|

Greetings District 6 Residents,

Thank you for contacting me, sharing your thoughts regarding CB-48-2020, a proposed Charter Amendment that may be placed on the November 2020 General Election ballot for voters in the County. I appreciate the opportunity to respond and hopefully inform you on both what the bill does and does not do, what the State Homestead Tax Credit Cap is as well as my efforts, and those of the County Council over the past several years to understand its impact on our quality of life.

First, I think it is important to give you background information, history of the Homestead Property Tax Credit Cap and recent County efforts to address our fiscal situation. Second, to clarify what the Charter Amendment process and CB-48-2020 are and are not. Lastly, to explain the bill's context as we address larger issues currently facing the County.

State Homestead Property Tax Credit

The Homestead Property Tax Credit is a State enacted program (see Section 9-105 of the Tax-Property Article of the Annotated Code of Maryland) which spreads out over a three-year process the implementation of the real property tax for any increase in the assessed value of one’s primary residence.

The Homestead Credit limits the increase in taxable assessments each year to a fixed percentage. All counties and municipalities in Maryland are required to limit taxable assessment increases to 10% or less each year and an owner must apply for it. Under State law, every property (residential and commercial) is assessed every three (3) years based on market conditions and other sales information.

An example of this process is as follows:

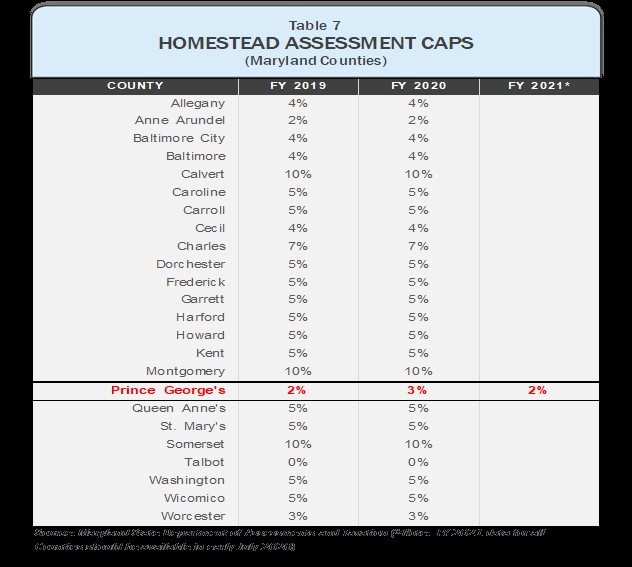

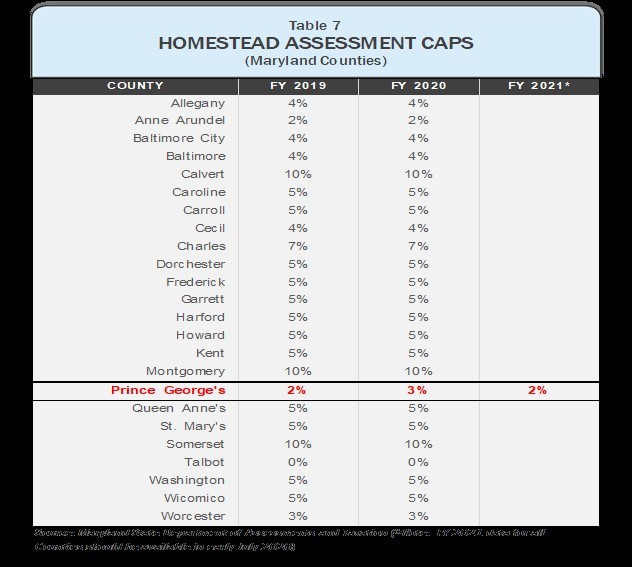

Assume that your old assessment was $100,000 and that your new phased-in assessment for the 1st year is $120,000. An increase of 10% would result in an assessment of $110,000. The difference between $120,000 and $110,000 is $10,000. The tax credit would apply to the taxes due on the $10,000. If the tax rate was $1.00 per $100 of assessed value, the tax credit would be $100 ($10,000 ÷ 100 x $1.00). This table shows the most recent Homestead Assessment Caps for all Maryland Counties and Baltimore City:

This table shows the most recent Homestead Assessment Caps for Large Municipalities in Maryland (population > than 5,000), including those in Prince George’s (including in Bowie, Greenbelt and District Heights, the only municipality in our Council District):

Cap In Prince George’s County

In 1992, the residents of the County, through a voter approved referendum question, imposed the current County Homestead Property Tax Credit Cap in the County Charter Section 812 (d):

“In accordance with the provisions of Section 9-105 of the Tax-Property Article of the Annotated Code of Maryland, on or before January 1 of each year, the County Council shall set, by law, the homestead credit percentage for the taxable year beginning the following July 1. The homestead credit percentage shall be no greater than 100% plus the percentage of increase in the Consumer Price Index for the previous twelve months, rounded to the nearest whole number, but not more than 105%.”

Prince George’s has operated under this Cap for over 28 years. And it has had a financial impact on both our residents and the County. For a listing of the Cap amounts since the County Cap was imposed, please review Council Bill 43-2019, an act concerning the Homestead Property Tax Credit for the purpose of establishing the homestead property tax credit for the County property tax for the taxable year beginning July 1, 2020. Please note that the County has only hit the 105% Cap twice in almost 30 years because of the CPI requirement.

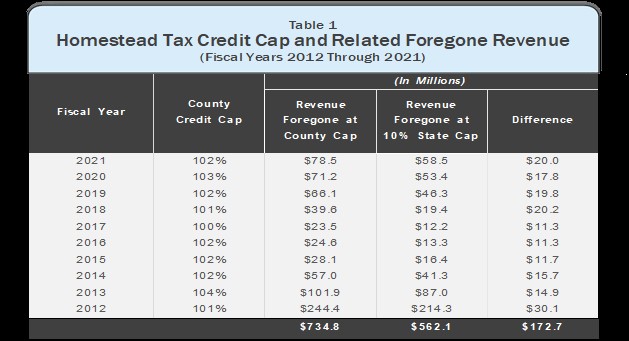

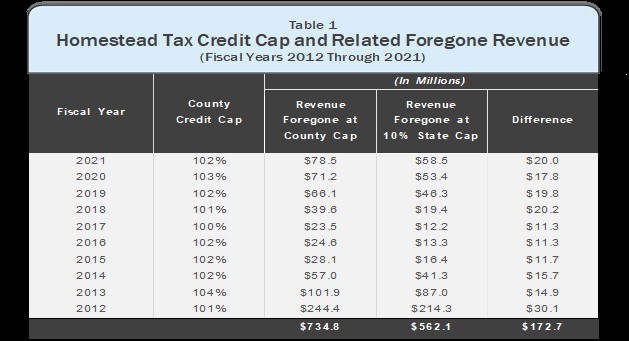

This Table shows the impact of the self-imposed 5% or CPI Cap over the past ten (10) County Fiscal Years:

County Financial Condition Studies

Within the past several years, the County and Council have undertaken substantial reviews of our financial conditions and programs. Here’s a brief summary and links to recent reports conducted:

-

Blue Ribbon Commission on Addressing Prince George’s County’s Structural Deficit

In 2016, the County Council established a 15-member Blue Ribbon Commission on Addressing Prince George’s County’s Structural Deficit, which had the charge to recommend policies to the County Council and County Executive that will address the County’s structural deficit – the imbalance caused when normal government spending exceeds tax revenues on an annual basis.

The Commission collected, reviewed and discussed comparative budget data and information regarding Prince George’s County’s fiscal health; policies and practices that affect Prince George’s County’s revenue structure and the strength of its tax base; the structure and fiscal dynamics of the Prince George’s County Government; and feedback from community stakeholders concerning the County’s budget and tax structure.

The Commission’s Final Report was issued in January 2017 and made several recommendations, including seeking the repeal of the Cap on the Homestead Property Tax Credit to give the County more flexibility.

For a copy of the Final Report and other materials, please link to https://pgccouncil.us/487/Blue-Ribbon-Commission.

2. Prince George’s County Tax Credit Reform Commission

In 2018 the County Council established a 17-member Prince George’s County Tax Credit Reform Commission to review and analyze all existing and proposed tax credits in the County to determine the tax credit’s effectiveness, utilization, and efficacy in the County, and to recommend reform of the tax credit policy based on its review and deliberations.

This Commission issued its final report in September 2018 and found that the Homestead Property Tax Credit was the largest of the all the tax credits in the County, representing approximately $51.5 million or 81% of all tax credits in Fiscal Year 2018 dollars. The Commission also posed several questions about expansion of additional tax credits, including not recommending any additional real property tax credits.

For a copy of the Final Report and other materials, please link to https://pgccouncil.us/593/Tax-Credit-Reform-Commission.

CB-48-2020

CB-48-2020 is NOT a tax increase. It is a Charter Amendment that would be voted on by voters in Prince George’s County in the November General Election.

CB-48-2020, as proposed, would ask the voters to consider whether to change the County’s Charter Section 812. It would ask the following question in November:

“In accordance with the provisions of Section 9-105 of the Tax-Property Article of the Annotated Code of Maryland, on or before [January 1] March 15 of each year, the County Council shall set, by law, the homestead credit percentage for the taxable year beginning the following July 1. The homestead credit percentage shall be no [greater] less than 100% [plus the percentage of increase in the Consumer Price Index for the previous twelve months, rounded to the nearest whole number, but not more than 105%.] or exceed 110% for any taxable year; and shall be expressed in increments of 1 percentage point.”

(Bold – proposed changes, [bracket] deleted and underlined new language.)

Therefore, CB-48-2020 proposes three things: (1) change the date by which the County would set the homestead credit percentage from January to March (as now required by State law) and (2) remove the CPI requirement and the 105% Cap and (3) add the cap between 100% and 110% (as allowed by State law).

If adopted (ratified) in the November General Election, this would put Prince George’s County in the same position as almost every other County and municipal government in the State of Maryland. The County Executive and Council, as part of the annual public budget review process, would determine the percentage of the homestead tax credit. This process would be consistent with state law, without artificial restrictions, and gives your elected officials the flexibility afforded our neighboring counties and all municipalities in the State of Maryland.

Charter Amendment Process

Section 1105 of the County Charter sets for the procedure and timing for a Charter Amendment question to be place on the ballot for consideration. Section 1105. - Charter Amendment state:

“Amendments to this Charter may be proposed by an act of the Council approved by not less than two-thirds of the members of the full Council, and such action shall be exempt from executive veto. Amendments may also be proposed by petition filed with the County Executive and signed by 10,000 registered voters of the County. When so proposed, whether by act of the Council or by petition, the question shall be submitted to the voters of the County at the next general election occurring after the passage of said act or the filing of said petition; and if at said election the majority of votes cast on the question shall be in favor of the proposed amendment, such amendment shall stand adopted from and after the thirtieth day following said election. Any amendments to this Charter, proposed in the manner aforesaid, shall be published by the County Executive in the County newspapers of record and in media for public notice as defined in Section 1008 of this Charter for five successive weeks prior to the election at which the question shall be considered by the voters of the County.”

In order to meet the Charter and State law certification requirements, as well as the Council legislative calendar, any Council Charter Amendment would have to be introduced by the end of June, be subject to a Public Hearing and enacted by the end of July. In this case, CB-48-2020 was presented on June 23rd, heard in our Committee of the Whole and favorably recommended by a vote of 8-3. It will now go to a Public Hearing on Tuesday July 21st prior to any vote by the Council to place it on the ballot. The Council will also adopt legislation for the ordering of all questions on the November ballot (On June 23rd the Council also approved 6 bond bills for referendum, which will also have public hearings on the 21st). If enacted, the proposed Charter Amendment in CB-48-2020 would have to be certified by the County Attorney and transmitted to the County Board of Elections for placement on the November General Election ballot for the voters.

Please visit the Clerk of the Council’s website for instructions on public participation, including providing written testimony or comments to the Council - https://pgccouncil.us/DocumentCenter/View/5289/Submitting-a-Comment-on-an-Agenda-Item.

Community Conversations

Recent events – the impact of COVID-19 and police brutality - have forced our nation and this County to re-examine ourselves and our priorities moving forward. George Floyd’s death in police custody triggered a movement in communities across our nation and here in Prince George’s County, against police brutality and racial injustice and for social justice. The devastating impacts of COVID-19 on our community are yet to be told in full, but our knowledge of the history of the health disparities bought on by structural racism in the African American community portend trouble ahead.

As elected officials we are being asked by our residents and forced by a changing economy to do things differently and focus on new ways of doing things. We must work together to achieve the real transformative change we express as a nation and a community – the discussion on the impact of this nearly 30 year old Cap should be part of that discussion as we begin to recover from COVID-19 and address these larger issues. At the end of the day, if CB-48-20 passes the Council in July– you, the voters of this County, make the final decision on the Charter Amendment this November.

Thank you again for your interest as a resident of Prince George’s County and I hope that this has both, clarified and informed. You have been added to our legislative email database, so we may provide important information and further engage with you. Please be safe and well.

Sincerely,

Derrick Leon Davis

Prince George's County Council

Council District 6

|