Rather, it pays dollar-for-dollar the amount of UI benefits that were paid in a calendar quarter to former employees. The employer is required to report to UIA quarterly employee wages and the UIA determines eligibility for benefits based on the wages reported. Each quarter, the employer will receive UIA Form 1763, Reimbursing Employer Billing for Benefit Charges which includes the balance due to be paid quarterly and annually based on organization type.

Only an entity that is classified by the federal Internal Revenue Service (IRS) as a church is exempt from paying Michigan unemployment taxes. Any other type of “religious” non-profit 501c3 entity is subject to reimbursement liability status and state unemployment taxes.

Employers may change their status from reimbursing to contributing by submitting a written request no later than Dec. 2 of the preceding year in which it plans to change.

Non-profit entities with 501c3 status, Indian tribes/tribal units, and out-of-state governmental units without an affiliated Michigan base are subject to security requirements. To retain reimbursing status, they must provide an original ink-signed or stamped security in the form of surety bond or letter of credit if its gross annual payroll (salary/wages) equals or exceeds $100,000.

The security must be updated annually based on an increase in gross annual payroll or coverage period of the expiration date.

|

|

|

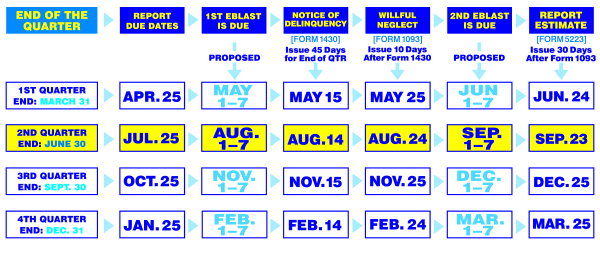

Michigan UIA makes every effort to inform employers of their tax obligation so they do not become delinquent in filing required Quarterly Wage and Tax reports. The chart below reflects all quarterly report due dates, email reminders, delinquency letters and deadlines for employers to meet to avoid penalty and interest charges before an estimated report is calculated and considered delinquent. |

|

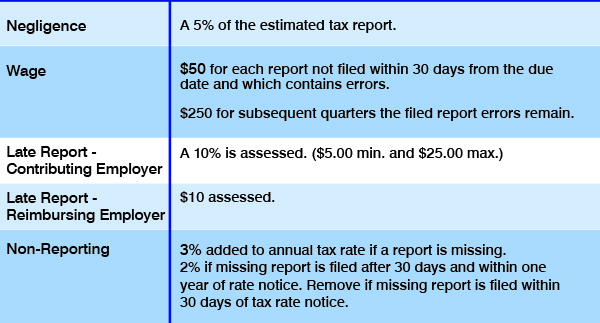

Filing corrected, timely and missing reports will eliminate the following penalties: |

|

You may request a waiver for these additional penalties after corrected reports are filed and all principal taxes are paid in full. |

|

If you no longer have employees, or if you are closing or selling your own business, you must notify the Michigan UIA of your change in payroll

by completing and submitting the UIA Form 1772 Notice of Change. This form is used to determine termination of liability and discontinuation of active UIA account status.

Form 1772, found in your MiWAM account or on the UIA website, lets you provide information about the new owner of your business if selling it to someone else.

UIA will automatically change the Employer Account status to inactive after eight quarters of no payroll activity. Filing a zero-wage report is considered no payroll activity. After the Employer Account Number (EAN) status is changed to inactive and remains in inactive status for an additional four quarters, the EAN is then terminated and UIA Form 1366, Termination of Coverage of Determination Under Section 24(c) of the Michigan Employment Security Act is issued.

The EAN can be restored to active status either before the account is terminated or up to one year after the termination notice is issued. UIA does not have jurisdiction to restore the account to active status if a request to reopen a terminated account is received more than a year from the date the termination notice is issued.

|

|

|

The Michigan Department of Labor and Economic Opportunity’s Office of Employment and Training is looking for feedback about State of Michigan resources to help in hiring returning citizens.

One such resources is the federal Work Opportunity Tax Credit (WOTC), administered by the Michigan Unemployment Insurance Agency (UIA). WOTC provides up to $9,600 in tax credits to private, for-profit employers who hire workers from targeted groups, such as ex-felons or veterans, that traditionally experience difficulty joining the workforce.

The WOTC program will be explained in more detail in a free Office of Employment and Training webinar in March about resources available to employers, such as the Fidelity Bonding Program, Clean Slate Program, and others. (Fidelity Bonding protects employers from money or property losses due to dishonesty by high-risk workers.)

In preparation for the webinar, planners want to know how familiar employers are with the programs that are available. Please take 5 - 10 minutes for a short survey about Resources for Hiring Returning Citizens.

UIA provides a WOTC video, brochure and fact sheet to help employers decide if the program is right for their business.

The Office of Employment and Training is offering a webinar from 11 a.m. to noon Feb. 22 about resources that support retaining employees. Resources include Michigan's Tri-Share Childcare Program, adult education and literacy programs, and business resources networks. You must register for the free event.

|

|

|

|

|