|

A Newsletter for Michigan Employers February 2022 |

|

This issue of the Michigan Employer Advisor is packed full of helpful information for employers. Are you aware that the Unemployment Insurance Agency has many programs that assist you? The Office of the Employer Ombudsman would be pleased to share with you information about our Work Opportunity Tax Credit program, Work Share, Employer Filed Claims, and our first quarter Apportionment option. This issue of the Employer Advisor will also include information regarding the delay of UIA’s Form 1099-G statements.

We also included a snapshot of the report delinquency criteria for your quarterly wage reports. Recently, many employers received a UIA Form 6367, Determination of Pattern of Non-Responsiveness. If you received one of these letters, it means the UIA did not receive a timely or adequate response to a request for information in 2021. This results in a nonresponsive determination. To avoid this in 2023, make sure you promptly and adequately respond to UIA correspondence this year. Failure to do so may negatively impact receipt of future credits to your account.

|

|

|

This annual letter is a notification to you regarding the Agency’s finding of a pattern on all determinations issued during the previous calendar year. If you disagree with the determination, you may submit a protest. The protest rights are listed on the reverse side of the letter. Also,

You may only protest the finding of a Pattern of Non-Responsiveness, each case listed may not be contested

at this time. If you disagree with the individual case which contributed to the pattern, please directly protest the individual non-monetary case on the appropriate letter.

If you want to suggest an article or topic for this newsletter or just want to tell us about how much you are enjoying it, send a message to:

UIA-EmployerAdvisor@Michigan.gov.

You can view the past newsletters at Michigan Employer Advisor Archive.

|

|

|

|

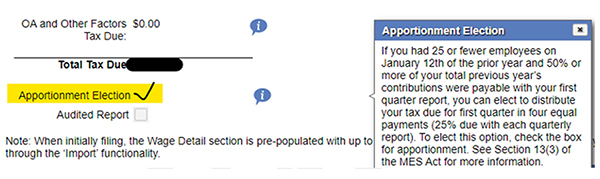

UIA has an apportionment program that allows qualified employers that incur a very large amount of their tax payment during the first quarter of the year to spread their tax payment into four quarterly installments. To take advantage of the apportionment option for the first quarter 2022 tax payment due April 25, you must have:

- 25 or fewer employees by January 12, 2021.

- 50 percent or more of your total previous year’s contributions were payable with your first quarter report.

There are no penalties or interest if you participate in the apportionment program. However, you still are responsible for the taxable wages for the three remaining quarters of the year.

To take advantage of the apportionment option, make sure that you check the appropriate box when completing your return.

|

|

UIA has been experiencing a large backlog due to the immense workload created by the COVID-19 pandemic. The agency is reviewing and processing previously submitted documents. As a result, you may receive a request for information —

such as Remuneration-Earned Income, separation information and/or monetary redeterminations — for claims that may be a year or more old. Please do not disregard these letters. You must respond as required to avoid non-responsive employer status. |

|

|

You may be getting questions from employees who have not received Form 1099-G. UIA received approval from the IRS to delay sending out the forms, which report the amount of benefits received and taxes withheld. The 1099-Gs now have been uploaded to all MiWAM accounts and will be mailed to claimants by February 28.

We are sorry for the inconvenience.

The UIA recently identified a problem with the production of 1099-Gs for calendar year 2021. Implementing the changes necessary to ensure the accuracy of the tax forms will cause a delay in issuing the statements.

|

|

|

UIA must verify reported wages in the first initial Wage/Tax report that liable employers provide on their Form 518, Michigan Business Tax Registration. The payroll date must be consistent with the reported wages of $1,000 (or $20,000 if an agriculture employer) for an account to remain active.

If there is a mismatch for the report, the employer will receive a UIA Form 6442, Action Needed for Employer Status for the following reasons:

- You filed a zero wage/tax report or wages less than the admitted payroll date in the quarter that liability occurred.

- There is no report filed by the employer during the liability quarter.

To correct the liability date, the employer must complete and return Form 6442 within 10 days to stop UIA from changing the account status to non-liable. Non-liable employers will not be able to perform the following tasks.

- File tax reports in MIWAM.

- Add a power of attorney to the account.

|

|

|

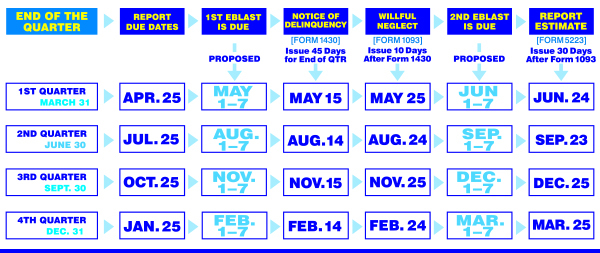

To avoid employers becoming delinquent in filing required Quarterly Wage/Tax reports, the UIA makes every effort to inform employers of their tax obligation. The chart below includes all quarterly report due dates, email reminders, delinquency letters and deadlines for employers to avoid penalty and interest charges before an estimated report is calculated to your account and considered delinquent.

A larger print-ready version of the handy chart shown below is available if you go to Michigan.gov/UIA.

|

|

|

|