|

A Newsletter for Employers APRIL 2022 |

|

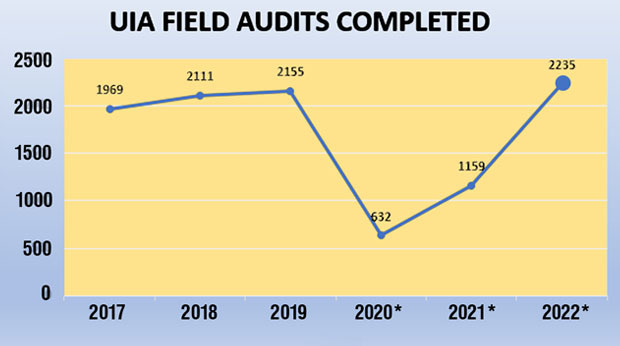

I hope this month finds you well and happily expecting Michigan spring weather! In this edition of the Michigan Employer Advisor, we explore the depths of our Audit Section. This area employs 32 staff throughout the State of Michigan that work hard to make sure all Michigan employers report accurate wages and equitably contribute to the fund that provides benefit payments to employees that are unfortunately laid off due to no fault of their own. |

|

Meet Danene Test, who is our audit manager. She has

28 years of experience and background in investigation, inspections, and audit with the State of Michigan.

The most asked questions are about misclassified workers and what to do if you are being audited. Danene provides details in this article to help you sort out your questions.

Additionally, UIA has released a presentation for new business owners on how to register as a liable UI employer. Please view the video and study the toolkit on our Tools and Resources webpage at Michigan Employer Liability Toolkit. Please pass this information along to any aspiring new business owners in Michigan.

If you want to suggest an article or topic for this newsletter or just want to tell us how much you are enjoying it, please send a message to:

UIA-EmployerAdvisor@Michigan.gov. You can also view past newsletters on our Tools and Resources webpage.

|

|

|

The UIA’s Field Audit and Employer Compliance Sections are responsible for identifying employer non-compliance. Non-compliance can sometimes be unintentional, honest mistakes made by employers, or intentional schemes.

There can be many types of employer

non-compliance including:

-

Misclassification

- An employer incorrectly classifies a worker as an independent contractor to avoid paying the unemployment insurance tax when legally the worker is an employee.

-

State Unemployment Tax Act (SUTA) Dumping

- An employer attempts to shift workforce or payroll, between entities to avoid paying established or higher unemployment tax rate or liability.

- Unreported and Under-reported Employee Wages

-

Fictitious Employer Schemes

- A fabricated business is registered with the UIA in order to obtain unemployment benefits under false pretenses. The false entity reports fake payroll and wages for non-existent employees and then files benefit claims as if those employees are laid off and collects benefits under those names.

-

Employer Fraud Schemes

- Misrepresentation or non-disclosure of information by an employer in order to avoid or to reduce the unemployment contribution liability. This can also be collusion between employers and employees to help the individual obtain unemployment benefits to which they

are not actually entitled to.

|

|

|

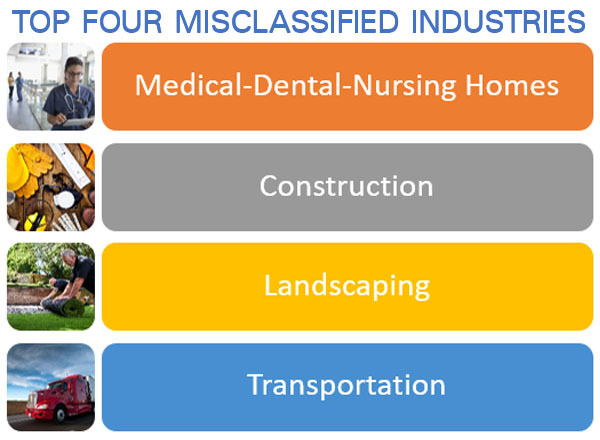

Misclassification of employees is a problem that impacts employers, workers and government. When workers are misclassified, they may not qualify for certain benefits, while government loses important tax revenues. The only party to benefit through misclassification is the non-compliant employer who achieves an unfair business advantage over its competition.

Misclassification most commonly occurs when an employer hires a worker and improperly classifies them as an independent contractor rather than as an employee.

UIA created Fact Sheet 155- Independent Contractor or Employee to help employers properly classify a person’s services.

What is an employee? The employer determines what needs to be done and controls how it is to be done. The person is normally directed by the employer.

What is an independent contractor? They are not employees but are in business for themselves. They are hired to accomplish a task or tasks as determined by the employer, but independent contractors retain the right to control how they will get the work done. Generally, an independent contractor performs a specialized service that is not central to the overall function of the business.

How are wages reported? Independent contractors should receive from employers Internal Revenue Service Form 1099-MISC, which reports payment of "non-employee compensation." Employees receive a W-2.

Often, wages for part-time, temporary, probationary, substitute and casual labor workers are misclassified, as well. Although a worker's job may be less than permanent or full-time, the worker is still an employee. Misclassification also occurs when workers operate in the "underground economy" and are typically paid in cash. The wages these workers receive are not reported, and the workers do not receive a 1099 form or a W-2 from their employers.

|

|

|

|

When a worker is misclassified, they may:

- Be ineligible for unemployment insurance and workers' compensation benefits.

- Lose other labor law protections such as minimum and prevailing wage, overtime, health and safety, and family and medical leave.

- Become liable for their full Social Security taxes and must report their own income taxes.

- Receive less in Social Security benefits at retirement as the unreported wages are not credited toward the employee's potential Social Security entitlement.

- Lose access to employer-based benefits, such as health insurance.

Employers who misclassify their employees, may:

- Avoid paying income taxes, FICA taxes, unemployment taxes and workers' compensation premiums on workers that they do not classify as employees.

- Underbid employers who do not misclassify their employees.

UIA is taking action to correct the problem of employee misclassification. It receives from the IRS statewide listings of employers who are issuing 1099-MISC statements, including workers who receive 1099-MISC statements from their employers.

UIA also coordinates with the Bureau of Employment Relations Wage & Hour Division, the Workers' Disability Compensation Agency and the IRS in Questionable Employment Tax Practices (QETP). This state and federal partnership has resulted in coordinated efforts in other tax areas to ensure that appropriate taxes are being fairly paid by all employers.

|

|

|

As a registered contributing employer, you may be selected to participate in a UI audit. The audit will be looking for verification of wages, compliance with hearing or court rulings, securing delinquent tax returns, the filing of claims for bankruptcy or other circumstances that may arise in the normal course of business.

An audit may occur either in person by a scheduled visit from one of our auditors or using our electronic audit process where employers can submit the required documents via the secure document portal in MiWAM.

Auditors will meet with you or your designated representative to explain the process. The auditor will then review the books and records and discuss with you the audit results. The auditor will provide a written report summarizing findings and conclusions along with a notice of refund or tax due that includes penalties or interest. The auditor will explain your rights and responsibilities as an employer.

After the conclusion of the audit, you will be asked to complete a Post Audit Employer Survey, which can be sent to UIA-FieldAuditSurveys@Michigan.gov.

|

|

|

|