|

A Newsletter for Employers January 2023 |

|

|

Happy January! I hope your holidays were spectacular as we jump into this New Year. I know the Michigan Unemployment Insurance Agency has many exciting initiatives planned for 2023, so watch this space for updates in the coming months.

We know that January is a busy month for employers. Our Office of Employer Ombudsman is available for you during business hours to help in all your UIA needs. OEO is the business community’s go-to source to troubleshoot general unemployment and UI tax-related issues. You can reach the Ombudsman’s office staff by calling 1-855-484-2636.

I want to highlight one of the many services UIA provides to employers. Our Advocacy Program provides assistance at no cost to employers who need legal help at initial protest hearings of UIA determinations before the Michigan Office of Administrative Hearings and Rules (MOAHR). Employers can choose an advocate from a statewide network of qualified independent consultants. The Advocacy Program can also be used by workers who dispute UIA determinations. Click on the video image below to learn more about this free program.

|

|

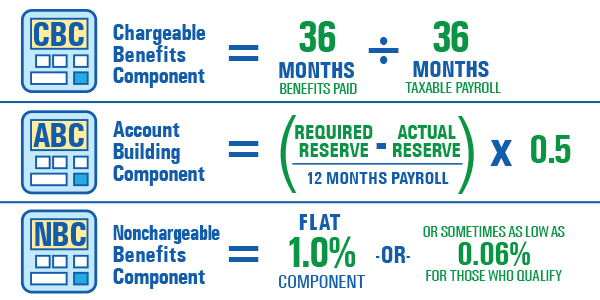

At the end of December, the Unemployment Insurance Agency mailed its tax rate information for 2023 to all registered businesses in Michigan.

If the tax rate listed on Form 1771 Determination of Tax Rate has changed, this may be why:

-

Are there benefit charges? This may affect the three components (Chargeable Benefits, Nonchargeable Benefits, and Account Building) that are used to set a business’ tax rate.

-

Did the total gross payroll for the computation period increase?

This affects the required reserve amounts.

-

Did the business change ownership or buy another business? This affects all components of the tax rate.

-

Are there missing Quarterly Wage/Tax report(s) for the calculation period? If so, a 3 percent non-reporting penalty is added to the tax rate.

|

|

|

|

If the change is a result of benefit charges, this may be related to former employees. If you agree with the charges, then no further action is necessary. If you disagree with the benefit charges or they do not relate to former employees, you can file a claim/benefit protest with the UIA.

If you disagree with the tax rate increase and your protest is pending, it won’t change your tax rate until the disputed benefit claim/charges are adjudicated. Notify UIA if your tax rate remains unchanged after the claims/charges have been reversed. Your tax rate can be reconsidered by protesting the rate notice within 30 days after the benefit credit has been mailed.

Please be patient with the UIA as it diligently works through all adjudications to apply and post benefit credits that may reconsider any prior tax rate determination.

|

|

Employers can designate a Third-Party Administrator (TPA) to act on behalf of the business when interacting with the UIA. The TPA needs an approved power of attorney (POA) to represent the employer and also receive tax information, including benefit correspondence.

If an employer wants to establish a TPA, it can grant power of attorney client access to its business using the Michigan Web Account Manager (MIWAM) online account and select the desired level of access.

Another form of TPA is a Professional Employer Organization (PEO). The PEO can be issued a 940 Certification for taxes paid while the party holding a power of attorney designation cannot.

The PEO must have PEO-client access with UIA to obtain certification. If the organization only has POA-client access, it must be re-established as PEO-client. If the organization is unable to add PEO-client in MIWAM then it does not have the correct designation type in the Michigan Data Automated System (MIDAS). Work with UIA staff to be associated with the appropriate representation type.

It’s no longer necessary to complete Form 1488 Power of Attorney. The form is not required since both the TPA and the employer are able to add the POA in MIWAM. However, if UIA staff request the form it must be provided.

|

|

|

|

Here’s how to add and grant authorizations to third-party administrators:

- The TPA must create a MIWAM account if one does not exist.

- The TPA can then add the client to their MIWAM account.

Once a third-party administrator is approved to receive mail, any correspondence from UIA will be directed to the TPA, so there is no need to change the address on the employer’s account.

Employers are encouraged to review their accounts periodically. Many third-party administrators do not have appropriate levels of authorization to receive or read UIA mail, do not register accounts on time, do not register in the correct state, use outdated addresses, do not correct errors, and do not respond to collection notices.

If the arrangement between a TPA and employer is terminated, ceasing the authorization in MWAM will prevent any further mail from being directed to the TPA.

The TPA or the employer must cease the PEO or POA authorization in MIWAM, including the authorizations with mailing permissions. If the employer sells its business or goes out of business, it is very important to submit a Form UIA 1772 Discontinuance of Business in a timely manner. Failure to end the authorizations will prevent any subsequent TPA you designate from gaining mail authorization access.

|

|

Michigan employers can qualify for a federal unemployment tax credit if they pay their state unemployment tax. By the end of January of each year, employers must submit Form 940 to the Internal Revenue Service (IRS) to report their annual taxable wages for the previous year to receive the federal tax credit.

Under the Federal Unemployment Tax Act (FUTA), the IRS will verify with Michigan that the credit claimed by an employer on Form 940 or Schedule H was paid into Michigan’s unemployment fund in order for a business to receive the maximum FUTA credit.

If there is a discrepancy in the reporting on the Form 940, then the employer can request a recertification Form 940-c, which includes:

- Experience rate.

- Liability date.

- State reporting ID number.

- Year of the requested 940-C.

- Experience rate period (Jan. 1 through Dec. 31).

- State taxable wages.

- Contributions paid before Feb. 1, between Feb. 1 and Feb. 10,

and after Feb. 10.

|

|

|

|

When a Professional Employer Organization (PEO) requests a 940 certification for their clients, they must provide Form 6324, Certification by PEO Regarding Payment of Wages to Leased Employees.

This form establishes the PEO relationship before Form 940-c can be issued. The representation type must also reflect PEO-client access. A general power of attorney authorization means the PEO has the same rights as the employer.

|

|

-

The employer reports the payments of the obligation assessment portion of the rate through calendar year 2019. The obligation assessment portion of the rate is excluded from the tax paid on Form 940-c.

-

If a company is sold in the middle of the calendar year, the buyer does not include wages paid by the seller. The taxable wage base is adjusted to include the wages from the previous employer.

-

Notify the UIA if the employer changes its Federal tax ID number (FEIN)

in the middle of the tax year or reorganized its business structure.

-

The employer must verify that the FEIN on their State Unemployment Account is correct to minimize reporting errors. The UIA reports the Form 940-c by the FEIN.

|

|

|

|